State Space Models and the Kalman Filter in EViews скачать в хорошем качестве

State Space Models and the Kalman Filter in EViews

6 дней назад

Не удается загрузить Youtube-плеер. Проверьте блокировку Youtube в вашей сети.

Повторяем попытку...

Повторяем попытку...

Скачать видео с ютуб по ссылке или смотреть без блокировок на сайте: State Space Models and the Kalman Filter in EViews в качестве 4k

У нас вы можете посмотреть бесплатно State Space Models and the Kalman Filter in EViews или скачать в максимальном доступном качестве, видео которое было загружено на ютуб. Для загрузки выберите вариант из формы ниже:

-

Информация по загрузке:

Скачать mp3 с ютуба отдельным файлом. Бесплатный рингтон State Space Models and the Kalman Filter in EViews в формате MP3:

Если кнопки скачивания не

загрузились

НАЖМИТЕ ЗДЕСЬ или обновите страницу

Если возникают проблемы со скачиванием видео, пожалуйста напишите в поддержку по адресу внизу

страницы.

Спасибо за использование сервиса ClipSaver.ru

State Space Models and the Kalman Filter in EViews

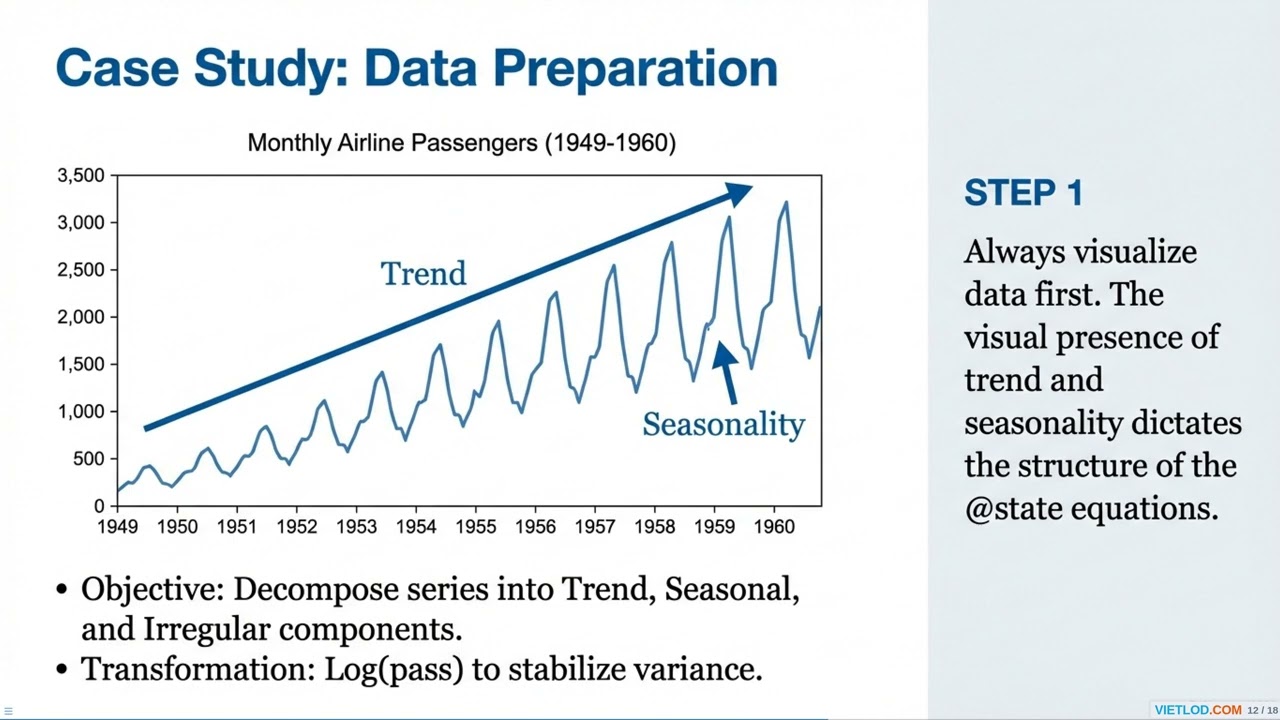

The State Space model is a time-series econometric framework for analyzing dynamic systems, integrating observable data with unobserved components like hidden trends or expectations. The structure comprises signal equations and state equations. The Kalman filter provides an optimal recursive algorithm for computing forecasts, updating, and smoothing states In EViews, you implement this using the Sspace object. Declare observation equations using the @SIGNAL keyword and transition equations using @STATE. Variances are defined directly via [var=...] or parameterized using @ename and @evar. The Proc - Define State Space... tool can automate this specification. Click Estimate to evaluate unknown parameters via maximum likelihood (MLE), and use Forecast for dynamic, smoothed, or n-step ahead predictions.

Comments