Computing expected return or cost of equity using Fama-French model in Python скачать в хорошем качестве

Computing expected return or cost of equity using Fama-French model in Python

4 года назад

Не удается загрузить Youtube-плеер. Проверьте блокировку Youtube в вашей сети.

Повторяем попытку...

Повторяем попытку...

Скачать видео с ютуб по ссылке или смотреть без блокировок на сайте: Computing expected return or cost of equity using Fama-French model in Python в качестве 4k

У нас вы можете посмотреть бесплатно Computing expected return or cost of equity using Fama-French model in Python или скачать в максимальном доступном качестве, видео которое было загружено на ютуб. Для загрузки выберите вариант из формы ниже:

-

Информация по загрузке:

Скачать mp3 с ютуба отдельным файлом. Бесплатный рингтон Computing expected return or cost of equity using Fama-French model in Python в формате MP3:

Если кнопки скачивания не

загрузились

НАЖМИТЕ ЗДЕСЬ или обновите страницу

Если возникают проблемы со скачиванием видео, пожалуйста напишите в поддержку по адресу внизу

страницы.

Спасибо за использование сервиса ClipSaver.ru

Computing expected return or cost of equity using Fama-French model in Python

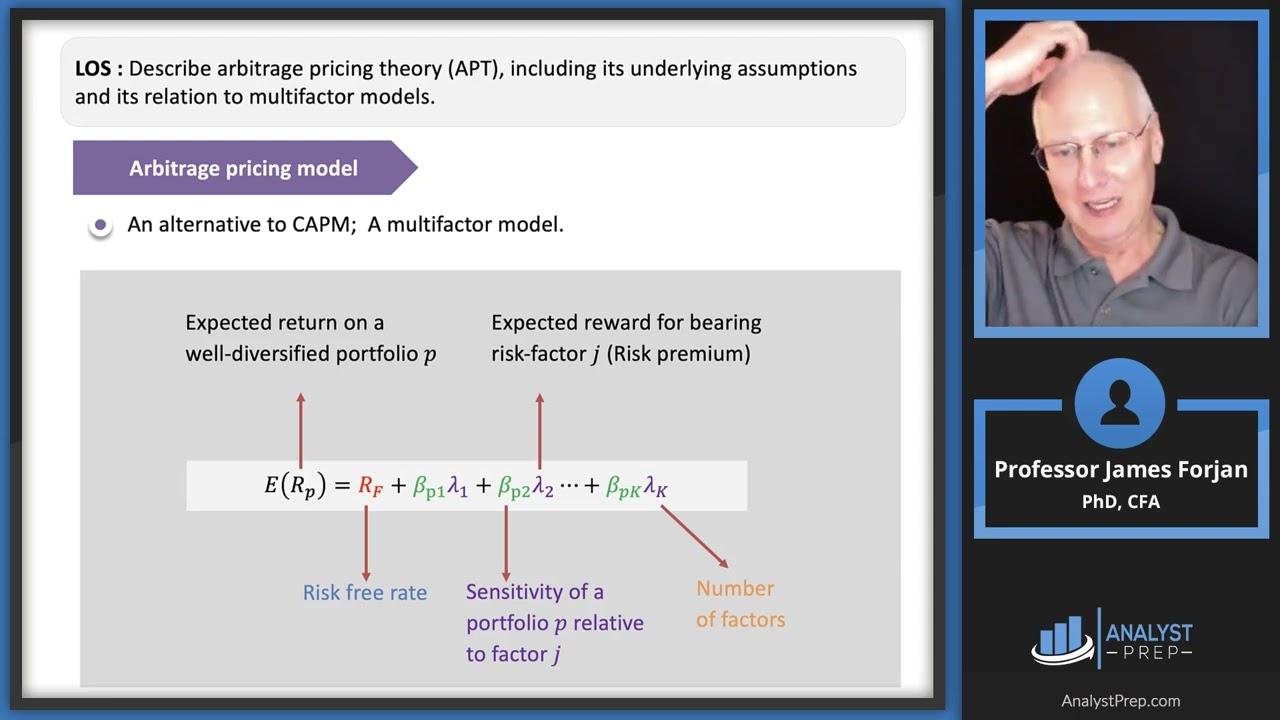

In this video, we start by explaining what kind of risks investors should expect to be rewarded with higher returns. Then we explain how to measure those risks that should be associated with higher returns. We then explain the relationship between CAPM and the Fama-French 3 factor models. Finally we go to the codes and start with the codes we wrote for estimating the CAPM in the previous video and modify it to estimate a more precise cost of equity (or expected return) based on the CAPM as well as a new expected return based on Fama-French 3 factor model for Tesla. The link to the previous video on estimating beta and the expected return based on CAPM: • Computing beta and expected return using C...

Comments