ARFIMA Tutorial: Fractional Integration and Spectral Analysis with psdensity скачать в хорошем качестве

ARFIMA Tutorial: Fractional Integration and Spectral Analysis with psdensity

7 дней назад

Не удается загрузить Youtube-плеер. Проверьте блокировку Youtube в вашей сети.

Повторяем попытку...

Повторяем попытку...

Скачать видео с ютуб по ссылке или смотреть без блокировок на сайте: ARFIMA Tutorial: Fractional Integration and Spectral Analysis with psdensity в качестве 4k

У нас вы можете посмотреть бесплатно ARFIMA Tutorial: Fractional Integration and Spectral Analysis with psdensity или скачать в максимальном доступном качестве, видео которое было загружено на ютуб. Для загрузки выберите вариант из формы ниже:

-

Информация по загрузке:

Скачать mp3 с ютуба отдельным файлом. Бесплатный рингтон ARFIMA Tutorial: Fractional Integration and Spectral Analysis with psdensity в формате MP3:

Если кнопки скачивания не

загрузились

НАЖМИТЕ ЗДЕСЬ или обновите страницу

Если возникают проблемы со скачиванием видео, пожалуйста напишите в поддержку по адресу внизу

страницы.

Спасибо за использование сервиса ClipSaver.ru

ARFIMA Tutorial: Fractional Integration and Spectral Analysis with psdensity

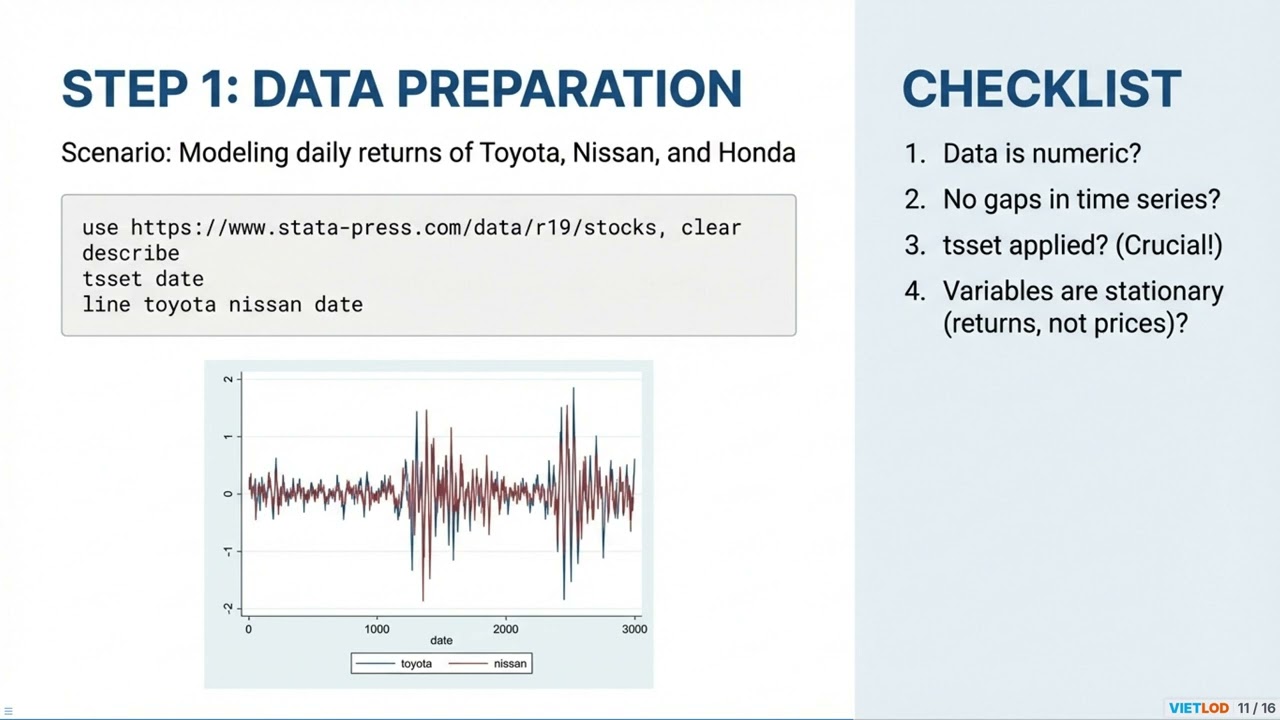

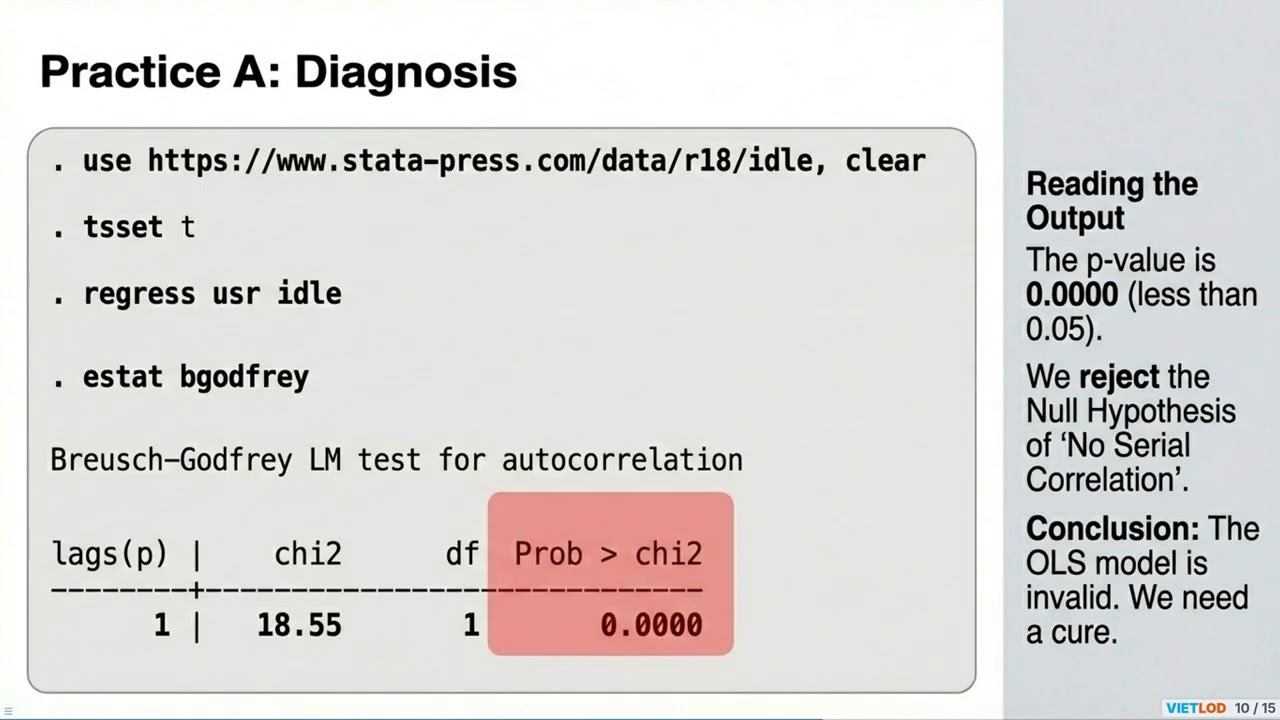

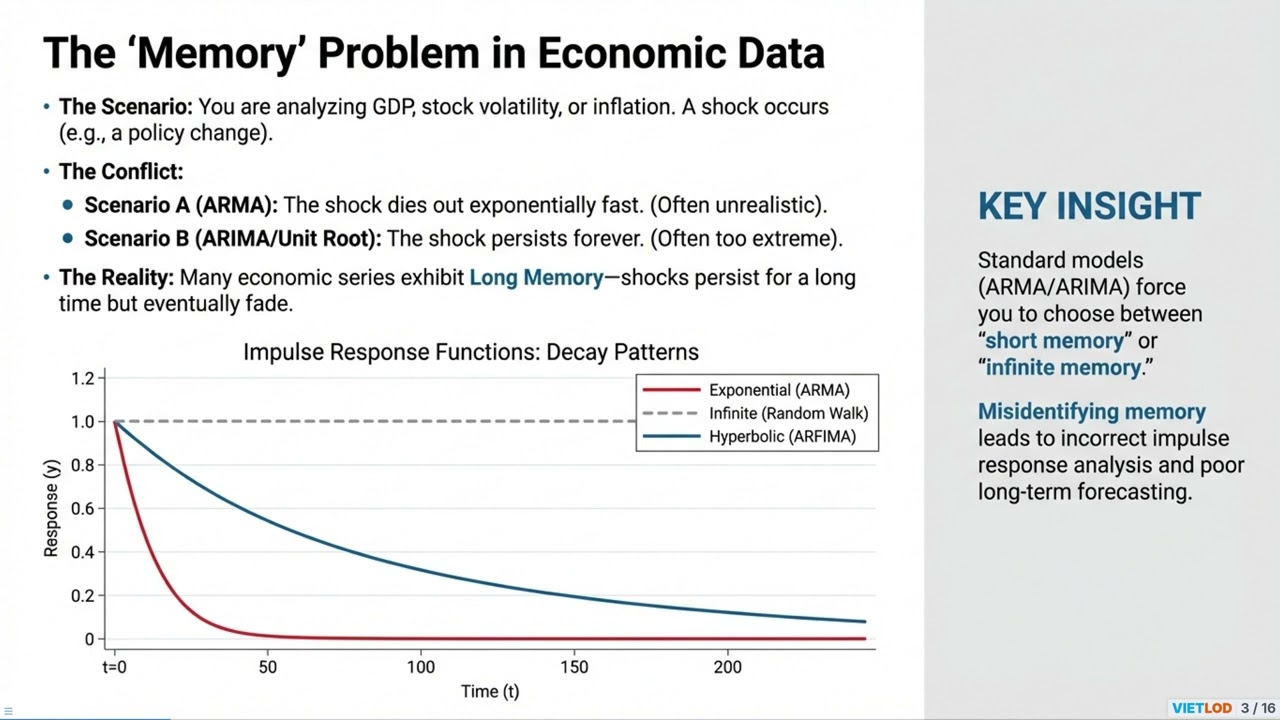

ARFIMA Models (Autoregressive Fractionally Integrated Moving Average) are powerful tools for analyzing "long-memory" time series, where the autocorrelation function decays very slowly over time. Unlike traditional ARIMA models which require integer integration orders (typically 0 or 1), ARFIMA allows the integration parameter d to be a real number (usually between -0.5 and 0.5). This generalization offers flexibility in modeling processes that are neither fully stationary nor pure random walks, effectively separating long-run effects (d) from short-run dynamics (ARMA). The implementation process in Stata mandates declaring time-series data using tsset. To determine the optimal model structure, the arfimasoc command is invaluable, reporting information criteria such as AIC, BIC, and HQIC for various AR and MA lags. The primary command arfima estimates parameters using maximum likelihood (MLE) or modified profile likelihood (MPL) to reduce bias in small samples,. Users can customize short-run structures via the ar() and ma() options. Following estimation, the predict command allows for forecasting the fractionally differenced series (fdifference) or standardized residuals, while psdensity and estat acplot assist in analyzing spectral density and autocorrelation functions to evaluate model fit ❤️ THANK YOU FOR WATCHING Follow Vietlod for more insightful bite-sized knowledge every day!

Comments