Multiple Equation Analysis: System Estimation & Var Modeling скачать в хорошем качестве

Multiple Equation Analysis: System Estimation & Var Modeling

13 дней назад

Не удается загрузить Youtube-плеер. Проверьте блокировку Youtube в вашей сети.

Повторяем попытку...

Повторяем попытку...

Скачать видео с ютуб по ссылке или смотреть без блокировок на сайте: Multiple Equation Analysis: System Estimation & Var Modeling в качестве 4k

У нас вы можете посмотреть бесплатно Multiple Equation Analysis: System Estimation & Var Modeling или скачать в максимальном доступном качестве, видео которое было загружено на ютуб. Для загрузки выберите вариант из формы ниже:

-

Информация по загрузке:

Скачать mp3 с ютуба отдельным файлом. Бесплатный рингтон Multiple Equation Analysis: System Estimation & Var Modeling в формате MP3:

Если кнопки скачивания не

загрузились

НАЖМИТЕ ЗДЕСЬ или обновите страницу

Если возникают проблемы со скачиванием видео, пожалуйста напишите в поддержку по адресу внизу

страницы.

Спасибо за использование сервиса ClipSaver.ru

Multiple Equation Analysis: System Estimation & Var Modeling

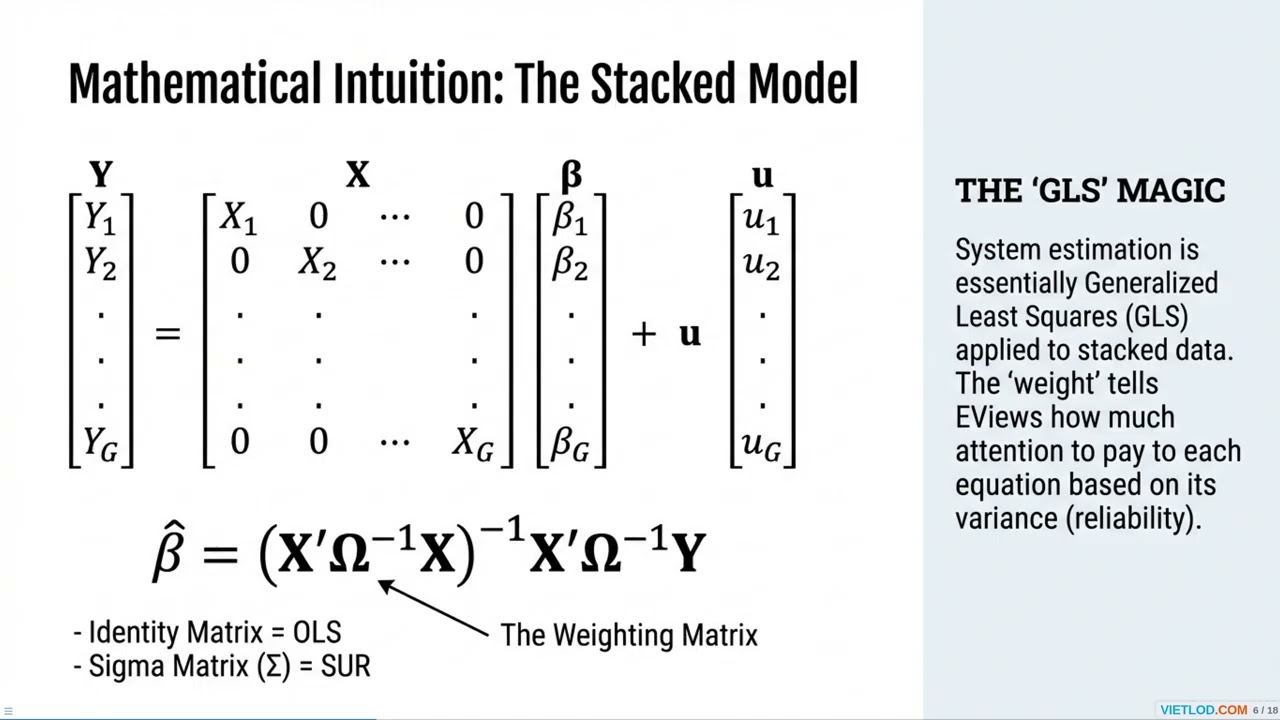

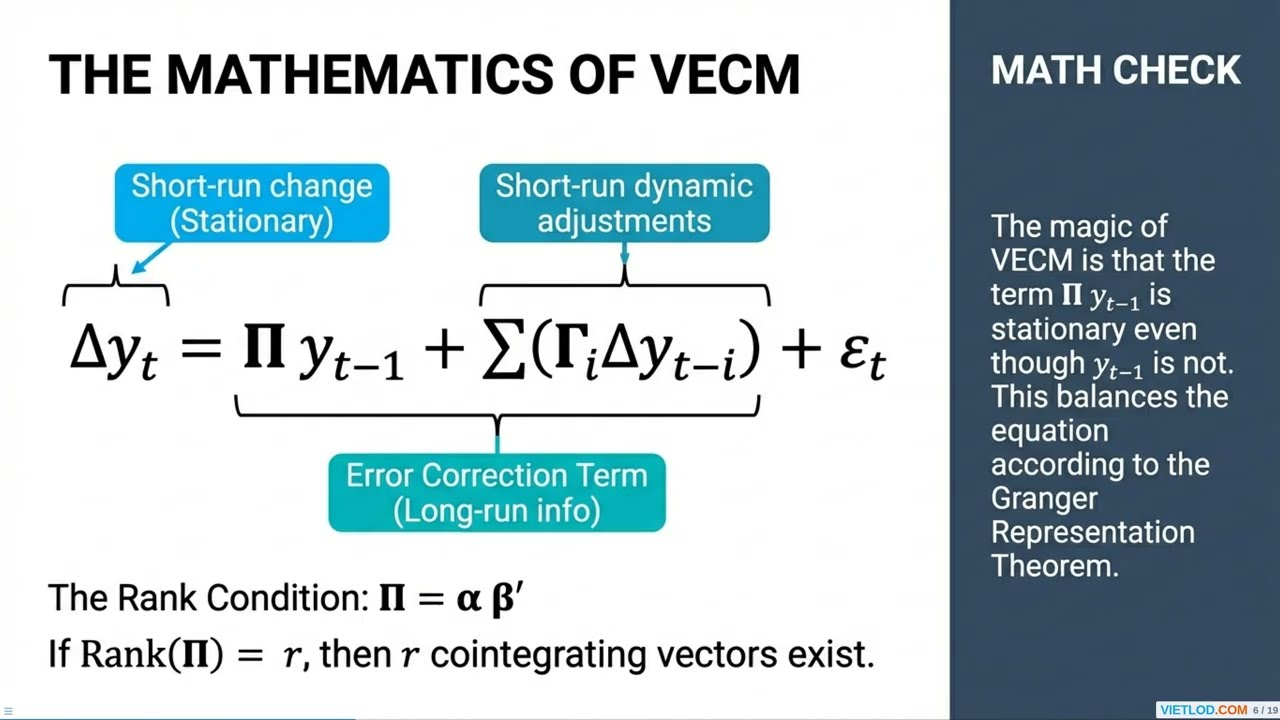

Welcome to our presentation on Multiple Equation Analysis, focusing on system estimation and Vector Autoregression modeling in EViews. As the EViews User Guide highlights, the structural approach uses economic theory to model the relationships among variables. This allows us to understand how different economic factors interact within a system rather than in isolation. We'll explore the methodologies and practical application using EViews. In the real world, economic variables are deeply interconnected and rarely move in isolation. For example, GDP influences interest rates, but interest rates also influence GDP. A major limitation of standard single-equation O-L-S is its assumption that predictors are exogenous, meaning they are not influenced by the dependent variable. This is often violated in macroeconomics. The solution is system estimation, such as a V-A-R model, which treats all variables as endogenous, acknowledging their mutual influence. In macroeconomics, variables are often both independent and dependent. V-A-Rs, or Vector Autoregressions, sidestep identification problems by treating every endogenous variable as a function of the lagged values of all endogenous variables in the system. This decision matrix provides a clear roadmap for selecting the appropriate time series model when working with multiple time series data. The first critical question to address is whether your data is stationary. As the decision logic highlights, stationarity is essential for the stability of a standard Vector Autoregression, or VAR, model. If your data is indeed stationary,... #eviews #timesseries

Comments

-

4 дня назад

4 дня назад

-

Трансляция закончилась 5 дней назад

Трансляция закончилась 5 дней назад

-

13 дней назад

13 дней назад

-

10 дней назад

10 дней назад

-

6 дней назад

6 дней назад

-

13 дней назад

13 дней назад

-

12 дней назад

12 дней назад

-

4 дня назад

4 дня назад

-

2 часа назад

2 часа назад

-

2 дня назад

2 дня назад

-

Трансляция закончилась 7 дней назад

Трансляция закончилась 7 дней назад

-

5 часов назад

5 часов назад

-

1 месяц назад

1 месяц назад

-

10 дней назад

10 дней назад

-

13 дней назад

13 дней назад

-

4 дня назад

4 дня назад

-

13 дней назад

13 дней назад

-

6 дней назад

6 дней назад

-

5 дней назад

5 дней назад

-

11 дней назад

11 дней назад