Bayesian Time-varying Coefficients VAR (BTVCVAR) Models in EViews скачать в хорошем качестве

Bayesian Time-varying Coefficients VAR (BTVCVAR) Models in EViews

10 дней назад

Не удается загрузить Youtube-плеер. Проверьте блокировку Youtube в вашей сети.

Повторяем попытку...

Повторяем попытку...

Скачать видео с ютуб по ссылке или смотреть без блокировок на сайте: Bayesian Time-varying Coefficients VAR (BTVCVAR) Models in EViews в качестве 4k

У нас вы можете посмотреть бесплатно Bayesian Time-varying Coefficients VAR (BTVCVAR) Models in EViews или скачать в максимальном доступном качестве, видео которое было загружено на ютуб. Для загрузки выберите вариант из формы ниже:

-

Информация по загрузке:

Скачать mp3 с ютуба отдельным файлом. Бесплатный рингтон Bayesian Time-varying Coefficients VAR (BTVCVAR) Models in EViews в формате MP3:

Если кнопки скачивания не

загрузились

НАЖМИТЕ ЗДЕСЬ или обновите страницу

Если возникают проблемы со скачиванием видео, пожалуйста напишите в поддержку по адресу внизу

страницы.

Спасибо за использование сервиса ClipSaver.ru

Bayesian Time-varying Coefficients VAR (BTVCVAR) Models in EViews

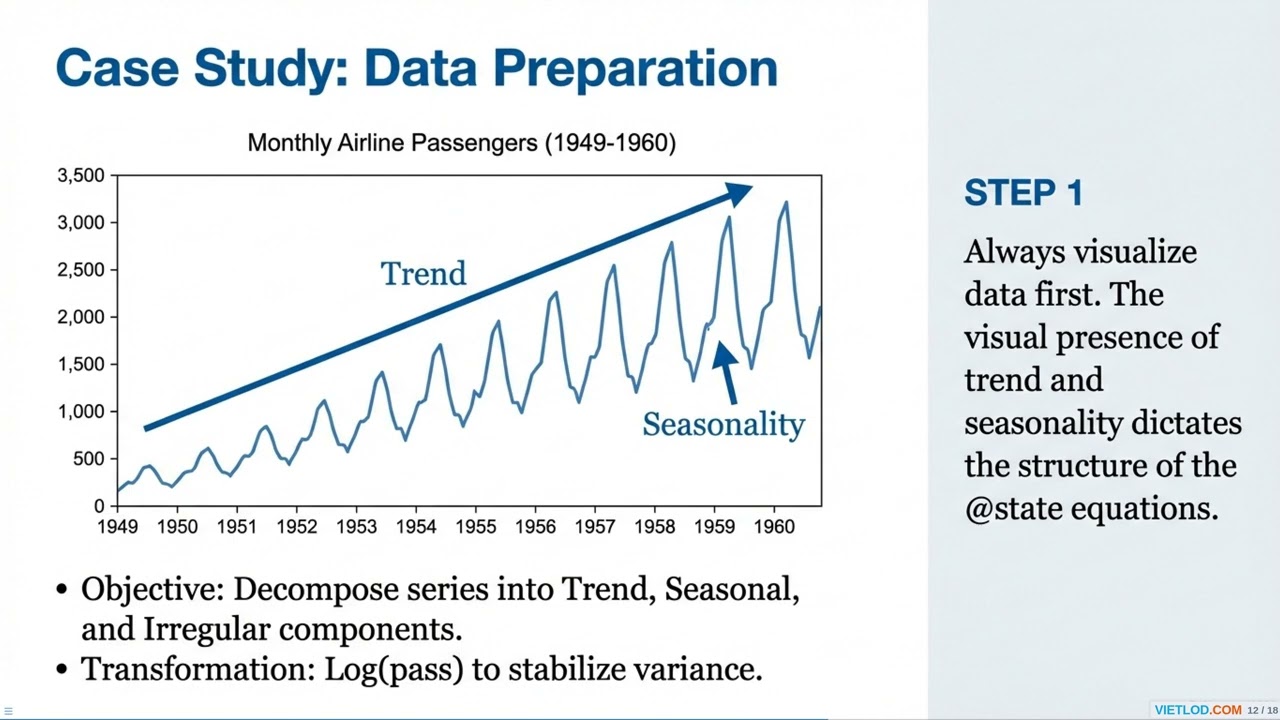

The Time-Varying Coefficients Vector Autoregression (TVCVAR) model is an advanced time-series analysis tool that relaxes the constant parameter assumption of traditional VAR models to capture constant, smooth changes in macroeconomic relationships over time. In EViews, this model is implemented using a Bayesian framework (BTVCVAR). The Bayesian approach is particularly advantageous because it utilizes prior distributions to provide a convenient way to induce parameter shrinkage. This technique helps overcome the over-parameterization issues common in VAR models by shrinking the estimates towards a simpler or stylized baseline model, yielding coefficients that evolve more smoothly over time. To estimate a BTVCVAR model in EViews, simply select Quick - Estimate VAR... from the main menu and choose Bayesian TVCVAR from the VAR type dropdown list. The dialog features three main tabs: the Basics tab for declaring endogenous variables and lags, the Prior tab for setting six scalar hyper-parameters of the prior distribution, and the Options tab where you can select a simulation smoother (such as CFA, KFS, or MMP) and enforce stable VAR coefficients (Cogley & Sargent stability). Once the posterior simulation is complete, EViews presents comprehensive output, including graphs showing the evolution of the coefficients over time,. Furthermore, computing Impulse Response Functions (IRFs) for a BTVCVAR calculates an IRF for every single date in the estimation sample, allowing for highly detailed dynamic impact analysis.

Comments