Applied Econometrics: OLS vs. Prais-Winsten vs. Newey-West скачать в хорошем качестве

Applied Econometrics: OLS vs. Prais-Winsten vs. Newey-West

5 дней назад

Не удается загрузить Youtube-плеер. Проверьте блокировку Youtube в вашей сети.

Повторяем попытку...

Повторяем попытку...

Скачать видео с ютуб по ссылке или смотреть без блокировок на сайте: Applied Econometrics: OLS vs. Prais-Winsten vs. Newey-West в качестве 4k

У нас вы можете посмотреть бесплатно Applied Econometrics: OLS vs. Prais-Winsten vs. Newey-West или скачать в максимальном доступном качестве, видео которое было загружено на ютуб. Для загрузки выберите вариант из формы ниже:

-

Информация по загрузке:

Скачать mp3 с ютуба отдельным файлом. Бесплатный рингтон Applied Econometrics: OLS vs. Prais-Winsten vs. Newey-West в формате MP3:

Если кнопки скачивания не

загрузились

НАЖМИТЕ ЗДЕСЬ или обновите страницу

Если возникают проблемы со скачиванием видео, пожалуйста напишите в поддержку по адресу внизу

страницы.

Спасибо за использование сервиса ClipSaver.ru

Applied Econometrics: OLS vs. Prais-Winsten vs. Newey-West

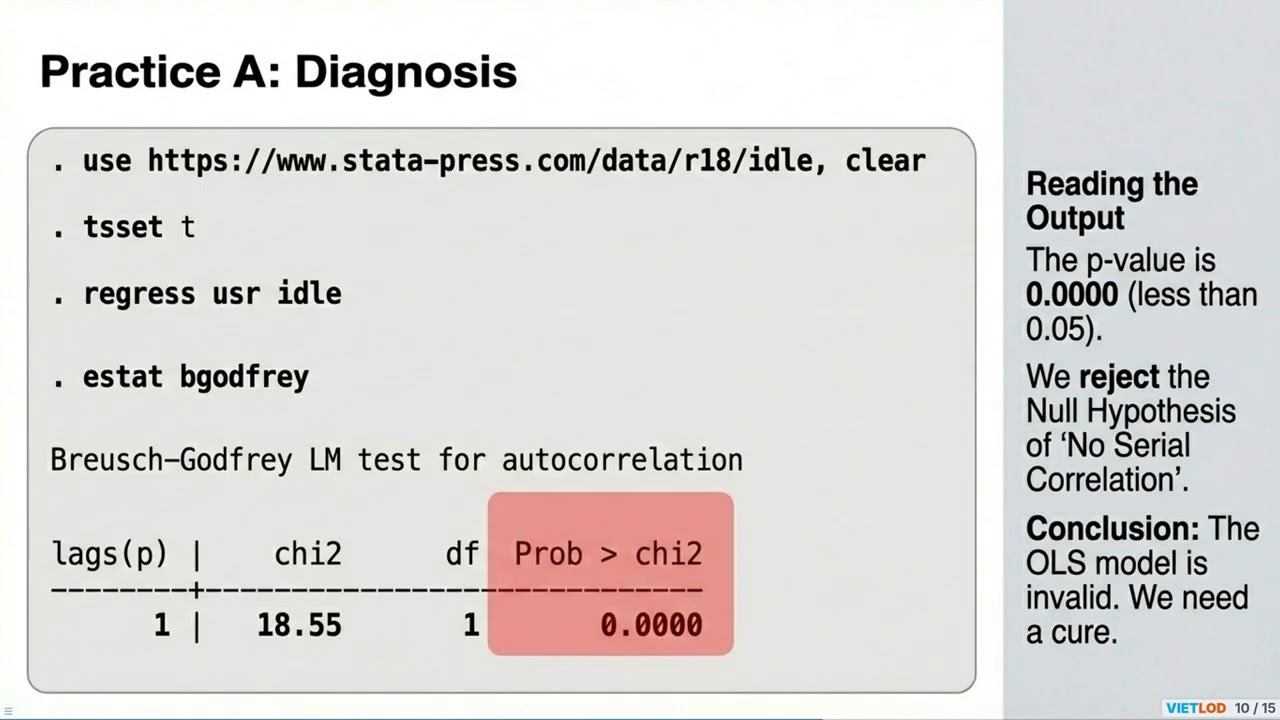

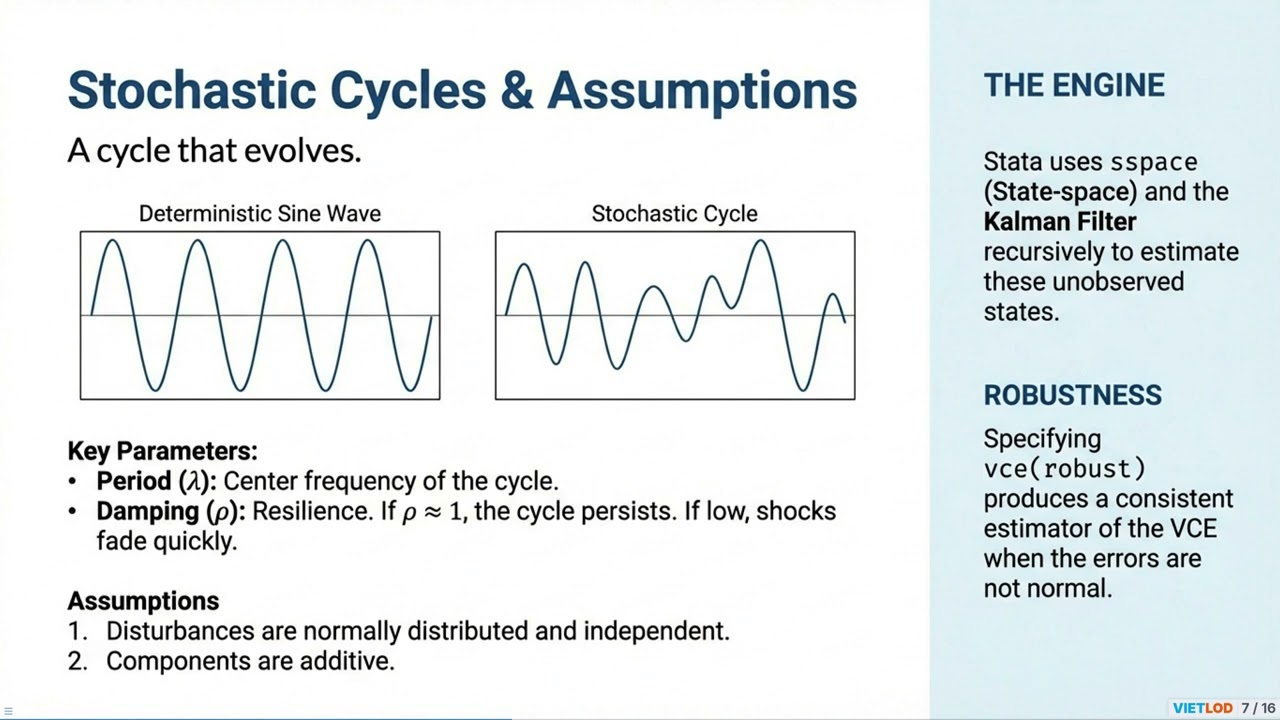

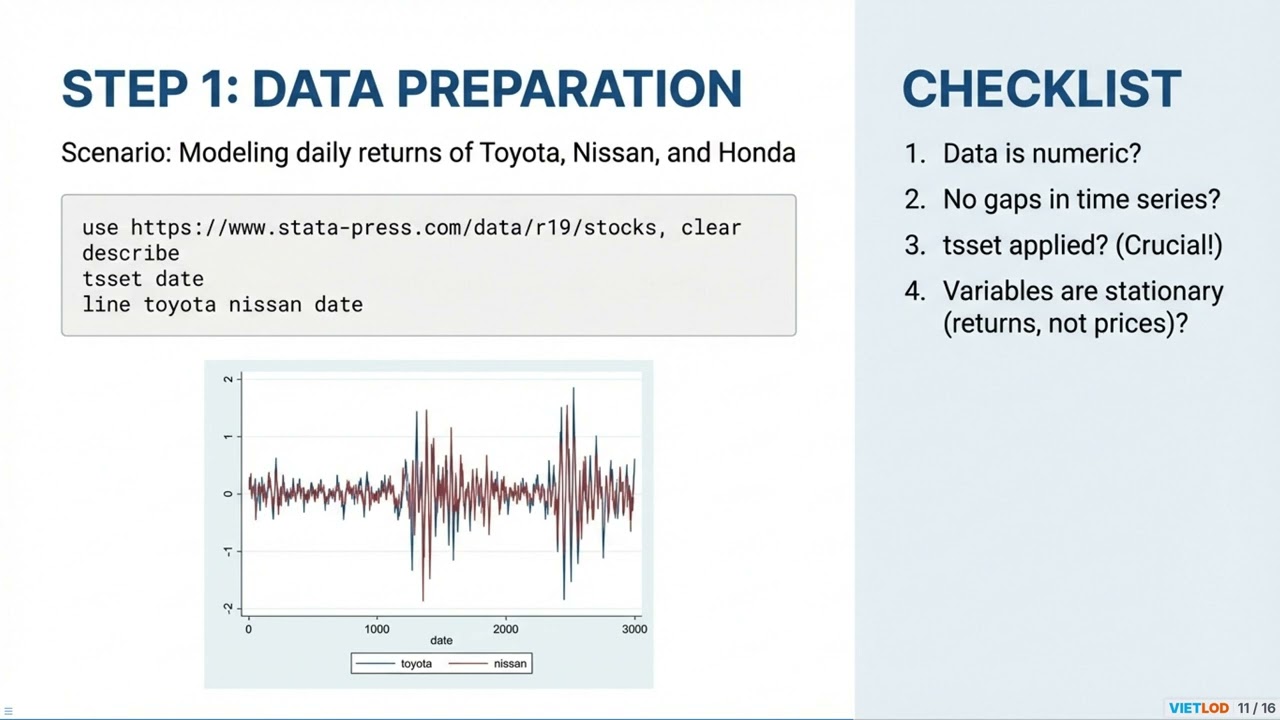

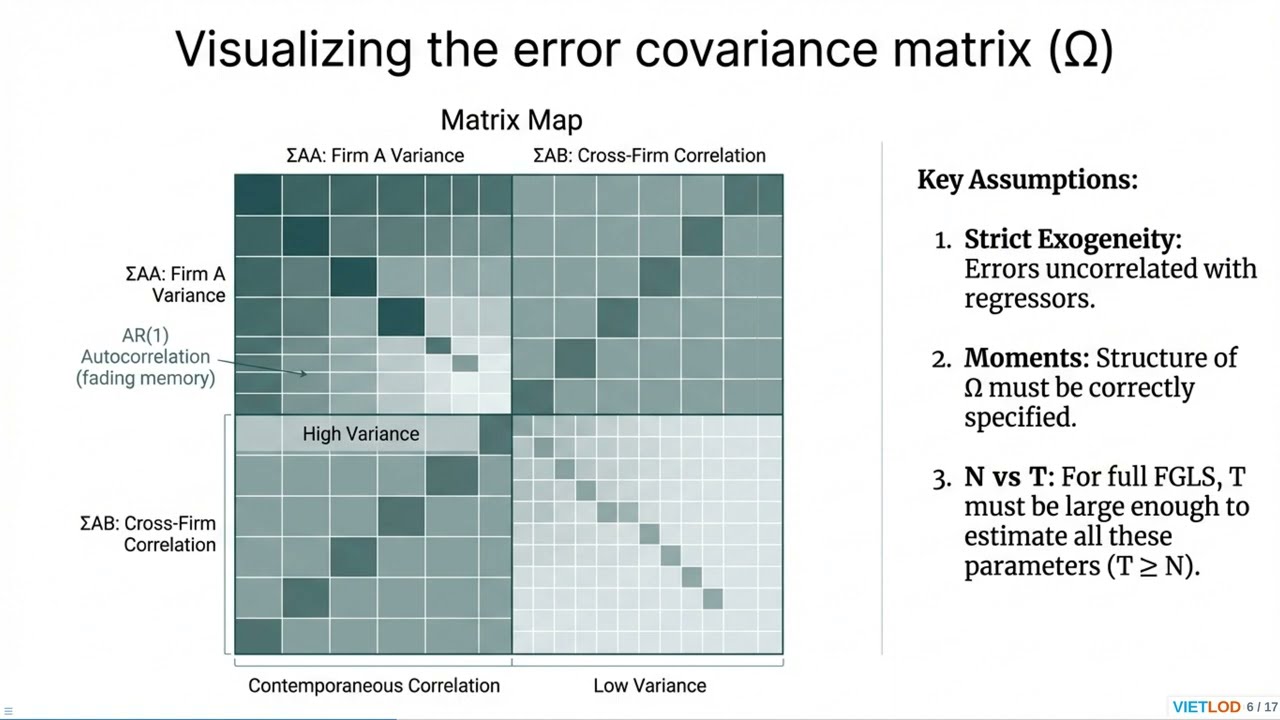

📝 Overview: This video presents core insights on Multivariate Garch in Stata: Modeling Volatility & Dynamic Correlations. We delve into hypothesis analysis and implementation methodologies. 📊 Detailed Content: AR1 Regression is an essential regression method for handling first-order autocorrelation in residuals, a common issue in time-series analysis. When model errors at the current time depend on past values, OLS estimates remain consistent, but standard errors become biased, rendering statistical tests unreliable. In Stata, the process begins by declaring data with tsset, followed by detecting autocorrelation using post-estimation commands such as estat dwatson (Durbin-Watson test) or estat bgodfrey. To address this, Stata provides powerful alternatives to OLS. The prais command implements Generalized Least Squares (GLS) estimation, allowing users to choose between the Prais-Winsten method or Cochrane-Orcutt (option corc). Prais-Winsten is often preferred as it preserves the first observation, offering a significant advantage in small samples. A more flexible approach uses the arima command (or ARMAX models) with the syntax arima y x, ar(1). This command employs maximum likelihood (ML) estimation for regression models with AR(1) disturbances. Alternatively, if researchers wish only to adjust standard errors while keeping OLS coefficients, the newey command provides Newey-West standard errors robust to autocorrelation and heteroskedasticity.

Comments

-

5 дней назад

5 дней назад

-

1 день назад

1 день назад

-

2 дня назад

2 дня назад

-

11 дней назад

11 дней назад

-

6 месяцев назад

6 месяцев назад

-

5 дней назад

5 дней назад

-

Трансляция закончилась 3 дня назад

Трансляция закончилась 3 дня назад

-

2 дня назад

2 дня назад

-

1 день назад

1 день назад

-

4 года назад

4 года назад

-

43 минуты назад

43 минуты назад

-

Трансляция закончилась 3 дня назад

Трансляция закончилась 3 дня назад

-

1 год назад

1 год назад

-

21 час назад

21 час назад

-

4 дня назад

4 дня назад

-

5 дней назад

5 дней назад

-

5 лет назад

5 лет назад

-

2 недели назад

2 недели назад

-

11 дней назад

11 дней назад

-

3 месяца назад

3 месяца назад