The Lifestyle Lock-In Trap: Why Your 40s Cost You $900,000 скачать в хорошем качестве

The Lifestyle Lock-In Trap: Why Your 40s Cost You $900,000

12 дней назад

Не удается загрузить Youtube-плеер. Проверьте блокировку Youtube в вашей сети.

Повторяем попытку...

Повторяем попытку...

Скачать видео с ютуб по ссылке или смотреть без блокировок на сайте: The Lifestyle Lock-In Trap: Why Your 40s Cost You $900,000 в качестве 4k

У нас вы можете посмотреть бесплатно The Lifestyle Lock-In Trap: Why Your 40s Cost You $900,000 или скачать в максимальном доступном качестве, видео которое было загружено на ютуб. Для загрузки выберите вариант из формы ниже:

-

Информация по загрузке:

Скачать mp3 с ютуба отдельным файлом. Бесплатный рингтон The Lifestyle Lock-In Trap: Why Your 40s Cost You $900,000 в формате MP3:

Если кнопки скачивания не

загрузились

НАЖМИТЕ ЗДЕСЬ или обновите страницу

Если возникают проблемы со скачиванием видео, пожалуйста напишите в поддержку по адресу внизу

страницы.

Спасибо за использование сервиса ClipSaver.ru

The Lifestyle Lock-In Trap: Why Your 40s Cost You $900,000

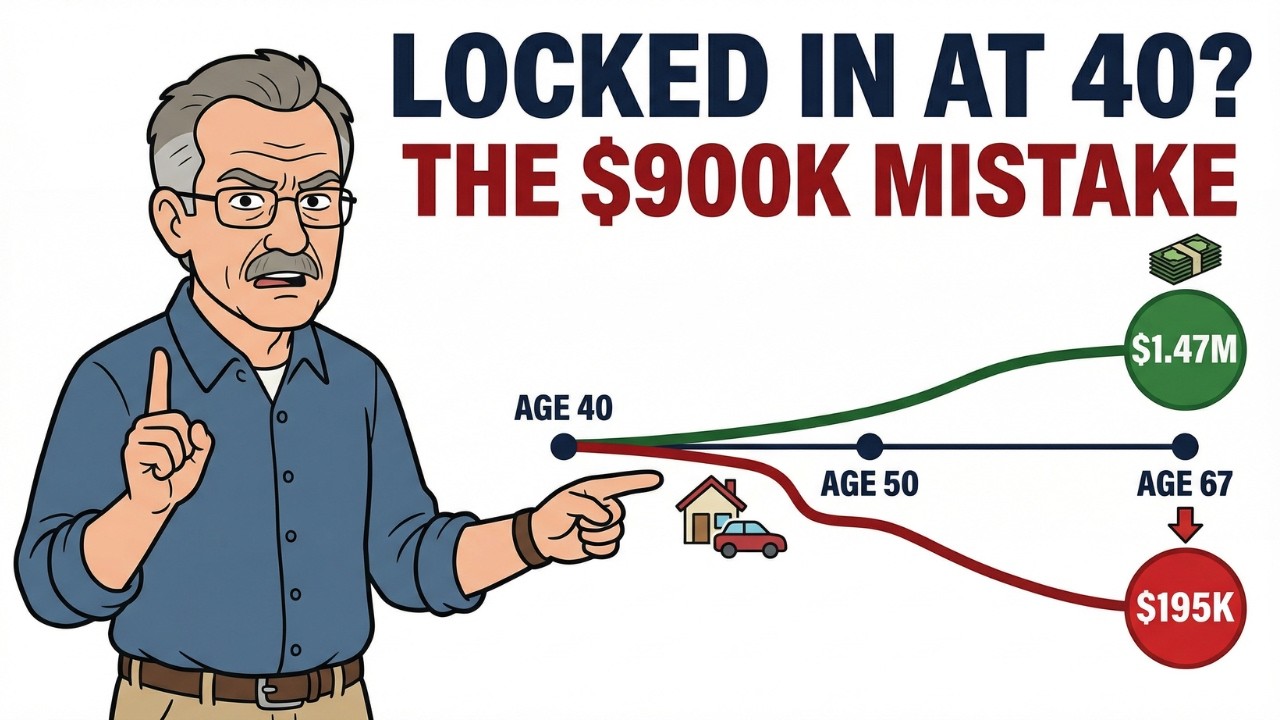

You hit your peak earning years in your 40s. Your income is finally strong. The kids are older. The career is stable. So why do so many high earners end up retiring stressed, underfunded, or forced to keep working? In this video, we break down The Lifestyle Lock-In Trap—the hidden financial force that can quietly cost you $900,000 over a single decade. Not because you invested badly. Not because you lacked information. But because of a series of completely reasonable decisions that permanently redirected your compounding window. I’ll walk you through: • Why your 40s are the most financially leveraged decade of your life • The three forces that converge during this period (peak income, remaining compounding time, and expense stabilization) • How a $1,500 monthly lifestyle upgrade can quietly become a $1 million opportunity cost • Real-world case studies of two couples with nearly identical incomes who ended up nearly $900,000 apart in retirement • The psychology of hedonic adaptation—and why lifestyle upgrades stop making you happier within 18–24 months • How healthcare costs (now estimated at $330,000 per couple in retirement) quietly destroy underfunded retirement plans • The exact framework to calculate your personal “lifestyle lock-in number” before making your next major financial decision If you’re in your 30s or 40s wondering whether you’re truly on track for financial independence—or just hoping it works out—this breakdown will change how you evaluate spending, saving, and long-term wealth building. This isn’t about extreme frugality. It’s about understanding the asymmetry: The discomfort of resisting lifestyle inflation lasts ten years. The reward lasts thirty. 👉 Subscribe for more deep dives into personal finance, wealth building, and the psychology behind money decisions. ⸻ Timestamps: 00:00 – Two Retirements, Same Income 03:12 – The Real Problem Isn’t Information 06:45 – The Leverage Window Explained 11:30 – The $1.28M vs $760K Example 16:20 – Healthcare Costs Nobody Plans For 20:05 – Kevin & Sarah’s $900K Gap 27:40 – The Psychology of Lifestyle Lock-In 32:15 – How to Calculate Your Lock-In Number 36:50 – The One Question That Changes Everything ⸻ 📚 Research & Data Mentioned: Empower – 2025 Retirement Savings Research Fidelity – Retirement Savings Benchmarks (2025) Fidelity – Estimated Healthcare Costs in Retirement (2025) Historical S&P 500 Long-Term Average Returns Research on Hedonic Adaptation (Behavioral Economics Studies) ⸻ ⚠️ DISCLAIMER: I am not a financial advisor, accountant, or legal professional. The content presented on this channel is for educational and entertainment purposes only. All opinions expressed are my own and should not be construed as financial, investment, tax, or legal advice. Every individual’s financial situation is unique, and you should consult with a qualified professional before making any financial decisions. The research and statistics cited in this video are for informational purposes and may not reflect your specific circumstances. Past economic trends are not guarantees of future conditions. The calculations, projections, and scenarios presented in this video are hypothetical and for illustrative purposes only. Actual investment returns vary significantly and past performance does not guarantee future results. The stock market involves risk, including the potential loss of principal. Always do your own research and consult with qualified financial professionals before making investment decisions or retirement plans.

Comments

-

2 дня назад

2 дня назад

-

1 день назад

1 день назад

-

3 дня назад

3 дня назад

-

1 день назад

1 день назад

-

7 часов назад

7 часов назад

-

3 часа назад

3 часа назад

-

6 часов назад

6 часов назад

-

3 месяца назад

3 месяца назад

-

6 часов назад

6 часов назад

-

6 часов назад

6 часов назад

-

Трансляция закончилась 4 часа назад

Трансляция закончилась 4 часа назад

-

1 день назад

1 день назад

-

2 месяца назад

2 месяца назад

-

1 час назад

1 час назад

-

3 дня назад

3 дня назад

-

1 день назад

1 день назад

-

Трансляция закончилась 1 день назад

Трансляция закончилась 1 день назад

-

2 дня назад

2 дня назад

-

10 дней назад

10 дней назад

-

4 месяца назад

4 месяца назад