Hedging (aka, neutralizing) option delta and gamma (FRM T4-19) скачать в хорошем качестве

Hedging (aka, neutralizing) option delta and gamma (FRM T4-19)

7 лет назад

Не удается загрузить Youtube-плеер. Проверьте блокировку Youtube в вашей сети.

Повторяем попытку...

Повторяем попытку...

Скачать видео с ютуб по ссылке или смотреть без блокировок на сайте: Hedging (aka, neutralizing) option delta and gamma (FRM T4-19) в качестве 4k

У нас вы можете посмотреть бесплатно Hedging (aka, neutralizing) option delta and gamma (FRM T4-19) или скачать в максимальном доступном качестве, видео которое было загружено на ютуб. Для загрузки выберите вариант из формы ниже:

-

Информация по загрузке:

Скачать mp3 с ютуба отдельным файлом. Бесплатный рингтон Hedging (aka, neutralizing) option delta and gamma (FRM T4-19) в формате MP3:

Если кнопки скачивания не

загрузились

НАЖМИТЕ ЗДЕСЬ или обновите страницу

Если возникают проблемы со скачиванием видео, пожалуйста напишите в поддержку по адресу внизу

страницы.

Спасибо за использование сервиса ClipSaver.ru

Hedging (aka, neutralizing) option delta and gamma (FRM T4-19)

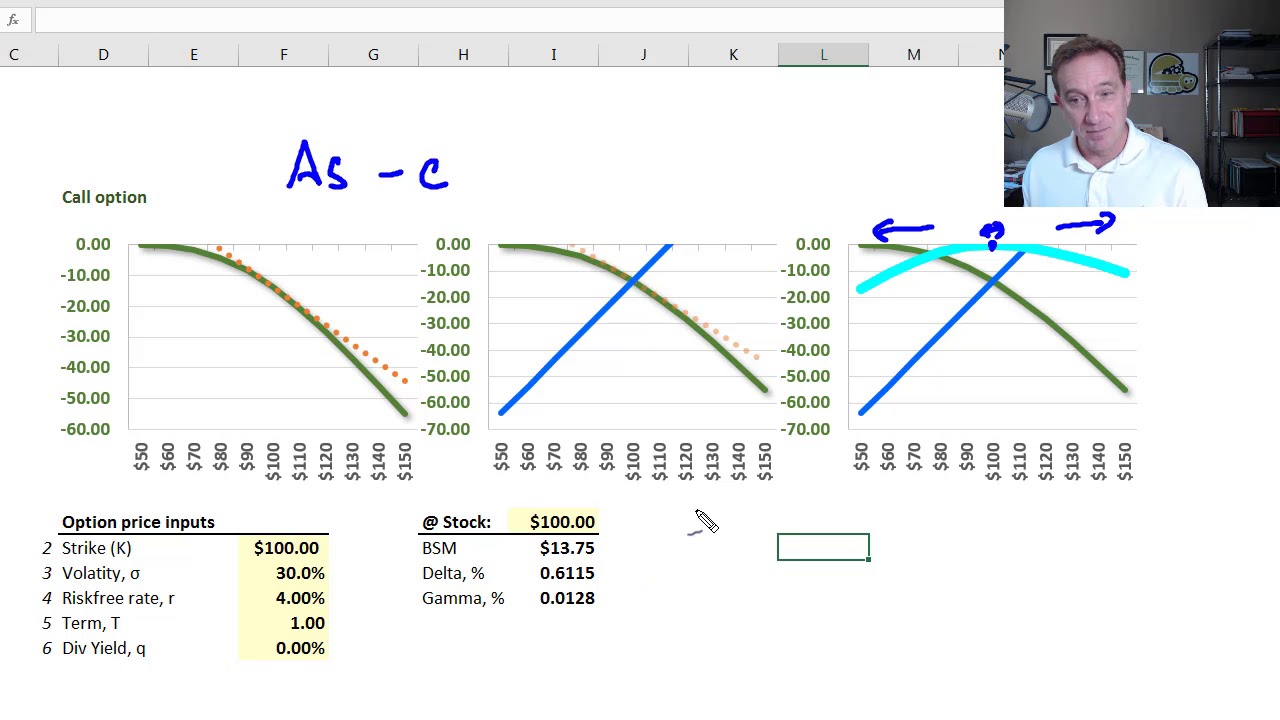

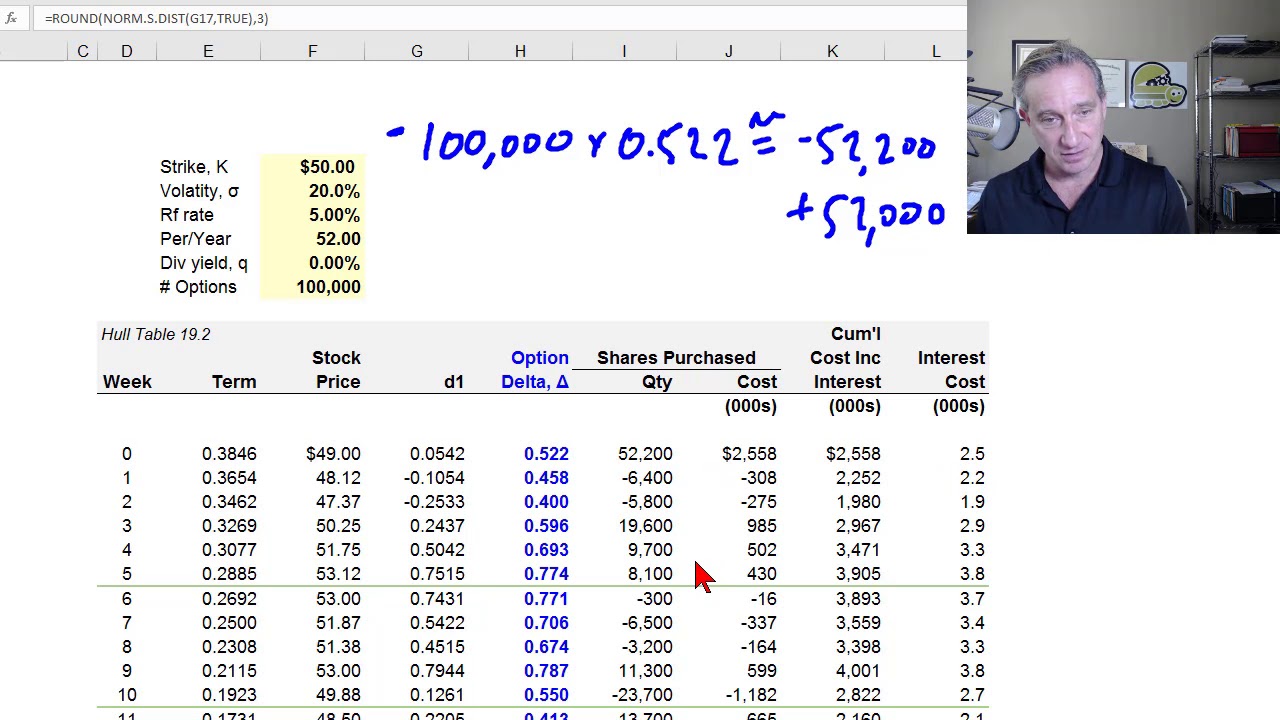

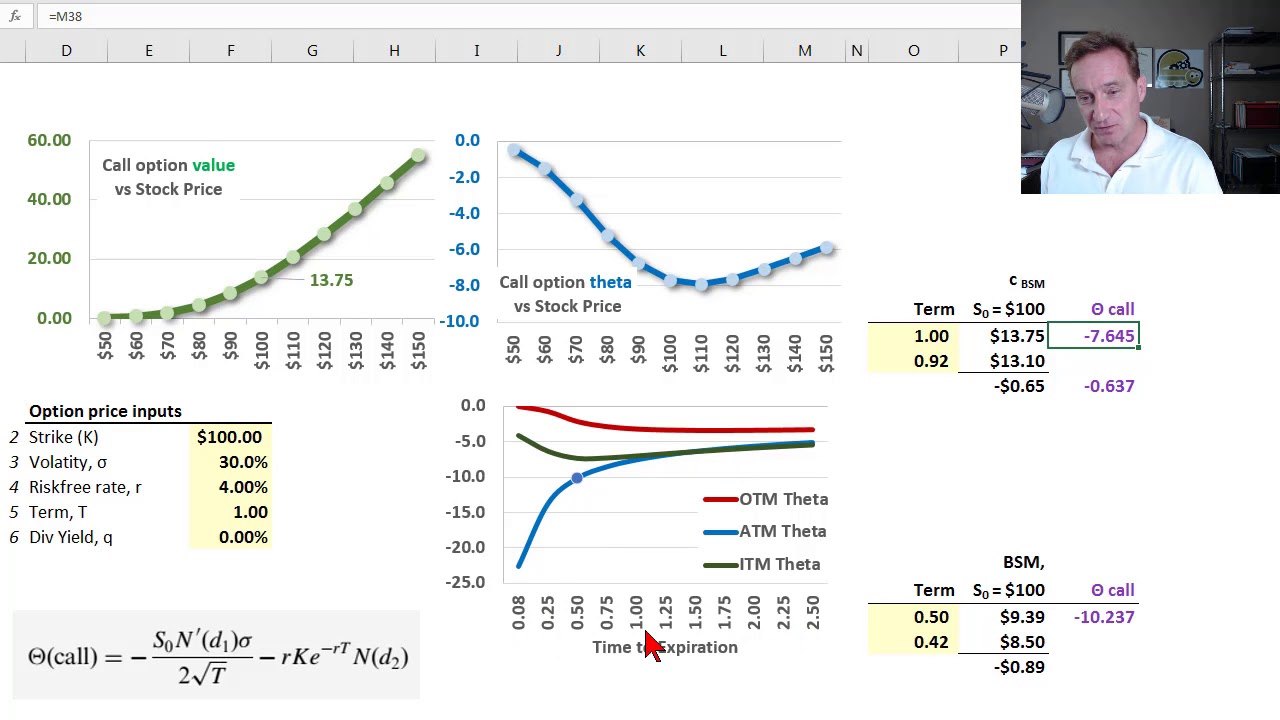

[my xls is here https://trtl.bz/2HjdxQq] To hedge options Greeks, we want to rely on the formula: +/- Quantity * %Greek = Position Greek, where a short position is represented by negative quantity. In this example, the market maker writes 10,000 ATM call options, each with percentage (per option) delta of 0.550 and gamma of 0.0440. This creates -10,000 * 0.550 = -5,500 position delta and -10,000 * 0.04400 = -440 position gamma. To neutralize (fully hedge) the gamma, the market maker buys OTM 12,055 call options, each with percentage delta of 0.270 and percentage gamma of 0.03650, which has position delta of 12,055 * 0.270 = +3,250 and position gamma of 12,055 * 0.03650 = +440. Due to -440 + 440, position gamma is now neutralized. However, position delta is -5,500 + 3,255 = -2,245 such that the market maker buys 2,245 shares (shares have 1.0 percentage delta and zero percentage gamma) and with that trade, both delta and gamma are neutralized. Discuss this video here in our FRM forum: https://trtl.bz/2Mi5BmX

Comments