Normality Testing Jarque–Bera and Shapiro–Wilk скачать в хорошем качестве

Normality Testing Jarque–Bera and Shapiro–Wilk

10 дней назад

Не удается загрузить Youtube-плеер. Проверьте блокировку Youtube в вашей сети.

Повторяем попытку...

Повторяем попытку...

Скачать видео с ютуб по ссылке или смотреть без блокировок на сайте: Normality Testing Jarque–Bera and Shapiro–Wilk в качестве 4k

У нас вы можете посмотреть бесплатно Normality Testing Jarque–Bera and Shapiro–Wilk или скачать в максимальном доступном качестве, видео которое было загружено на ютуб. Для загрузки выберите вариант из формы ниже:

-

Информация по загрузке:

Скачать mp3 с ютуба отдельным файлом. Бесплатный рингтон Normality Testing Jarque–Bera and Shapiro–Wilk в формате MP3:

Если кнопки скачивания не

загрузились

НАЖМИТЕ ЗДЕСЬ или обновите страницу

Если возникают проблемы со скачиванием видео, пожалуйста напишите в поддержку по адресу внизу

страницы.

Спасибо за использование сервиса ClipSaver.ru

Normality Testing Jarque–Bera and Shapiro–Wilk

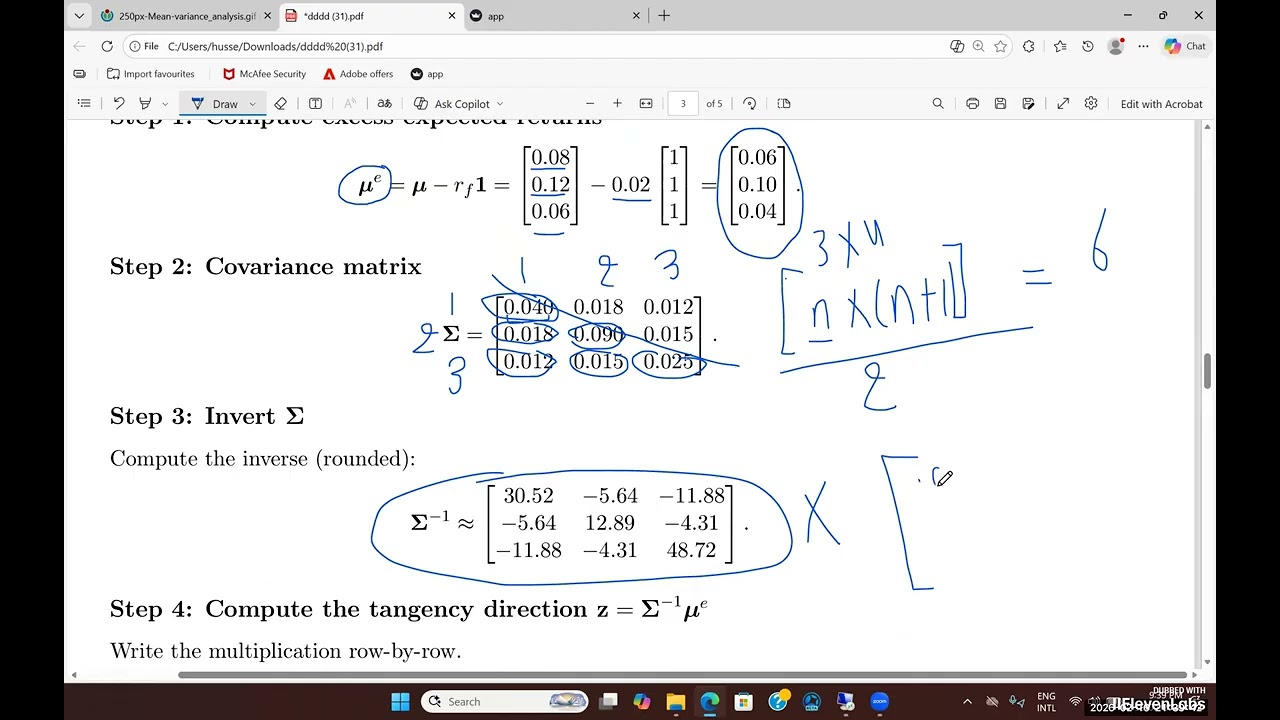

This lecture explains how to test normality in financial returns using the Jarque–Bera and Shapiro–Wilk tests. We build intuition using histograms, KDEs, and normal Q–Q plots, and show why financial return data often look normal in the center but fail in the tails. The video clarifies what rejection of normality really means, how skewness and fat tails drive the results, and why this behavior is expected in finance rather than a problem. The analysis is demonstrated using monthly sector returns implemented on the Finance Research Gate platform, with an applied, econometrics-focused interpretation.

Comments