What is the difference between a stochastic process and a random variable? ―¹–Κ–Α―΅–Α―²―¨ –≤ ―Ö–Ψ―Ä–Ψ―à–Β–Φ –Κ–Α―΅–Β―¹―²–≤–Β

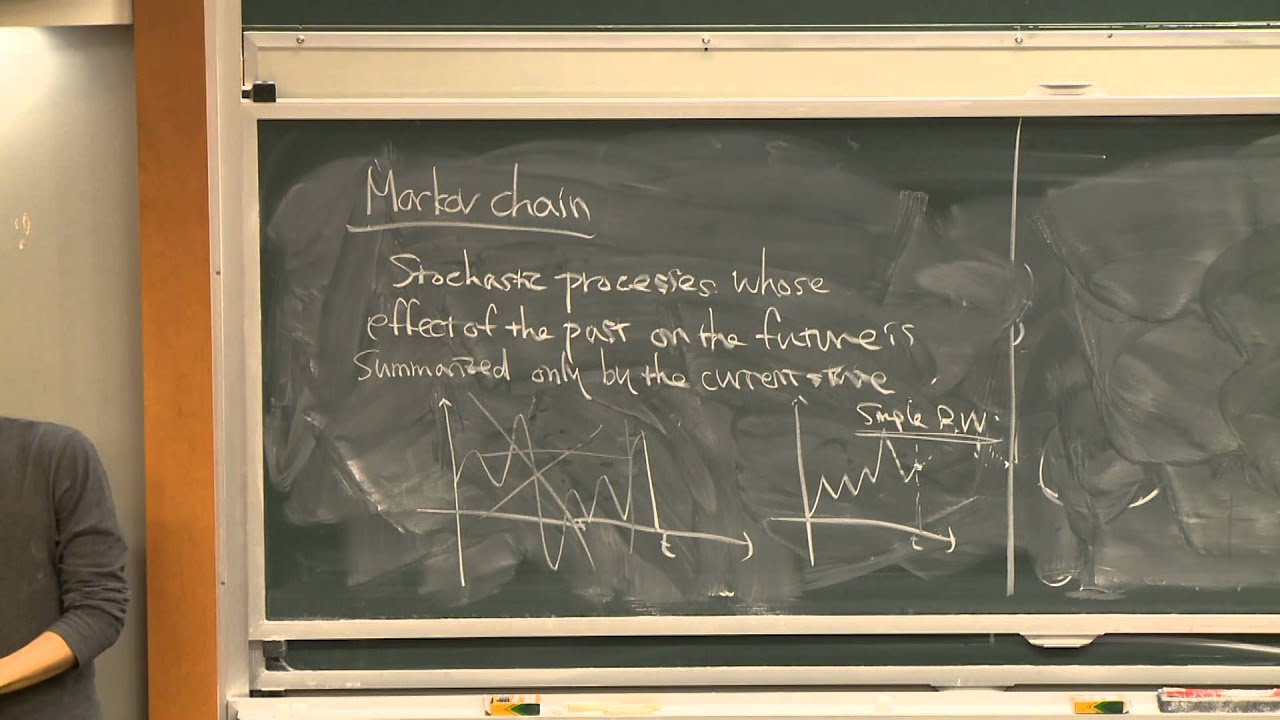

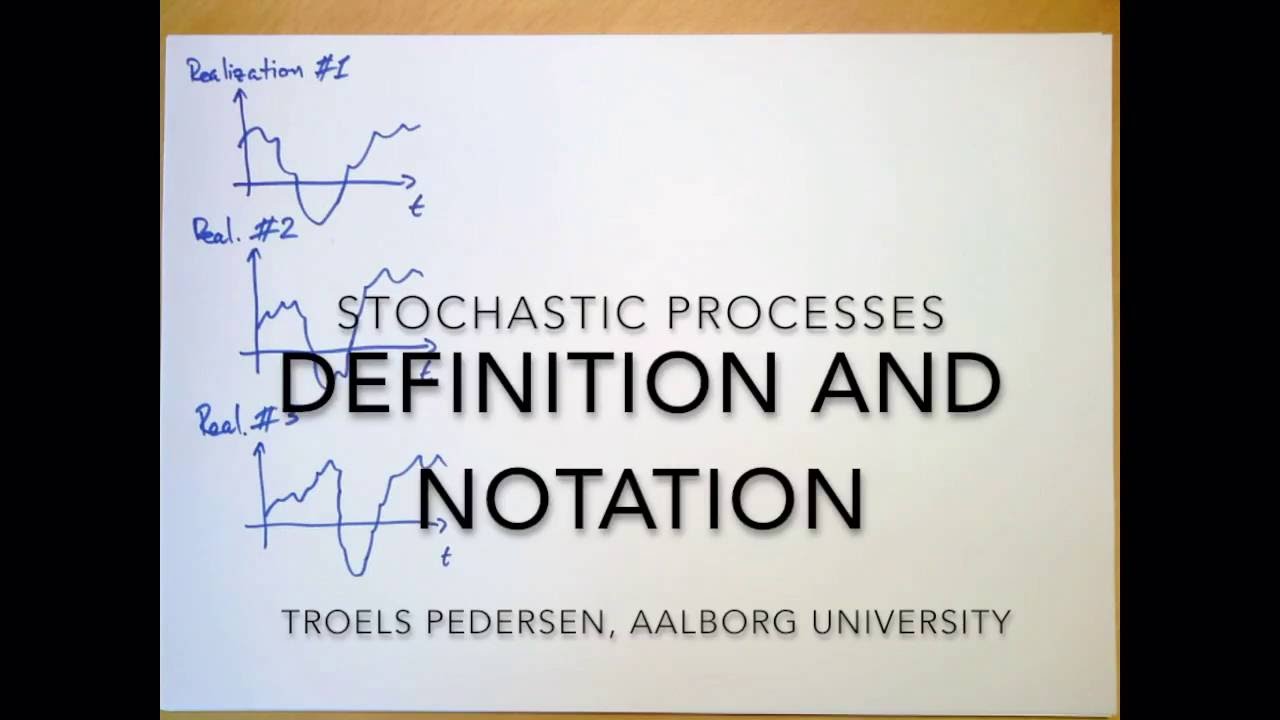

What is the difference between a stochastic process and a random variable?

3 –≥–Ψ–¥–Α –Ϋ–Α–Ζ–Α–¥

–ù–Β ―É–¥–Α–Β―²―¹―è –Ζ–Α–≥―Ä―É–Ζ–Η―²―¨ Youtube-–Ω–Μ–Β–Β―Ä. –ü―Ä–Ψ–≤–Β―Ä―¨―²–Β –±–Μ–Ψ–Κ–Η―Ä–Ψ–≤–Κ―É Youtube –≤ –≤–Α―à–Β–Ι ―¹–Β―²–Η.

–ü–Ψ–≤―²–Ψ―Ä―è–Β–Φ –Ω–Ψ–Ω―΄―²–Κ―É...

–ü–Ψ–≤―²–Ψ―Ä―è–Β–Φ –Ω–Ψ–Ω―΄―²–Κ―É...

–Γ–Κ–Α―΅–Α―²―¨ –≤–Η–¥–Β–Ψ ―¹ ―é―²―É–± –Ω–Ψ ―¹―¹―΄–Μ–Κ–Β –Η–Μ–Η ―¹–Φ–Ψ―²―Ä–Β―²―¨ –±–Β–Ζ –±–Μ–Ψ–Κ–Η―Ä–Ψ–≤–Ψ–Κ –Ϋ–Α ―¹–Α–Ι―²–Β: What is the difference between a stochastic process and a random variable? –≤ –Κ–Α―΅–Β―¹―²–≤–Β 4k

–Θ –Ϋ–Α―¹ –≤―΄ –Φ–Ψ–Ε–Β―²–Β –Ω–Ψ―¹–Φ–Ψ―²―Ä–Β―²―¨ –±–Β―¹–Ω–Μ–Α―²–Ϋ–Ψ What is the difference between a stochastic process and a random variable? –Η–Μ–Η ―¹–Κ–Α―΅–Α―²―¨ –≤ –Φ–Α–Κ―¹–Η–Φ–Α–Μ―¨–Ϋ–Ψ–Φ –¥–Ψ―¹―²―É–Ω–Ϋ–Ψ–Φ –Κ–Α―΅–Β―¹―²–≤–Β, –≤–Η–¥–Β–Ψ –Κ–Ψ―²–Ψ―Ä–Ψ–Β –±―΄–Μ–Ψ –Ζ–Α–≥―Ä―É–Ε–Β–Ϋ–Ψ –Ϋ–Α ―é―²―É–±. –î–Μ―è –Ζ–Α–≥―Ä―É–Ζ–Κ–Η –≤―΄–±–Β―Ä–Η―²–Β –≤–Α―Ä–Η–Α–Ϋ―² –Η–Ζ ―³–Ψ―Ä–Φ―΄ –Ϋ–Η–Ε–Β:

-

–‰–Ϋ―³–Ψ―Ä–Φ–Α―Ü–Η―è –Ω–Ψ –Ζ–Α–≥―Ä―É–Ζ–Κ–Β:

–Γ–Κ–Α―΅–Α―²―¨ mp3 ―¹ ―é―²―É–±–Α –Ψ―²–¥–Β–Μ―¨–Ϋ―΄–Φ ―³–Α–Ι–Μ–Ψ–Φ. –ë–Β―¹–Ω–Μ–Α―²–Ϋ―΄–Ι ―Ä–Η–Ϋ–≥―²–Ψ–Ϋ What is the difference between a stochastic process and a random variable? –≤ ―³–Ψ―Ä–Φ–Α―²–Β MP3:

–ï―¹–Μ–Η –Κ–Ϋ–Ψ–Ω–Κ–Η ―¹–Κ–Α―΅–Η–≤–Α–Ϋ–Η―è –Ϋ–Β

–Ζ–Α–≥―Ä―É–Ζ–Η–Μ–Η―¹―¨

–ù–ê–•–€–‰–Δ–ï –½–î–ï–Γ–§ –Η–Μ–Η –Ψ–±–Ϋ–Ψ–≤–Η―²–Β ―¹―²―Ä–Α–Ϋ–Η―Ü―É

–ï―¹–Μ–Η –≤–Ψ–Ζ–Ϋ–Η–Κ–Α―é―² –Ω―Ä–Ψ–±–Μ–Β–Φ―΄ ―¹–Ψ ―¹–Κ–Α―΅–Η–≤–Α–Ϋ–Η–Β–Φ –≤–Η–¥–Β–Ψ, –Ω–Ψ–Ε–Α–Μ―É–Ι―¹―²–Α –Ϋ–Α–Ω–Η―à–Η―²–Β –≤ –Ω–Ψ–¥–¥–Β―Ä–Ε–Κ―É –Ω–Ψ –Α–¥―Ä–Β―¹―É –≤–Ϋ–Η–Ζ―É

―¹―²―Ä–Α–Ϋ–Η―Ü―΄.

–Γ–Ω–Α―¹–Η–±–Ψ –Ζ–Α –Η―¹–Ω–Ψ–Μ―¨–Ζ–Ψ–≤–Α–Ϋ–Η–Β ―¹–Β―Ä–≤–Η―¹–Α ClipSaver.ru

What is the difference between a stochastic process and a random variable?

Computational Finance Q&A, Volume 1, Question 5/30 ╧╧╧╧╧╧╧╧╧╧╧╧╧╧╧╧╧╧╧╧╧╧╧╧╧╧╧╧╧╧╧╧╧╧╧╧╧╧╧ Materials discussed in this video are based on: 1) FREE online course "Computational Finance" is available at: ¬†¬†¬†βÄΔ¬†Computational¬†Finance¬†Course¬†¬† βÄΣ@ComputationsInFinanceβħ 2) Book: "Mathematical Modeling and Computation in Finance: With Exercises and Python and MATLAB Computer Codes", by C.W. Oosterlee and L.A. Grzelak, World Scientific Publishing, 2019. ╧╧╧╧╧╧╧╧╧╧╧╧╧╧╧╧╧╧╧╧╧╧╧╧╧╧╧╧╧╧╧╧╧╧╧╧╧╧╧ The slides can be found at: https://github.com/LechGrzelak/Comput... See https://quantfinancebook.com/ for more details and for additional materials. Course syllabus can be found at: https://CompFinance.ddns.net/wordpres... ╧╧╧╧╧╧╧╧╧╧╧╧╧╧╧╧╧╧╧╧╧╧╧╧╧╧╧╧╧╧╧╧╧╧╧╧╧╧╧ This volume addresses the following questions: 1. Can we use the same pricing models for different asset classes? 2. How is the money savings account related to a zero-coupon bond? 3. What are the challenges in the calculation of implied volatilities? 4. Can you price options using Arithmetic Brownian motion? 5. What is the difference between a stochastic process and a random variable? 6. What are the advantages and disadvantages of using ABM/GBM for modelling a stock process? 7. What sanity checks can you perform for a simulated stock process? 8. What is the Feynman-Kac formula? 9. What is the implied volatility term structure? 10. What are the deficiencies of the Black-Scholes model? Why is the BS model still used? 11. What is the impact of jumps on implied volatility? 12. How does the so-called ItoβÄôs table look like if we include the Poisson jump process? 13. How to derive a characteristic function for a model with jumps? 14. Is the Heston model with time-dependent parameters affine? 15. Why is adding more and more factors to the pricing models not the best idea? 16. Can you interpret the Heston model parameters and their impact on the volatility surface? 17. Can we model volatility with the Arithmetic Brownian Motion process? 18. What are the benefits of FFT compared to a βÄ€brute forceβÄù integration? 19. What to do if the FFT/COS method does not converge for increasing expansion terms? 20. What is a standard error? How to interpret it? 21. What is weak and strong convergence in Monte Carlo pricing? 22. What are the challenges of discretizing the CIR process using the Euler method? 23. Why do we need Monte Carlo if we have FFT methods for pricing? 24. How to hedge Jumps? 25. What is pathwise sensitivity? 26. What is the Bates model, and how can it be used for pricing? 27. What is the relation between European and Forward-start options? 28. What instruments to choose to calibrate your pricing model? 29. How to calibrate a pricing model? How to choose the objective function? 30. What are the Chooser options? #ComputationalFinance, #InterviewQuestions, #Quant, #Python, #QuantitativeFinance, #FinancialMathematics, #MonteCarloSimulation, #OptionPricing, #Finance, #DerivativePricing, #Options, #BlackScholes, #FreeCourse, #FinancialEngineering, #Hedging, #Simulation, #xVA ╧╧╧╧╧╧╧╧╧╧╧╧╧╧╧╧╧╧╧╧╧╧╧╧╧╧╧╧╧╧╧╧╧╧╧╧╧╧╧ Music: www.bensound.com

Comments

-

3 –≥–Ψ–¥–Α –Ϋ–Α–Ζ–Α–¥

3 –≥–Ψ–¥–Α –Ϋ–Α–Ζ–Α–¥

-

2 –≥–Ψ–¥–Α –Ϋ–Α–Ζ–Α–¥

2 –≥–Ψ–¥–Α –Ϋ–Α–Ζ–Α–¥

-

8 –Μ–Β―² –Ϋ–Α–Ζ–Α–¥

8 –Μ–Β―² –Ϋ–Α–Ζ–Α–¥

-

4 –≥–Ψ–¥–Α –Ϋ–Α–Ζ–Α–¥

4 –≥–Ψ–¥–Α –Ϋ–Α–Ζ–Α–¥

-

6 –Φ–Β―¹―è―Ü–Β–≤ –Ϋ–Α–Ζ–Α–¥

6 –Φ–Β―¹―è―Ü–Β–≤ –Ϋ–Α–Ζ–Α–¥

-

7 –Φ–Β―¹―è―Ü–Β–≤ –Ϋ–Α–Ζ–Α–¥

7 –Φ–Β―¹―è―Ü–Β–≤ –Ϋ–Α–Ζ–Α–¥

-

11 –Μ–Β―² –Ϋ–Α–Ζ–Α–¥

11 –Μ–Β―² –Ϋ–Α–Ζ–Α–¥

-

2 –≥–Ψ–¥–Α –Ϋ–Α–Ζ–Α–¥

2 –≥–Ψ–¥–Α –Ϋ–Α–Ζ–Α–¥

-

9 –Μ–Β―² –Ϋ–Α–Ζ–Α–¥

9 –Μ–Β―² –Ϋ–Α–Ζ–Α–¥

-

3 ―΅–Α―¹–Α –Ϋ–Α–Ζ–Α–¥

3 ―΅–Α―¹–Α –Ϋ–Α–Ζ–Α–¥

-

5 –¥–Ϋ–Β–Ι –Ϋ–Α–Ζ–Α–¥

5 –¥–Ϋ–Β–Ι –Ϋ–Α–Ζ–Α–¥

-

3 –≥–Ψ–¥–Α –Ϋ–Α–Ζ–Α–¥

3 –≥–Ψ–¥–Α –Ϋ–Α–Ζ–Α–¥

-

3 –Φ–Β―¹―è―Ü–Α –Ϋ–Α–Ζ–Α–¥

3 –Φ–Β―¹―è―Ü–Α –Ϋ–Α–Ζ–Α–¥

-

4 –≥–Ψ–¥–Α –Ϋ–Α–Ζ–Α–¥

4 –≥–Ψ–¥–Α –Ϋ–Α–Ζ–Α–¥

-

3 –≥–Ψ–¥–Α –Ϋ–Α–Ζ–Α–¥

3 –≥–Ψ–¥–Α –Ϋ–Α–Ζ–Α–¥

-

2 –≥–Ψ–¥–Α –Ϋ–Α–Ζ–Α–¥

2 –≥–Ψ–¥–Α –Ϋ–Α–Ζ–Α–¥

-

2 –≥–Ψ–¥–Α –Ϋ–Α–Ζ–Α–¥

2 –≥–Ψ–¥–Α –Ϋ–Α–Ζ–Α–¥

-

1 –≥–Ψ–¥ –Ϋ–Α–Ζ–Α–¥

1 –≥–Ψ–¥ –Ϋ–Α–Ζ–Α–¥

-

5 –Μ–Β―² –Ϋ–Α–Ζ–Α–¥

5 –Μ–Β―² –Ϋ–Α–Ζ–Α–¥

-

2 –≥–Ψ–¥–Α –Ϋ–Α–Ζ–Α–¥

2 –≥–Ψ–¥–Α –Ϋ–Α–Ζ–Α–¥