Unobserved Components Models: Extracting Stochastic Cycles скачать в хорошем качестве

Unobserved Components Models: Extracting Stochastic Cycles

5 дней назад

Не удается загрузить Youtube-плеер. Проверьте блокировку Youtube в вашей сети.

Повторяем попытку...

Повторяем попытку...

Скачать видео с ютуб по ссылке или смотреть без блокировок на сайте: Unobserved Components Models: Extracting Stochastic Cycles в качестве 4k

У нас вы можете посмотреть бесплатно Unobserved Components Models: Extracting Stochastic Cycles или скачать в максимальном доступном качестве, видео которое было загружено на ютуб. Для загрузки выберите вариант из формы ниже:

-

Информация по загрузке:

Скачать mp3 с ютуба отдельным файлом. Бесплатный рингтон Unobserved Components Models: Extracting Stochastic Cycles в формате MP3:

Если кнопки скачивания не

загрузились

НАЖМИТЕ ЗДЕСЬ или обновите страницу

Если возникают проблемы со скачиванием видео, пожалуйста напишите в поддержку по адресу внизу

страницы.

Спасибо за использование сервиса ClipSaver.ru

Unobserved Components Models: Extracting Stochastic Cycles

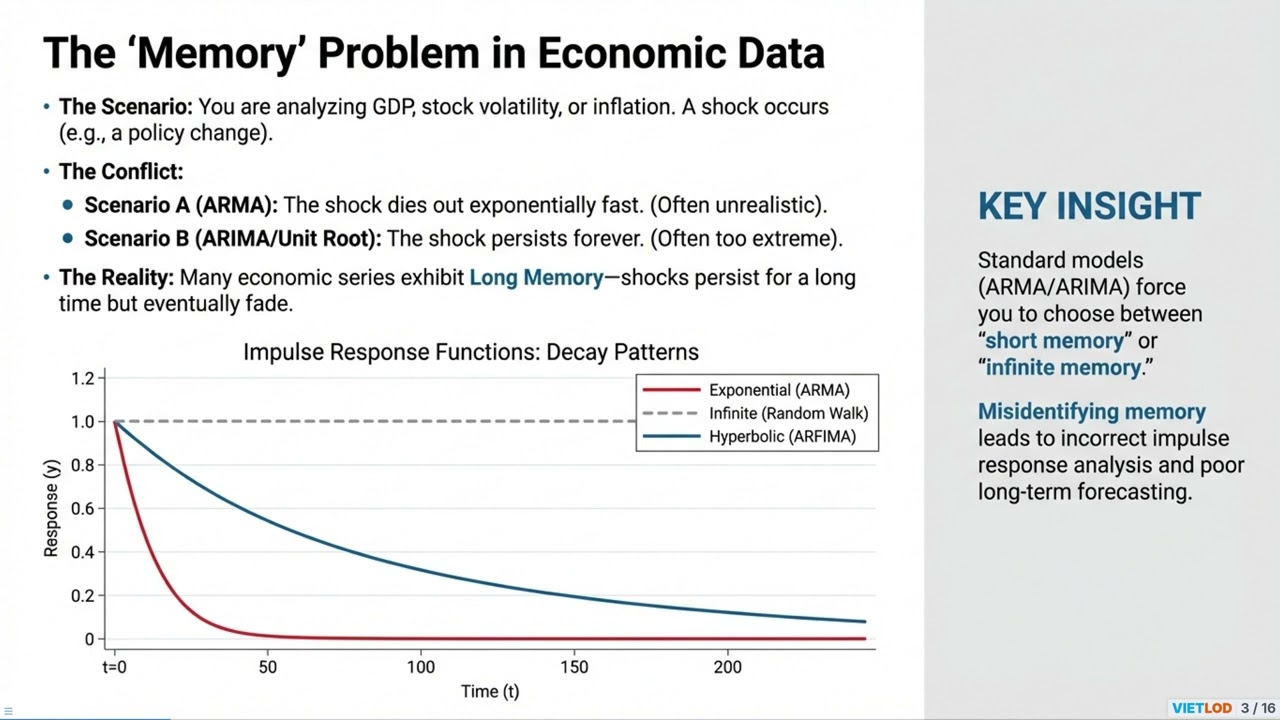

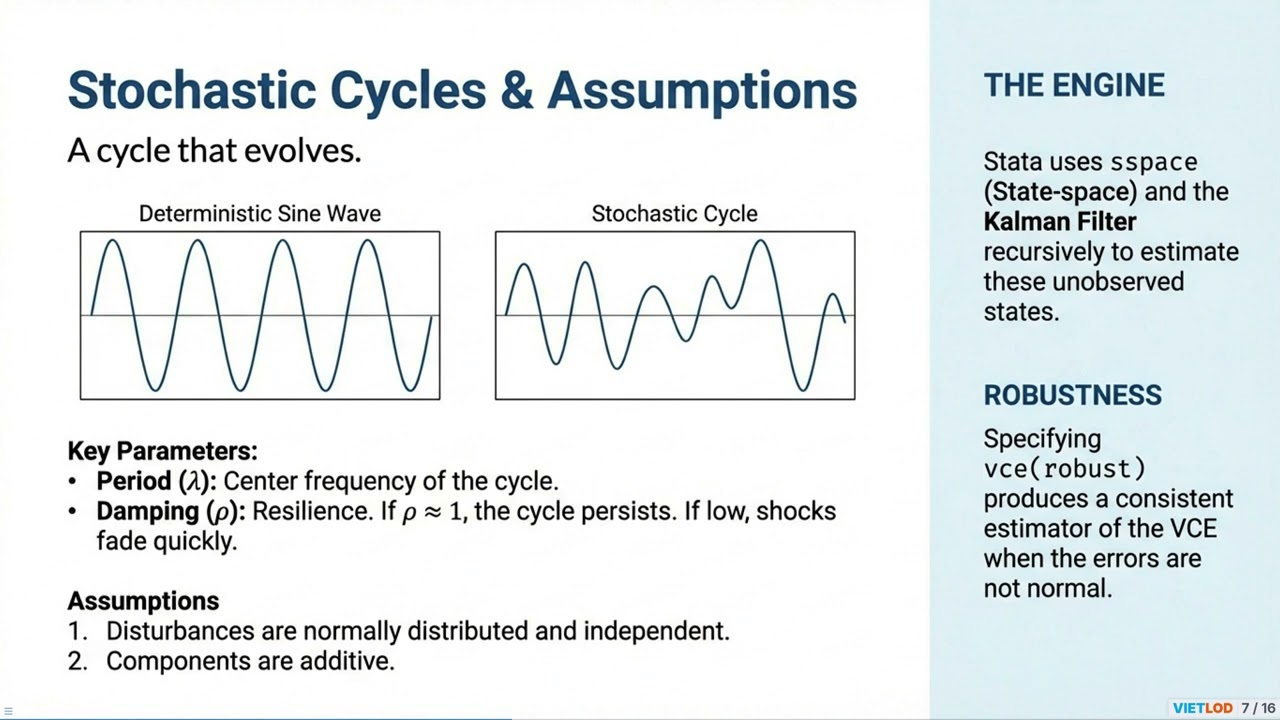

UCM Trend Cycle Decomposition is a structural time-series analysis method that decomposes a variable into unobserved components: trend, seasonal, cyclical , and idiosyncratic. In Stata, the ucm (Unobserved-Components Model) command estimates these parameters via maximum likelihood using state-space models,. Before implementation, data must be declared using the tsset command. The process begins by specifying the trend model structure. Stata offers various choices via the model() option, ranging from random walk (rwalk) and random walk with drift (rwdrift) to smooth trend (strend). A key strength of this command is the ability to model the stochastic cycle component following Harvey (1989) using the cycle() option. After estimation, researchers use the estat period command to convert the estimated frequency into a specific time period length, facilitating interpretation. Most importantly, the predict command allows for the extraction of separate series such as trend and cycle for further analysis or visualizing economic fluctuations. Additionally, the psdensity command estimates the spectral density to evaluate the importance of different frequency components within the model ❤️ THANK YOU FOR WATCHING Follow Vietlod for more insightful bite-sized knowledge every day!

Comments