Скачать с ютуб Convexity adjustment for Eurodollar futures в хорошем качестве

Convexity adjustment for Eurodollar futures

16 лет назад

Скачать бесплатно и смотреть ютуб-видео без блокировок Convexity adjustment for Eurodollar futures в качестве 4к (2к / 1080p)

У нас вы можете посмотреть бесплатно Convexity adjustment for Eurodollar futures или скачать в максимальном доступном качестве, которое было загружено на ютуб. Для скачивания выберите вариант из формы ниже:

Загрузить музыку / рингтон Convexity adjustment for Eurodollar futures в формате MP3:

Если кнопки скачивания не

загрузились

НАЖМИТЕ ЗДЕСЬ или обновите страницу

Если возникают проблемы со скачиванием, пожалуйста напишите в поддержку по адресу внизу

страницы.

Спасибо за использование сервиса ClipSaver.ru

Convexity adjustment for Eurodollar futures

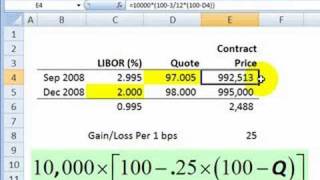

A key difference between a futures contract and a forward contract is daily settlement: the instrument is daily marked-to-market. If the value of the futures increases, this creates excess margin cash; if value declines, there will be a margin call (when the maintenance level is reached). Therefore, a Eurodollar futures contract has more volatility than a similar forward rate agreement (FRA). This implies a slightly higher rate.

Comments