Скачать с ютуб Explaining Convexity, Lecture 024, Securities Investment 101, Video 00027 в хорошем качестве

Explaining Convexity, Lecture 024, Securities Investment 101, Video 00027

11 лет назад

Скачать бесплатно и смотреть ютуб-видео без блокировок Explaining Convexity, Lecture 024, Securities Investment 101, Video 00027 в качестве 4к (2к / 1080p)

У нас вы можете посмотреть бесплатно Explaining Convexity, Lecture 024, Securities Investment 101, Video 00027 или скачать в максимальном доступном качестве, которое было загружено на ютуб. Для скачивания выберите вариант из формы ниже:

Загрузить музыку / рингтон Explaining Convexity, Lecture 024, Securities Investment 101, Video 00027 в формате MP3:

Если кнопки скачивания не

загрузились

НАЖМИТЕ ЗДЕСЬ или обновите страницу

Если возникают проблемы со скачиванием, пожалуйста напишите в поддержку по адресу внизу

страницы.

Спасибо за использование сервиса ClipSaver.ru

Explaining Convexity, Lecture 024, Securities Investment 101, Video 00027

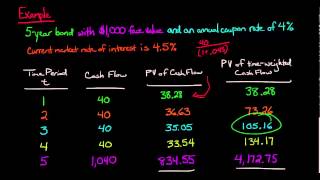

In a non-mathematical way, and before our next lecture on actually calculating convexity, we try to explain why convexity has to be taken into account, particularly for large interest rate moves in either direction. At the limit, interest rates moving down have a proportionally larger and larger effect on bond prices. Similarly, interest rates moving up have a proportionally smaller and smaller effect on bond prices. Taken together at the limit of infinitely small interest rate moves, these two effects create convexity in the bond price, when measured against changing interest rates. The flat-sloped tangential line of Modified Duration will then tend to underestimate price moves up, when interest rates move down, and will tend to overestimate price moves down, when interest rates move up. This is the calculus principle behind convexity. In our next lecture, we will actually calculate convexity. Previous lecture: • Modified Duration, Lecture 023, Secur... Next lecture: • Calculating Convexity, Lecture 025, S... For financial education from London to Singapore and beyond, please contact MithrilMoney via the following website: http://mithrilmoney.com/ This MithrilMoney lecture was delivered by Andy Duncan, CQF. Please read our disclaimer: http://mithrilmoney.com/disclaimer/

Comments