Causal Inference Beyond the Mean: Mastering IV Quantile Regression (ivqregress) in Stata скачать в хорошем качестве

Causal Inference Beyond the Mean: Mastering IV Quantile Regression (ivqregress) in Stata

2 недели назад

Не удается загрузить Youtube-плеер. Проверьте блокировку Youtube в вашей сети.

Повторяем попытку...

Повторяем попытку...

Скачать видео с ютуб по ссылке или смотреть без блокировок на сайте: Causal Inference Beyond the Mean: Mastering IV Quantile Regression (ivqregress) in Stata в качестве 4k

У нас вы можете посмотреть бесплатно Causal Inference Beyond the Mean: Mastering IV Quantile Regression (ivqregress) in Stata или скачать в максимальном доступном качестве, видео которое было загружено на ютуб. Для загрузки выберите вариант из формы ниже:

-

Информация по загрузке:

Скачать mp3 с ютуба отдельным файлом. Бесплатный рингтон Causal Inference Beyond the Mean: Mastering IV Quantile Regression (ivqregress) in Stata в формате MP3:

Если кнопки скачивания не

загрузились

НАЖМИТЕ ЗДЕСЬ или обновите страницу

Если возникают проблемы со скачиванием видео, пожалуйста напишите в поддержку по адресу внизу

страницы.

Спасибо за использование сервиса ClipSaver.ru

Causal Inference Beyond the Mean: Mastering IV Quantile Regression (ivqregress) in Stata

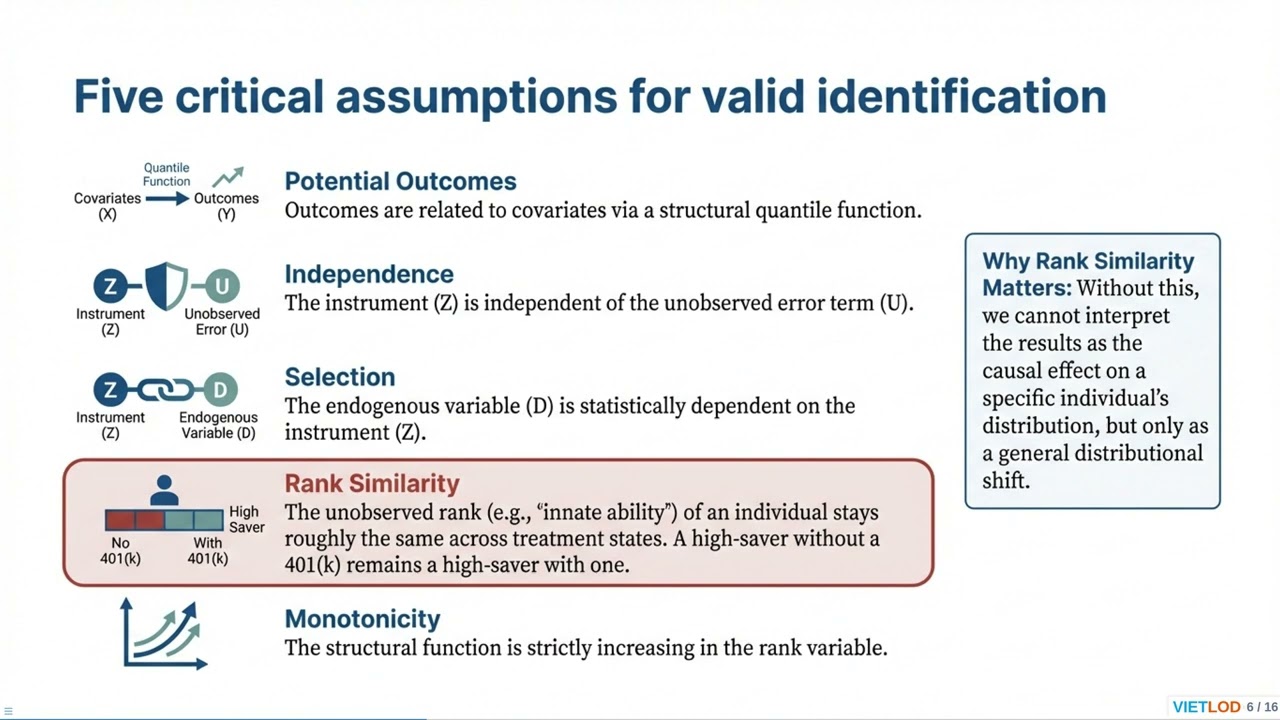

Instrumental-variable quantile regression (IVQR) is a sophisticated econometric method designed to identify structural causal effects across the entire distribution of an outcome variable when regressors are endogenous. Unlike standard quantile regression, which yields inconsistent estimates under endogeneity, or Two-Stage Least Squares (2SLS), which focuses solely on average effects, IVQR leverages instrumental variables to uncover heterogeneous impacts. By relying on rank similarity assumptions—where an individual's rank in the potential outcome distribution remains stable across treatment states—IVQR allows researchers to determine, for instance, if an education policy benefits low-income earners differently than high-income ones. Stata 18 revolutionized this analysis with the official ivqregress command, offering two distinct estimators. The Inverse Quantile Regression (iqr) estimator employs a robust grid-search algorithm. While computationally intensive, it allows for inference that remains valid even with weak instruments using the post-estimation command estat dualci. For models with multiple endogenous regressors, the Smoothed Estimating Equations (smooth) estimator applies kernel smoothing to the objective function, enabling faster gradient-based optimization. The syntax follows the familiar IV pattern: ivqregress iqr depvar exovars (endovars = instruments). For specialized data structures, community commands like mmqreg (for panel fixed effects) and cqiv (for censored data) remain valuable alternatives. Stata also provides powerful post-estimation tools; estat endogeffects tests hypotheses like dominance or constant effects, while estat coefplot generates visual evidence of how coefficients evolve across the quantile index How to Conduct Endogeneity in Quantile Regression Standard quantile regression yields inconsistent estimates when regressors are endogenous. To address this, researchers typically employ Instrumental Variable Quantile Regression (IVQR), which identifies structural quantile effects by utilizing instruments that influence the endogenous variable but remain independent of the outcome's rank error. The IVQR framework, notably developed by Chernozhukov and Hansen, relies on rank similarity assumptions to recover causal effects across the entire distribution. In Stata, the official ivqregress command provides a comprehensive toolkit for this analysis. Users can select the Inverse Quantile Regression (iqr) estimator, which employs a grid-search algorithm and offers inference robust to weak instruments, making it suitable for models with a single endogenous variable. Alternatively, the Smoothed Estimating Equations (smooth) estimator uses gradient-based optimization, offering superior computational speed and the ability to handle multiple endogenous regressors. Alternative approaches exist for specific data structures. The cqiv command handles censored dependent variables using a control function approach within a triangular model framework. For binary treatments where interest lies in the "complier" subpopulation, ivqte estimates Local Quantile Treatment Effects. Finally, for panel data requiring the control of individual fixed effects, the mmqreg command implements Method of Moments Quantile Regression. Comparing IQR and SEE Estimators in ivqregress The Inverse Quantile Regression (IQR) estimator employs a grid-search algorithm to solve the objective function. Its primary advantage is providing inference robust to weak instruments through dual confidence intervals, though it is computationally intensive and restricted to a single endogenous variable. Conversely, the Smoothed Estimating Equations (SEE) estimator uses kernel smoothing to enable faster gradient-based optimization. While SEE efficiently handles multiple endogenous regressors, it lacks the weak-instrument robust inference capabilities found in the IQR estimator.

Comments

![Цепи Маркова — математика предсказаний [Veritasium]](https://imager.clipsaver.ru/QI7oUwNrQ34/max.jpg)