Finance Theory — 14.6: Risk Parameter Estimation and Stationarity скачать в хорошем качестве

Finance Theory — 14.6: Risk Parameter Estimation and Stationarity

2 недели назад

Не удается загрузить Youtube-плеер. Проверьте блокировку Youtube в вашей сети.

Повторяем попытку...

Повторяем попытку...

Скачать видео с ютуб по ссылке или смотреть без блокировок на сайте: Finance Theory — 14.6: Risk Parameter Estimation and Stationarity в качестве 4k

У нас вы можете посмотреть бесплатно Finance Theory — 14.6: Risk Parameter Estimation and Stationarity или скачать в максимальном доступном качестве, видео которое было загружено на ютуб. Для загрузки выберите вариант из формы ниже:

-

Информация по загрузке:

Скачать mp3 с ютуба отдельным файлом. Бесплатный рингтон Finance Theory — 14.6: Risk Parameter Estimation and Stationarity в формате MP3:

Если кнопки скачивания не

загрузились

НАЖМИТЕ ЗДЕСЬ или обновите страницу

Если возникают проблемы со скачиванием видео, пожалуйста напишите в поддержку по адресу внизу

страницы.

Спасибо за использование сервиса ClipSaver.ru

Finance Theory — 14.6: Risk Parameter Estimation and Stationarity

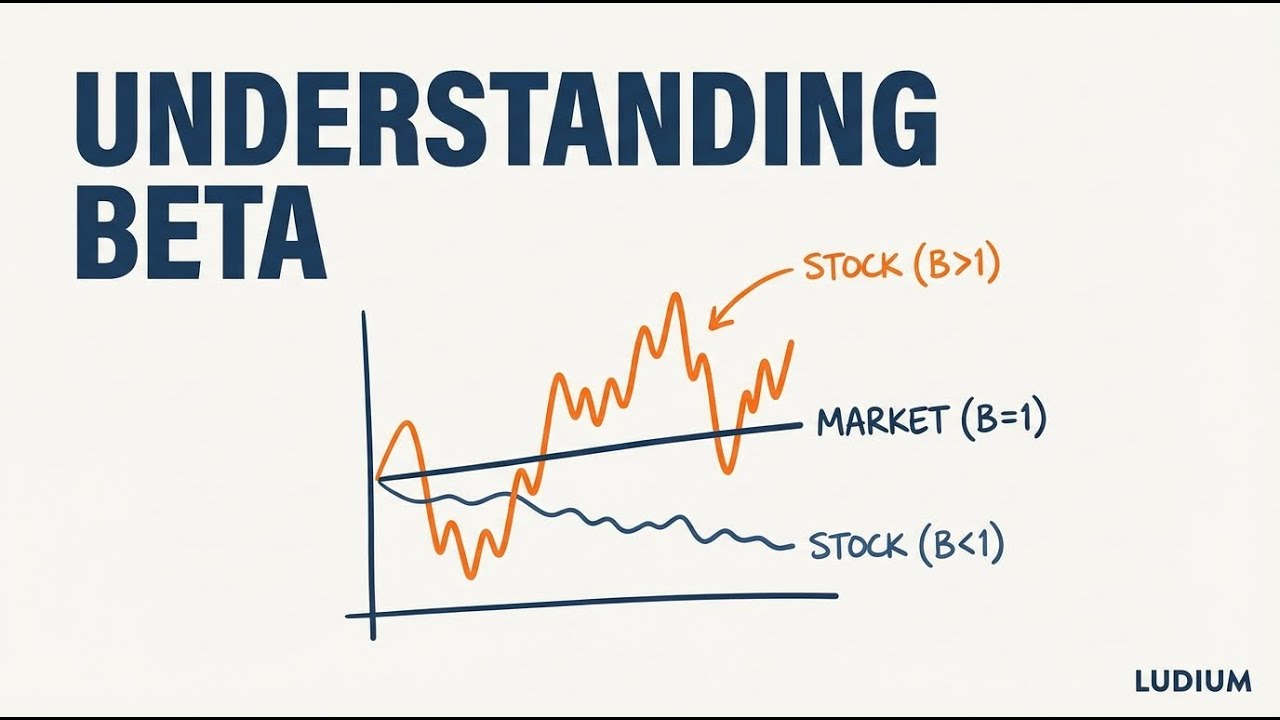

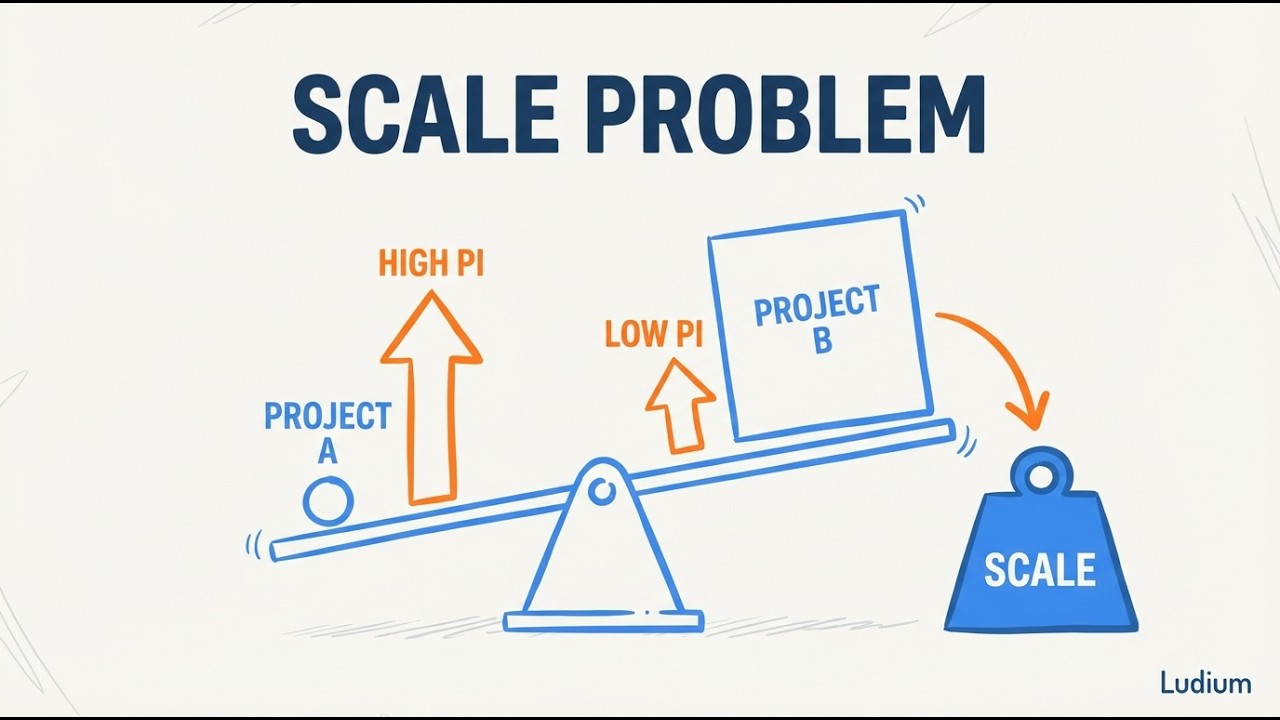

How much historical data should you use to estimate portfolio risk parameters — and when should you override the math with judgment? This video walks through the covariance estimation formula with a concrete numerical example, explains the fundamental tradeoff between statistical precision and economic relevance, and builds a practical decision framework for choosing estimation windows. Key concepts covered: • Sample covariance formula: computing cross-products of return deviations and averaging across periods • Numerical example: two-stock, four-period covariance calculation step by step • Non-stationarity: why the statistical properties of financial returns change over time • The estimation window tradeoff: more data reduces noise, but older data introduces systematic bias • Annualizing volatility: converting monthly variance to annual variance using the square root of 12 rule • Portfolio theory vs. stock picking: two fundamentally different investment philosophies and their assumptions • Why crisis data (1987, 1998, 2000, 2008, 2020) should not be excluded from long-term estimates • Rolling correlations: how S&P 500 vs. NASDAQ correlation shifts dramatically during crises • Practitioner decision framework: structural breaks, regime dependence, and investment horizon • The Venn diagram of effective risk estimation: mathematical framework, economic understanding, and contextual judgment ORIGINAL SOURCE This video is based on content from the following source: • Ses 14: Portfolio Theory II

Comments

-

13 дней назад

13 дней назад

-

5 дней назад

5 дней назад

-

Трансляция закончилась 4 дня назад

Трансляция закончилась 4 дня назад

-

2 недели назад

2 недели назад

-

2 недели назад

2 недели назад

-

11 дней назад

11 дней назад

-

2 дня назад

2 дня назад

-

1 день назад

1 день назад

-

6 дней назад

6 дней назад

-

Трансляция закончилась 6 часов назад

Трансляция закончилась 6 часов назад

-

11 дней назад

11 дней назад

-

3 дня назад

3 дня назад

-

9 дней назад

9 дней назад

-

8 дней назад

8 дней назад

-

2 дня назад

2 дня назад

-

2 недели назад

2 недели назад

-

10 дней назад

10 дней назад

-

11 дней назад

11 дней назад

-

2 месяца назад

2 месяца назад

-

1 день назад

1 день назад