📜 CFTC Credit Risk Transfer (CRT) Swaps CDS: CPO Registration Exemption Explained (letter 25-37) скачать в хорошем качестве

📜 CFTC Credit Risk Transfer (CRT) Swaps CDS: CPO Registration Exemption Explained (letter 25-37)

3 месяца назад

Не удается загрузить Youtube-плеер. Проверьте блокировку Youtube в вашей сети.

Повторяем попытку...

Повторяем попытку...

Скачать видео с ютуб по ссылке или смотреть без блокировок на сайте: 📜 CFTC Credit Risk Transfer (CRT) Swaps CDS: CPO Registration Exemption Explained (letter 25-37) в качестве 4k

У нас вы можете посмотреть бесплатно 📜 CFTC Credit Risk Transfer (CRT) Swaps CDS: CPO Registration Exemption Explained (letter 25-37) или скачать в максимальном доступном качестве, видео которое было загружено на ютуб. Для загрузки выберите вариант из формы ниже:

-

Информация по загрузке:

Скачать mp3 с ютуба отдельным файлом. Бесплатный рингтон 📜 CFTC Credit Risk Transfer (CRT) Swaps CDS: CPO Registration Exemption Explained (letter 25-37) в формате MP3:

Если кнопки скачивания не

загрузились

НАЖМИТЕ ЗДЕСЬ или обновите страницу

Если возникают проблемы со скачиванием видео, пожалуйста напишите в поддержку по адресу внизу

страницы.

Спасибо за использование сервиса ClipSaver.ru

📜 CFTC Credit Risk Transfer (CRT) Swaps CDS: CPO Registration Exemption Explained (letter 25-37)

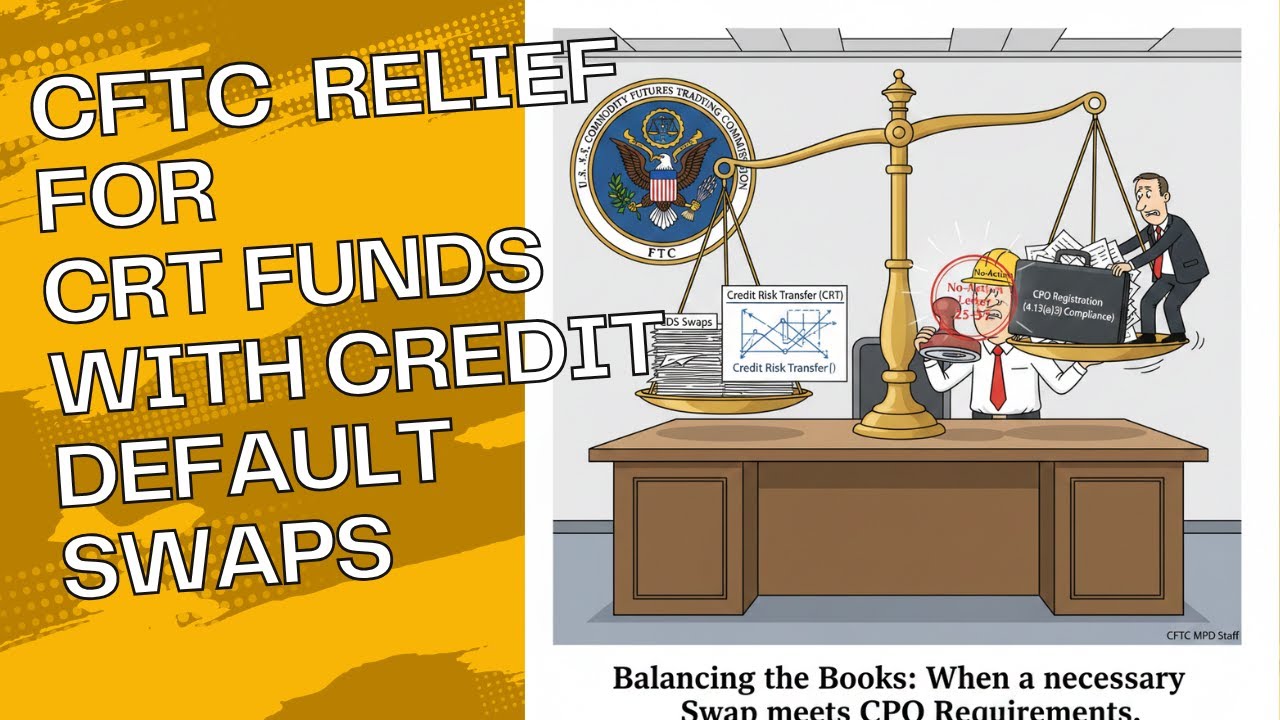

www.turnkeyfamilyoffice.com This video breaks down the CFTC Letter No. 25-37, issued on November 21, 2025, which grants a no-action position regarding the Commodity Pool Operator (CPO) registration requirement for certain participants in Credit Risk Transfer (CRT) transactions. What We Cover: The Request: The Structured Finance Association (SFA) requested that the CFTC's Market Participants Division (MPD) grant an exemption from CPO registration for SFA member financial institutions (SFA Banks), their affiliates, or others operating the Special Purpose Vehicles (SPVs) in CRT transactions. What are CRTs? These are risk-sharing transactions designed to transfer credit risk from SFA-member financial institutions (like national banks and bank holding companies) to voluntary sophisticated investors to manage balance sheet risks and obtain capital relief under prudential regulators' requirements. The Structure: A typical CRT involves an SPV issuing fixed-income, credit-linked notes to sophisticated investors and entering into a Credit Default Swap (CDS) or similar agreement with the SFA Bank. The notes' proceeds collateralize the SPV's obligations. The Exemption: The no-action position allows these operators to rely on the CPO registration exemption found in CFTC Regulation §4.13(a)(3), even though their disclosures may not strictly comply with the rule's "marketing prong". Key Conditions: The MPD's no-action position is subject to several conditions, including: The transaction must continually meet the requirements of CFTC Regulations §4.13(a)(3)(i)-(iii). The SPV's only commodity interest must be the CDS necessary for risk-sharing. Marketing materials must indicate the CPO is not registered with the Commission. The collateral must be highly liquid, cash, or cash-equivalent assets. Watch to understand how this no-action letter provides regulatory relief and clarifies the status of these complex risk-transfer arrangements! www.petersanchezguarda.com

Comments

-

3 недели назад

3 недели назад

-

1 месяц назад

1 месяц назад

-

8 дней назад

8 дней назад

-

4 года назад

4 года назад

-

3 месяца назад

3 месяца назад

-

Трансляция закончилась 2 часа назад

Трансляция закончилась 2 часа назад

-

2 года назад

2 года назад

-

1 год назад

1 год назад

-

3 месяца назад

3 месяца назад

-

20 часов назад

20 часов назад

-

2 недели назад

2 недели назад

-

1 день назад

1 день назад

-

Трансляция закончилась 2 дня назад

Трансляция закончилась 2 дня назад

-

7 дней назад

7 дней назад

-

1 день назад

1 день назад

-

2 года назад

2 года назад

-

3 месяца назад

3 месяца назад

-

1 месяц назад

1 месяц назад

-

13 дней назад

13 дней назад

-

2 месяца назад

2 месяца назад