Switching VAR Models and Implementation in EViews скачать в хорошем качестве

Switching VAR Models and Implementation in EViews

10 дней назад

Не удается загрузить Youtube-плеер. Проверьте блокировку Youtube в вашей сети.

Повторяем попытку...

Повторяем попытку...

Скачать видео с ютуб по ссылке или смотреть без блокировок на сайте: Switching VAR Models and Implementation in EViews в качестве 4k

У нас вы можете посмотреть бесплатно Switching VAR Models and Implementation in EViews или скачать в максимальном доступном качестве, видео которое было загружено на ютуб. Для загрузки выберите вариант из формы ниже:

-

Информация по загрузке:

Скачать mp3 с ютуба отдельным файлом. Бесплатный рингтон Switching VAR Models and Implementation in EViews в формате MP3:

Если кнопки скачивания не

загрузились

НАЖМИТЕ ЗДЕСЬ или обновите страницу

Если возникают проблемы со скачиванием видео, пожалуйста напишите в поддержку по адресу внизу

страницы.

Спасибо за использование сервиса ClipSaver.ru

Switching VAR Models and Implementation in EViews

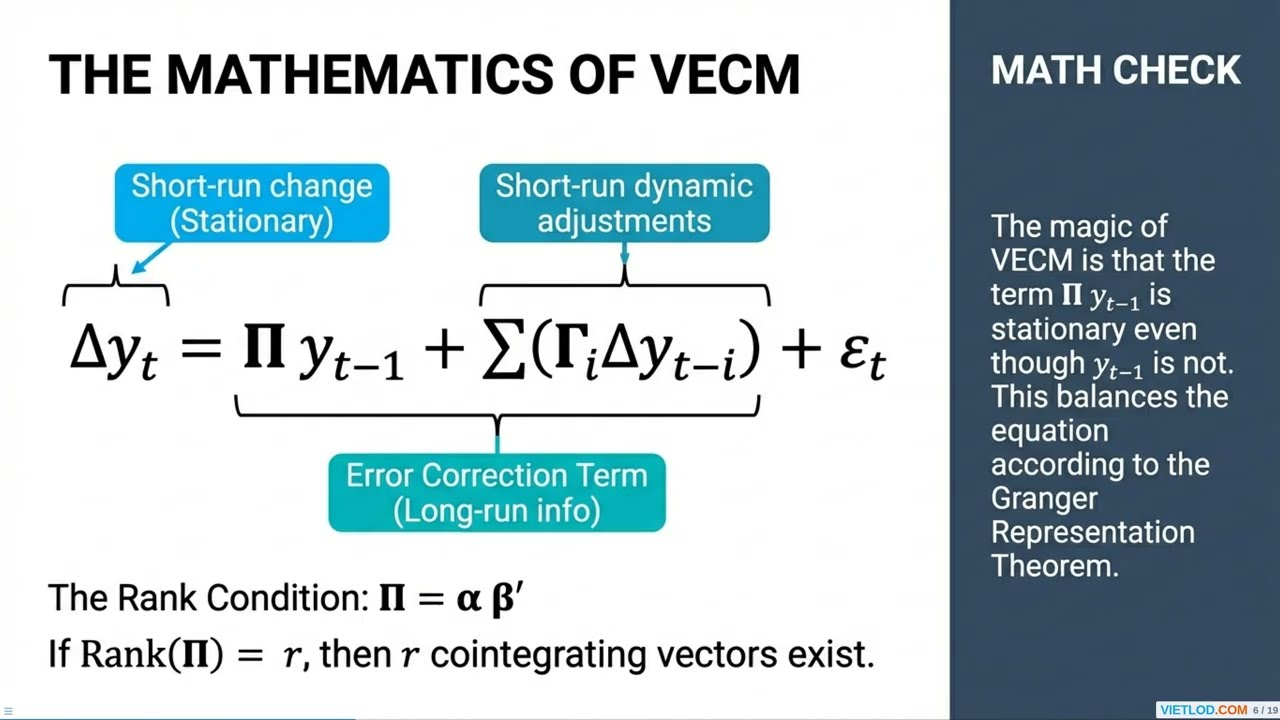

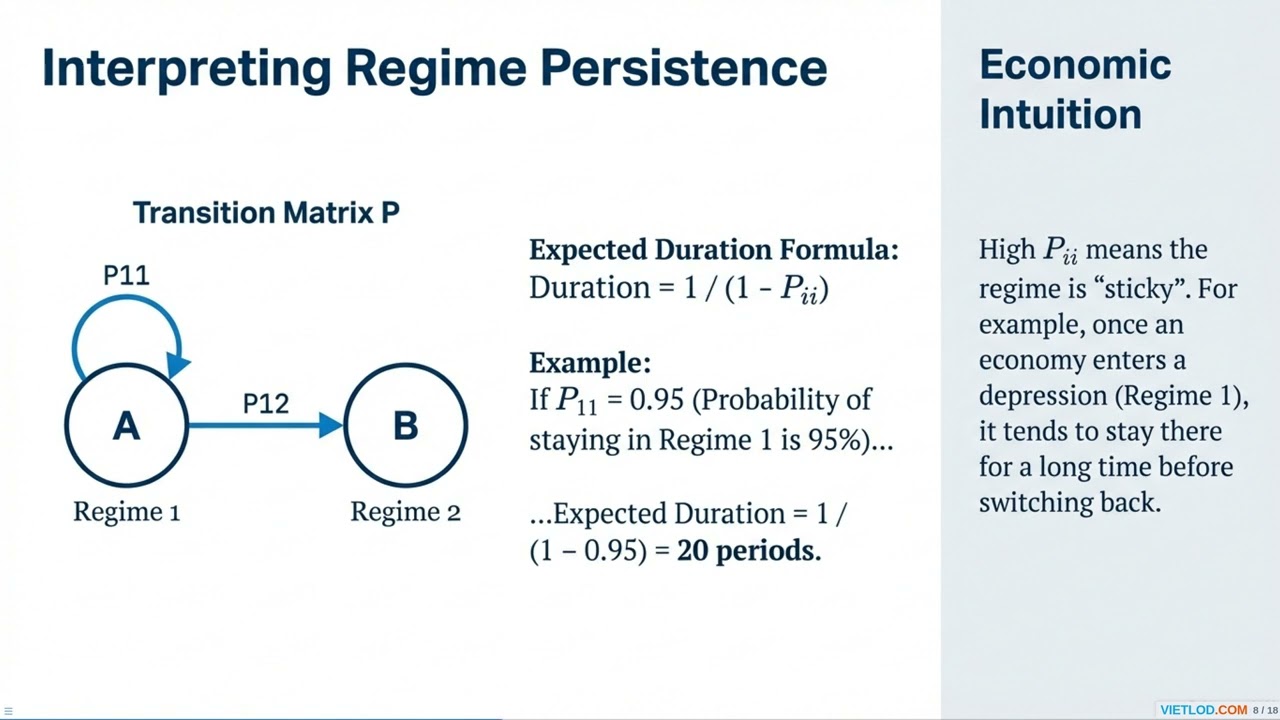

Welcome to this session on Switching Vector Autoregression Analysis, a crucial part of our Advanced Time Series Analysis course. We will be delving into both the theoretical underpinnings and practical applications, specifically demonstrating how to implement these models using EViews versions 13 and 14. This module is brought to you by the Vietlod Econometrics Group. As the excerpt on the slide highlights, integrating individual series and accounting for concepts like 'equilibrium error' naturally leads us to more sophisticated modeling frameworks, such as vector error correction models and, by extension, the switching VAR models we'll explore today. These advanced models are essential for capturing the dynamic, non-linear behaviors often observed in economic and financial time series, moving beyond the limitations of traditional linear models. The fundamental problem with a standard VAR (*Vector Autoregression*) model is its assumption of linearity and stability. It presumes that the parameters governing the economic system are constant over time. However, the real world is not so simple. Economies experience *structural breaks* due to events like wars, major policy shocks, or financial crises. They also shift between discrete states, such as a recessionary period versus an expansionary one. When a linear model is forced upon data that contains these different regimes, it essentially averages them out. This leads to a poor fit and, more importantly, unreliable forecasts. Think of modeling traffic speed. A single average speed for... #eviews #regression

Comments