Maximum Sharpe Ratio Portfolio Optimization: Theory and Implementation скачать в хорошем качестве

Maximum Sharpe Ratio Portfolio Optimization: Theory and Implementation

12 дней назад

Не удается загрузить Youtube-плеер. Проверьте блокировку Youtube в вашей сети.

Повторяем попытку...

Повторяем попытку...

Скачать видео с ютуб по ссылке или смотреть без блокировок на сайте: Maximum Sharpe Ratio Portfolio Optimization: Theory and Implementation в качестве 4k

У нас вы можете посмотреть бесплатно Maximum Sharpe Ratio Portfolio Optimization: Theory and Implementation или скачать в максимальном доступном качестве, видео которое было загружено на ютуб. Для загрузки выберите вариант из формы ниже:

-

Информация по загрузке:

Скачать mp3 с ютуба отдельным файлом. Бесплатный рингтон Maximum Sharpe Ratio Portfolio Optimization: Theory and Implementation в формате MP3:

Если кнопки скачивания не

загрузились

НАЖМИТЕ ЗДЕСЬ или обновите страницу

Если возникают проблемы со скачиванием видео, пожалуйста напишите в поддержку по адресу внизу

страницы.

Спасибо за использование сервиса ClipSaver.ru

Maximum Sharpe Ratio Portfolio Optimization: Theory and Implementation

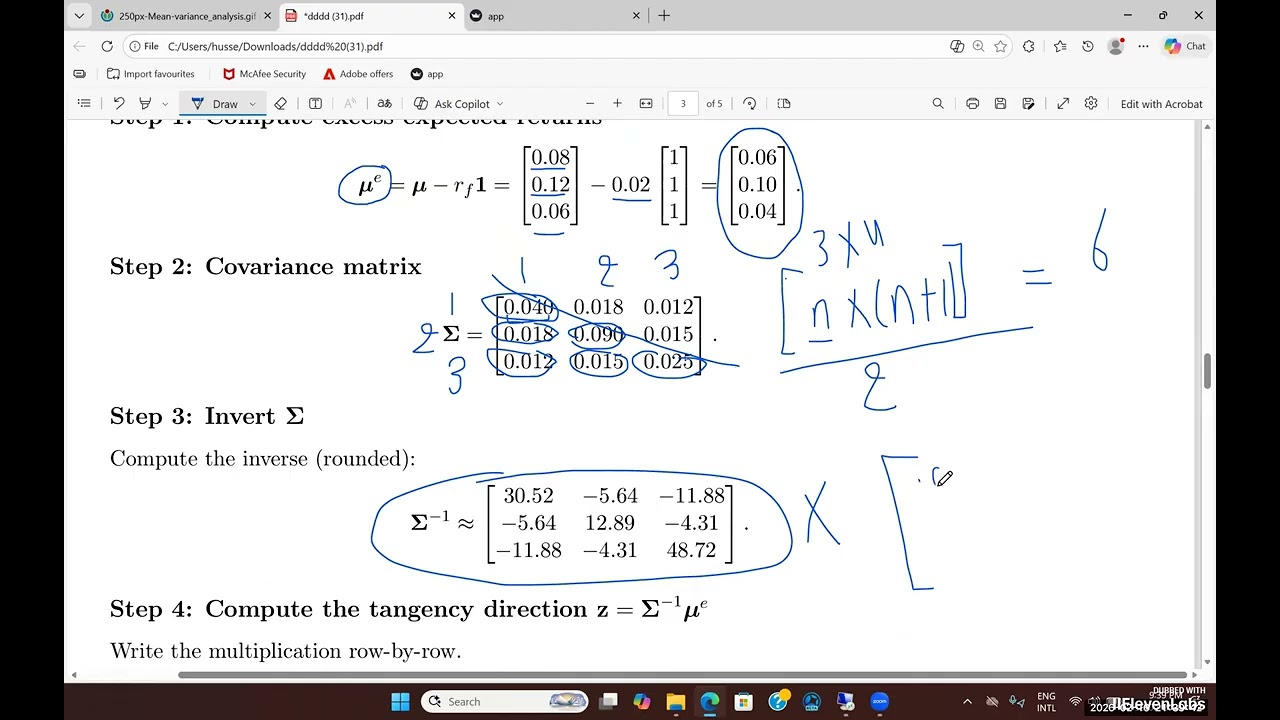

We study Maximum Sharpe Ratio portfolio optimization from both a theoretical and applied perspective. We derive the tangency portfolio and explain the role of expected returns, covariance, and the risk-free rate in Sharpe ratio maximization. Using the Finance Research Gate platform, we apply the Max Sharpe approach to real data by constructing portfolios for firms in the Consumer Staples sector and the Energy sector, and we compare the resulting portfolio behavior and performance across sectors. The lecture connects portfolio theory directly to empirical implementation and sector-level investment analysis.

Comments