Finance Theory — 12.6: Correlation and Diversification скачать в хорошем качестве

Finance Theory — 12.6: Correlation and Diversification

11 часов назад

Не удается загрузить Youtube-плеер. Проверьте блокировку Youtube в вашей сети.

Повторяем попытку...

Повторяем попытку...

Скачать видео с ютуб по ссылке или смотреть без блокировок на сайте: Finance Theory — 12.6: Correlation and Diversification в качестве 4k

У нас вы можете посмотреть бесплатно Finance Theory — 12.6: Correlation and Diversification или скачать в максимальном доступном качестве, видео которое было загружено на ютуб. Для загрузки выберите вариант из формы ниже:

-

Информация по загрузке:

Скачать mp3 с ютуба отдельным файлом. Бесплатный рингтон Finance Theory — 12.6: Correlation and Diversification в формате MP3:

Если кнопки скачивания не

загрузились

НАЖМИТЕ ЗДЕСЬ или обновите страницу

Если возникают проблемы со скачиванием видео, пожалуйста напишите в поддержку по адресу внизу

страницы.

Спасибо за использование сервиса ClipSaver.ru

Finance Theory — 12.6: Correlation and Diversification

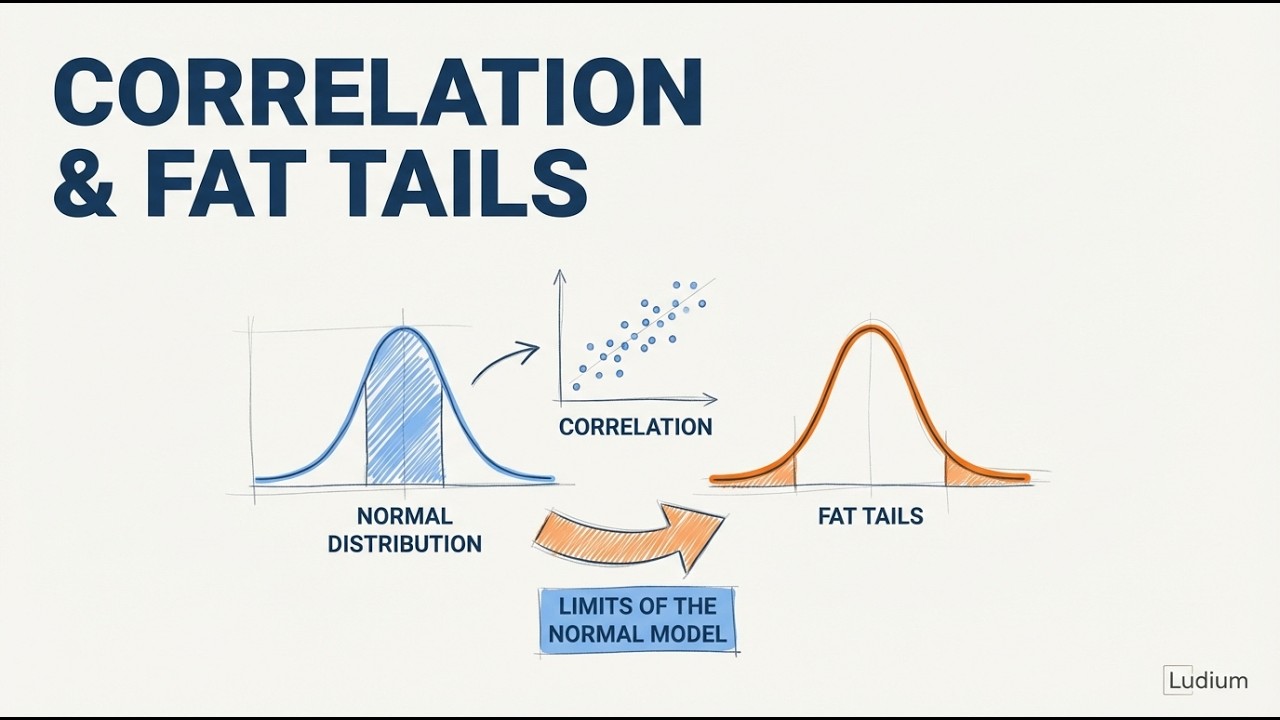

The normal distribution says Black Monday's 22% crash should occur once every several billion years — yet it happened on a regular Monday in 1987. This video explains why the bell curve fails at the extremes, how correlation drives portfolio diversification, and what fat tails mean for real-world risk management. You'll learn why combining two risky assets can produce less risk than either alone, how the correlation term in the portfolio variance equation controls everything, and why stress-testing for extreme events matters more than perfecting your model's center. Key concepts covered: • Correlation: measuring how assets move together (-1 to +1) • Why diversification depends on correlation structure, not asset count • Portfolio variance formula and the role of the correlation term (ρ) • How correlation of +1, 0, and -1 dramatically changes portfolio risk • The normal distribution's 95% accuracy — and its dangerous 5% blind spot • Fat tails: why extreme market events happen far more often than models predict • Historical evidence from GM returns, Black Monday, and S&P 500 data (1946–2001) • Practical portfolio construction: seeking low correlation and stress-testing for tail risk • The linear risk-return relationship and a preview of the CAPM equation ORIGINAL SOURCE This video distills concepts from a longer lecture. Full credit to the original creator. Source: • Ses 12: Options III & Risk and Return I

Comments