Applied Econometrics: Panel Cointegration Estimation in EViews скачать в хорошем качестве

Applied Econometrics: Panel Cointegration Estimation in EViews

3 дня назад

Не удается загрузить Youtube-плеер. Проверьте блокировку Youtube в вашей сети.

Повторяем попытку...

Повторяем попытку...

Скачать видео с ютуб по ссылке или смотреть без блокировок на сайте: Applied Econometrics: Panel Cointegration Estimation in EViews в качестве 4k

У нас вы можете посмотреть бесплатно Applied Econometrics: Panel Cointegration Estimation in EViews или скачать в максимальном доступном качестве, видео которое было загружено на ютуб. Для загрузки выберите вариант из формы ниже:

-

Информация по загрузке:

Скачать mp3 с ютуба отдельным файлом. Бесплатный рингтон Applied Econometrics: Panel Cointegration Estimation in EViews в формате MP3:

Если кнопки скачивания не

загрузились

НАЖМИТЕ ЗДЕСЬ или обновите страницу

Если возникают проблемы со скачиванием видео, пожалуйста напишите в поддержку по адресу внизу

страницы.

Спасибо за использование сервиса ClipSaver.ru

Applied Econometrics: Panel Cointegration Estimation in EViews

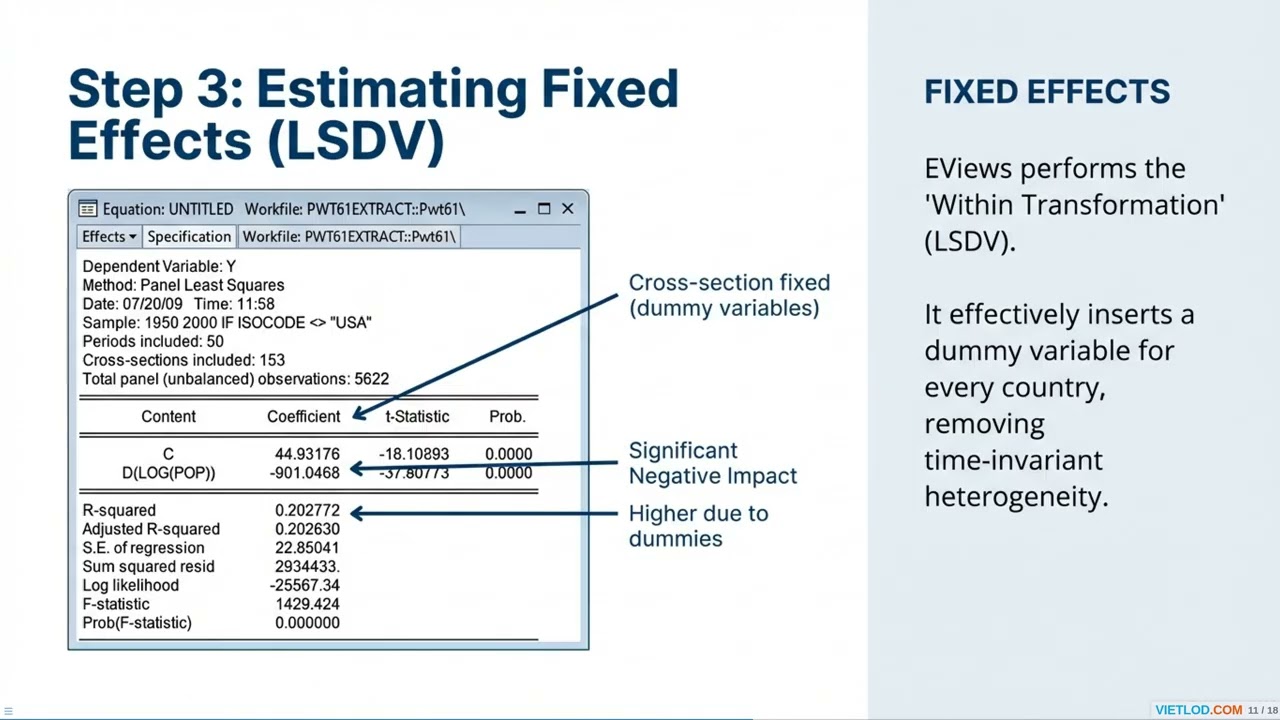

Panel Cointegration analyzes long-run equilibrium relationships among non-stationary variables. Combining time-series and cross-sectional dimensions helps overcome spurious regressions. EViews supports Fully Modified OLS (FMOLS) and Dynamic OLS (DOLS), producing asymptotically unbiased and normally distributed coefficient estimates. To perform this, your workfile must have a panel structure. Navigate to Quick/Estimate Equation, and choose COINTREG - Cointegrating Regression from the Method dropdown. Under the Equation specification tab, enter the dependent variable, cointegrating regressors, and define the deterministic trend (e.g., select Constant for fixed effects). Choose a panel method such as Pooled, Pooled (weighted), or Grouped mean. Adjust the lags/leads (for DOLS) or long-run variances if necessary, then click OK to estimate.

Comments