Handling Model Uncertainty: Bayesian Model Averaging (BMA) with Stata скачать в хорошем качестве

Handling Model Uncertainty: Bayesian Model Averaging (BMA) with Stata

2 недели назад

Не удается загрузить Youtube-плеер. Проверьте блокировку Youtube в вашей сети.

Повторяем попытку...

Повторяем попытку...

Скачать видео с ютуб по ссылке или смотреть без блокировок на сайте: Handling Model Uncertainty: Bayesian Model Averaging (BMA) with Stata в качестве 4k

У нас вы можете посмотреть бесплатно Handling Model Uncertainty: Bayesian Model Averaging (BMA) with Stata или скачать в максимальном доступном качестве, видео которое было загружено на ютуб. Для загрузки выберите вариант из формы ниже:

-

Информация по загрузке:

Скачать mp3 с ютуба отдельным файлом. Бесплатный рингтон Handling Model Uncertainty: Bayesian Model Averaging (BMA) with Stata в формате MP3:

Если кнопки скачивания не

загрузились

НАЖМИТЕ ЗДЕСЬ или обновите страницу

Если возникают проблемы со скачиванием видео, пожалуйста напишите в поддержку по адресу внизу

страницы.

Спасибо за использование сервиса ClipSaver.ru

Handling Model Uncertainty: Bayesian Model Averaging (BMA) with Stata

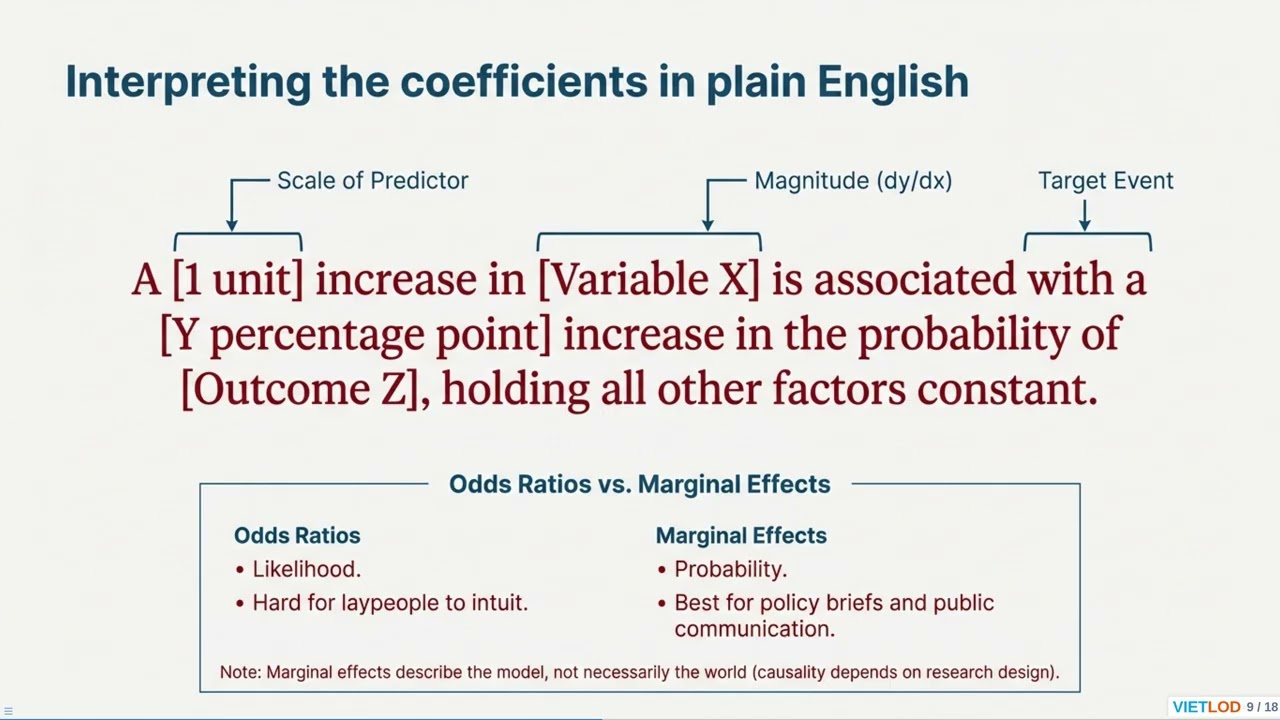

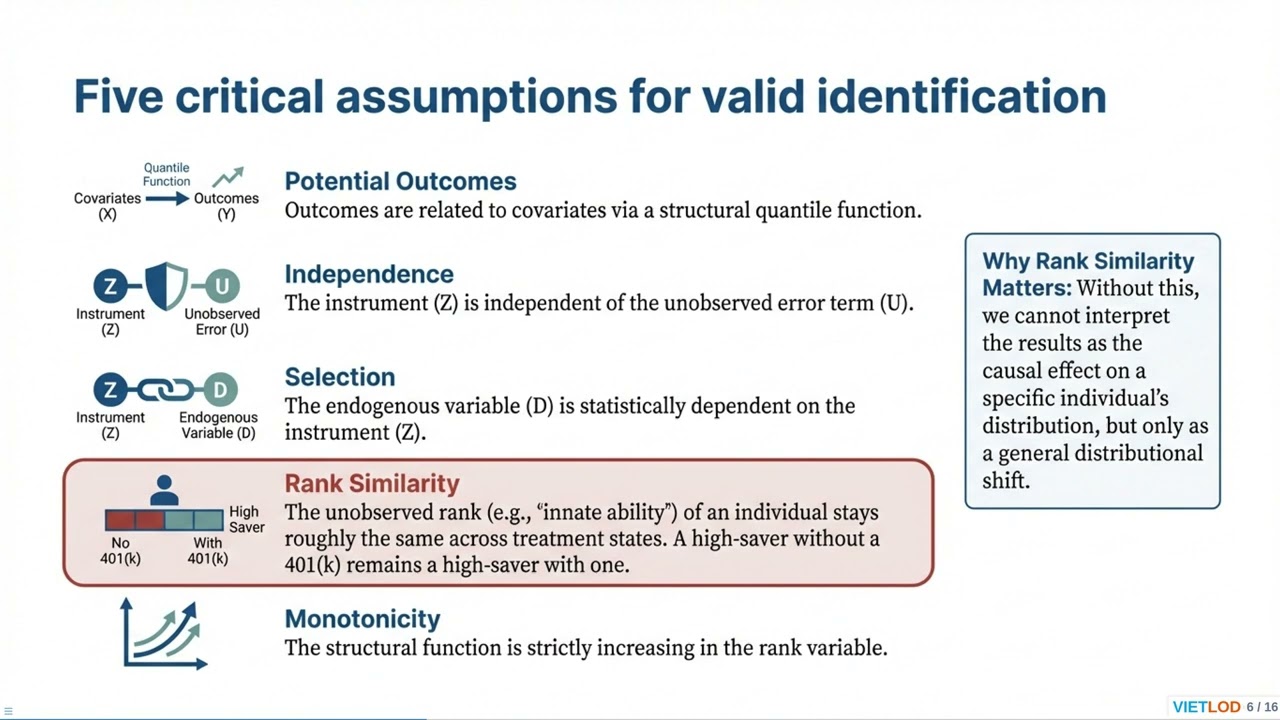

Bayesian estimation is a statistical paradigm where model parameters are treated as random quantities, a fundamental shift from the frequentist view of fixed constants. By applying Bayes' theorem, researchers combine prior knowledge—formulated as prior distributions—with the likelihood of observed data to derive a posterior distribution. This framework allows for intuitive probabilistic interpretations, such as determining the probability that a parameter falls within a specific credible interval, and proves particularly robust in small-sample contexts where asymptotic assumptions may fail. Stata offers a comprehensive suite for performing this analysis. The most accessible method is the bayes: prefix; simply placing it before standard estimation commands (e.g., bayes: regress or bayes: logit) fits the model using default priors and MCMC methods. For more complex, nonlinear, or custom models, the bayesmh command provides granular control over likelihood functions and prior specifications using Adaptive Metropolis-Hastings or Gibbs sampling. Crucially, Stata facilitates the necessary "Bayesian workflow," including convergence diagnostics via bayesgraph to ensure MCMC stability and posterior summaries via bayesstats summary. Advanced users can also leverage bayesstats ic for model comparison using Bayes factors, bayespredict for posterior predictive checks, and sophisticated features like bmaregress for Bayesian Model Averaging to rigorously account for model uncertainty. How to Choose and Test Prior Distributions in Stata: From Defaults to Sensitivity Analysis Choosing the right prior distribution in Stata depends on the availability of prior information and the specific goals of your analysis. For standard regression tasks where you lack strong prior beliefs, Stata's bayes: prefix conveniently assigns default noninformative or weakly informative priors, such as Normal(0, 10000) for coefficients and Inverse-Gamma(0.01, 0.01) for variances. These defaults are designed to let the observed data dominate the posterior estimation. When you have specific domain knowledge or results from historical data, you should use the prior() option with bayesmh or the bayes: prefix to specify informative priors, such as a Normal distribution with a specific mean and smaller variance. For advanced modeling focused on variable selection, Stata offers specialized global-local shrinkage priors like the Horseshoe or Bayesian Lasso through the bayesselect command, or Zellner's g-priors within bmaregress to handle model uncertainty. Regardless of the initial choice, best practice dictates performing a sensitivity analysis—systematically varying prior hyperparameters to verify that your substantive conclusions remain robust and are not driven solely by subjective assumptions.

Comments

-

5 часов назад

5 часов назад

-

2 недели назад

2 недели назад

-

1 год назад

1 год назад

-

1 день назад

1 день назад

-

Трансляция закончилась 23 часа назад

Трансляция закончилась 23 часа назад

-

22 часа назад

22 часа назад

-

2 недели назад

2 недели назад

-

Трансляция закончилась 2 дня назад

Трансляция закончилась 2 дня назад

-

4 года назад

4 года назад

-

Трансляция закончилась 18 часов назад

Трансляция закончилась 18 часов назад

-

1 день назад

1 день назад

-

11 дней назад

11 дней назад

-

Трансляция закончилась 3 дня назад

Трансляция закончилась 3 дня назад

-

10 месяцев назад

10 месяцев назад

-

2 недели назад

2 недели назад

-

5 месяцев назад

5 месяцев назад

-

5 дней назад

5 дней назад

-

2 недели назад

2 недели назад

-

3 месяца назад

3 месяца назад

-

3 месяца назад

3 месяца назад