Achintya Gopal (Bloomberg): "NeuralBeta and the Importance of Network Design" скачать в хорошем качестве

Achintya Gopal (Bloomberg): "NeuralBeta and the Importance of Network Design"

1 год назад

Не удается загрузить Youtube-плеер. Проверьте блокировку Youtube в вашей сети.

Повторяем попытку...

Повторяем попытку...

Скачать видео с ютуб по ссылке или смотреть без блокировок на сайте: Achintya Gopal (Bloomberg): "NeuralBeta and the Importance of Network Design" в качестве 4k

У нас вы можете посмотреть бесплатно Achintya Gopal (Bloomberg): "NeuralBeta and the Importance of Network Design" или скачать в максимальном доступном качестве, видео которое было загружено на ютуб. Для загрузки выберите вариант из формы ниже:

-

Информация по загрузке:

Скачать mp3 с ютуба отдельным файлом. Бесплатный рингтон Achintya Gopal (Bloomberg): "NeuralBeta and the Importance of Network Design" в формате MP3:

Если кнопки скачивания не

загрузились

НАЖМИТЕ ЗДЕСЬ или обновите страницу

Если возникают проблемы со скачиванием видео, пожалуйста напишите в поддержку по адресу внизу

страницы.

Спасибо за использование сервиса ClipSaver.ru

Achintya Gopal (Bloomberg): "NeuralBeta and the Importance of Network Design"

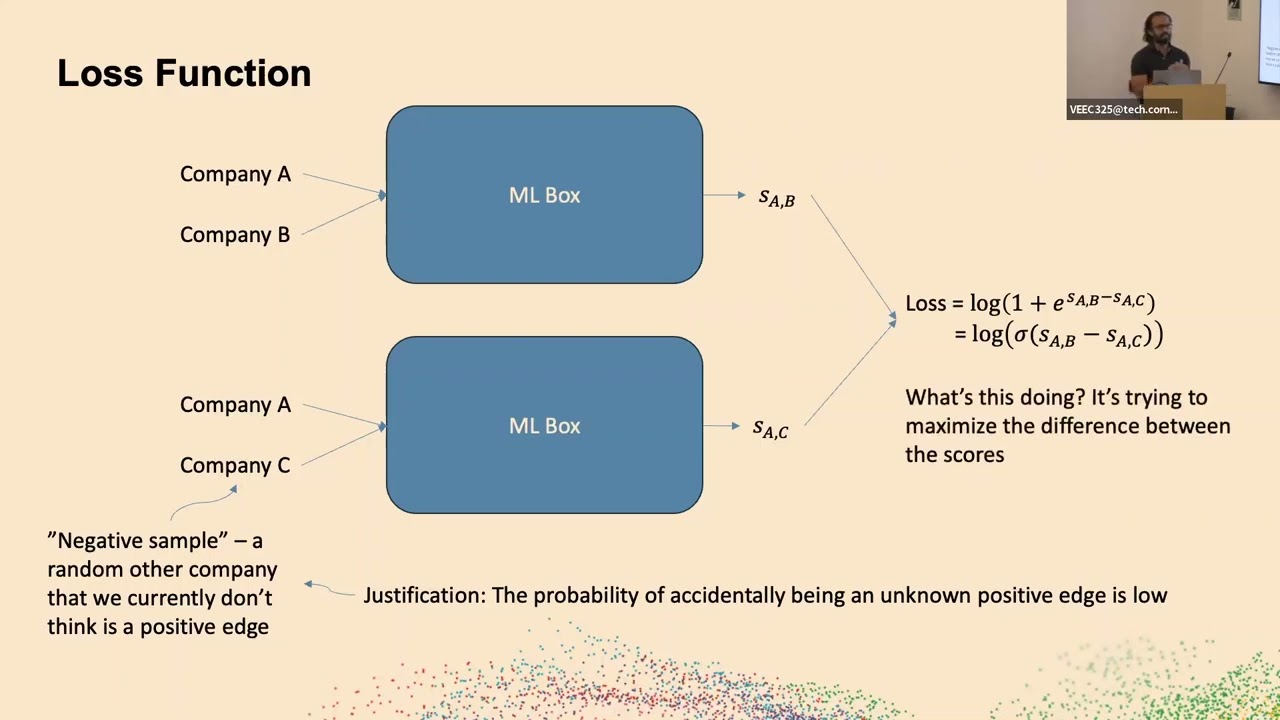

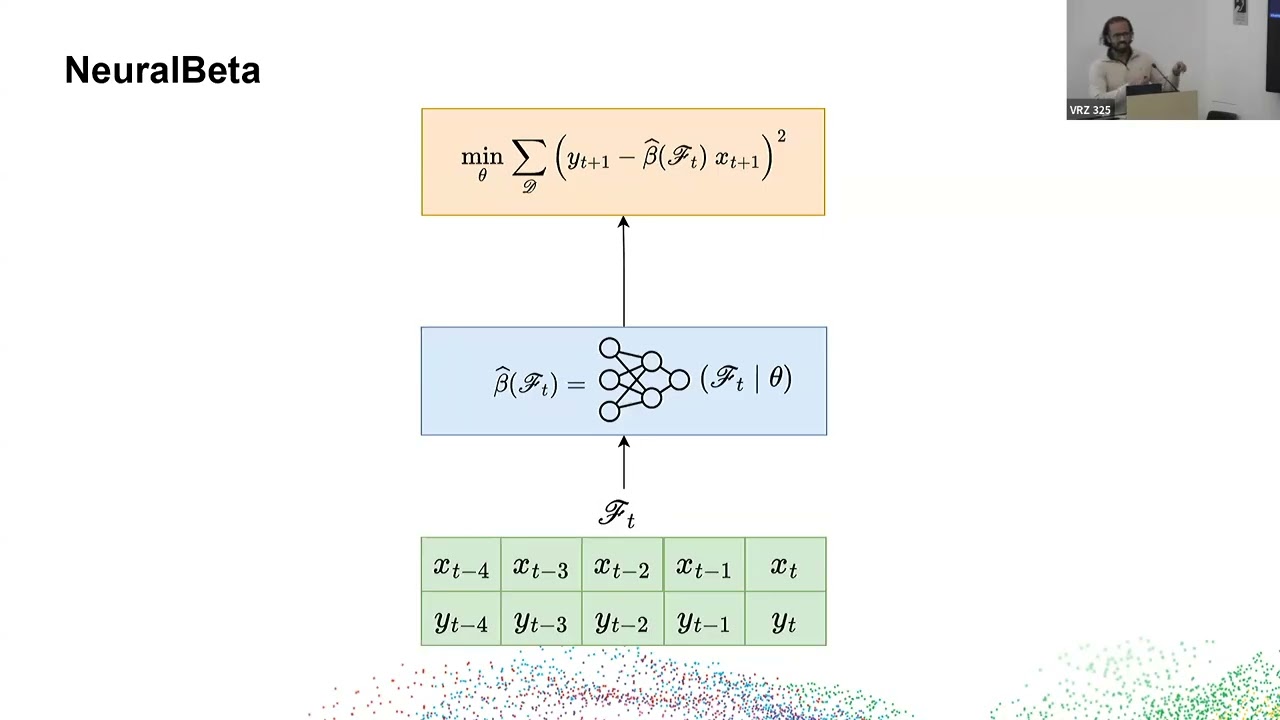

Abstract: A common approach in finance is to find a linear relationship between two variables, such as the beta between stock returns and market returns, the delta between option returns and stock returns, or the SSR between change in implied volatility and stock returns. The most common method is to use linear regression, but this approach is too rigid for real data. What if we used neural networks instead? To address these limitations, we have developed a novel method using neural networks called NeuralBeta. NeuralBeta can estimate univariate and multivariate betas, even when they are time-varying. We also introduce a new interpretable neural network inspired by weighted linear regression, which provides transparency into the model's decision-making process (i.e., neural networks do not have to be complete black boxes). We conducted extensive experiments on both simulated and market data, demonstrating NeuralBeta's superior performance compared to benchmark methods across various scenarios, especially instances where beta is highly time-varying, e.g., during regime shifts in the market, such as what we witnessed during the COVID pandemic. Speaker Bio: Achintya Gopal is a Machine Learning Quant Researcher in the Quantitative Research group in Bloomberg’s Office of the CTO, where he works on applying machine learning within the financial domain such as designing neural networks for beta estimation and factor modeling. Prior to this, he worked on estimating carbon emissions using machine learning, developing new models in normalizing flows, and exploring new methods to evaluate statistical models with model uncertainty. More recently, he has worked on a variety of projects related to time-series modeling with neural networks, causal inference for investing, generative models in differential privacy, active learning for NLP, and generative modeling for factor analysis.

Comments