Internal Control: Revenue Cycle - Lesson 2 скачать в хорошем качестве

Internal Control: Revenue Cycle - Lesson 2

10 лет назад

Не удается загрузить Youtube-плеер. Проверьте блокировку Youtube в вашей сети.

Повторяем попытку...

Повторяем попытку...

Скачать видео с ютуб по ссылке или смотреть без блокировок на сайте: Internal Control: Revenue Cycle - Lesson 2 в качестве 4k

У нас вы можете посмотреть бесплатно Internal Control: Revenue Cycle - Lesson 2 или скачать в максимальном доступном качестве, видео которое было загружено на ютуб. Для загрузки выберите вариант из формы ниже:

-

Информация по загрузке:

Скачать mp3 с ютуба отдельным файлом. Бесплатный рингтон Internal Control: Revenue Cycle - Lesson 2 в формате MP3:

Если кнопки скачивания не

загрузились

НАЖМИТЕ ЗДЕСЬ или обновите страницу

Если возникают проблемы со скачиванием видео, пожалуйста напишите в поддержку по адресу внизу

страницы.

Спасибо за использование сервиса ClipSaver.ru

Internal Control: Revenue Cycle - Lesson 2

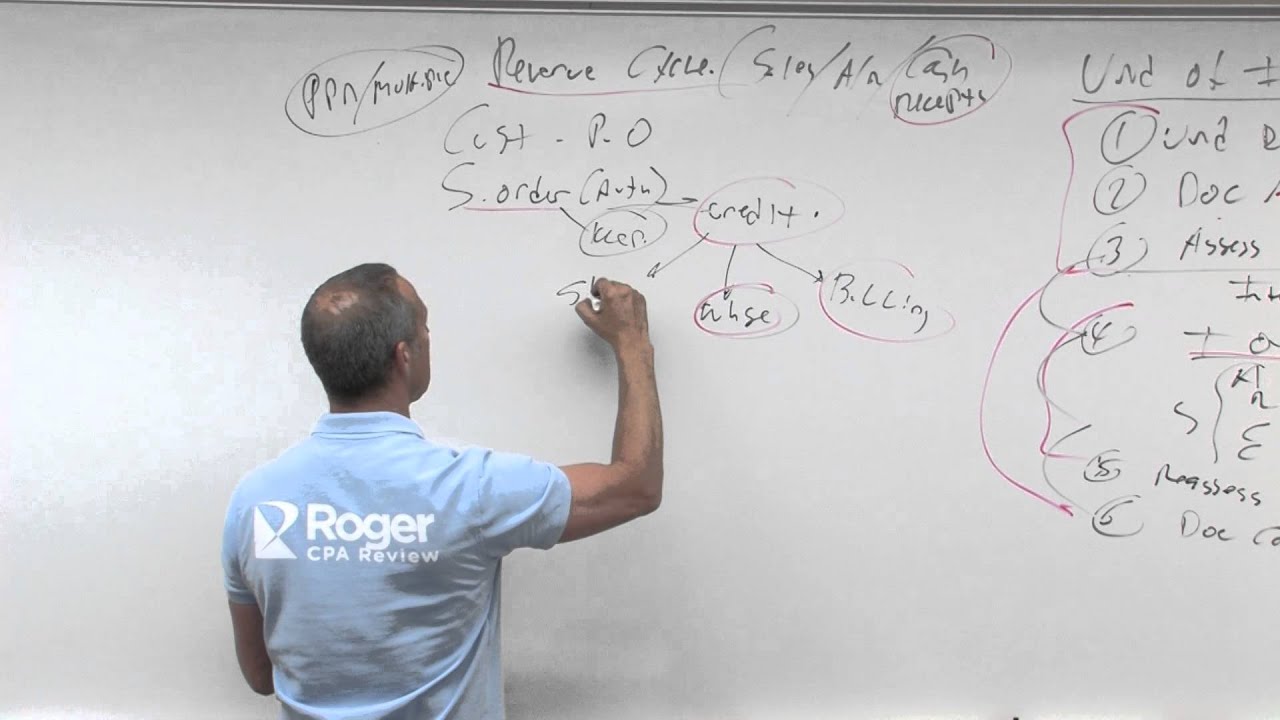

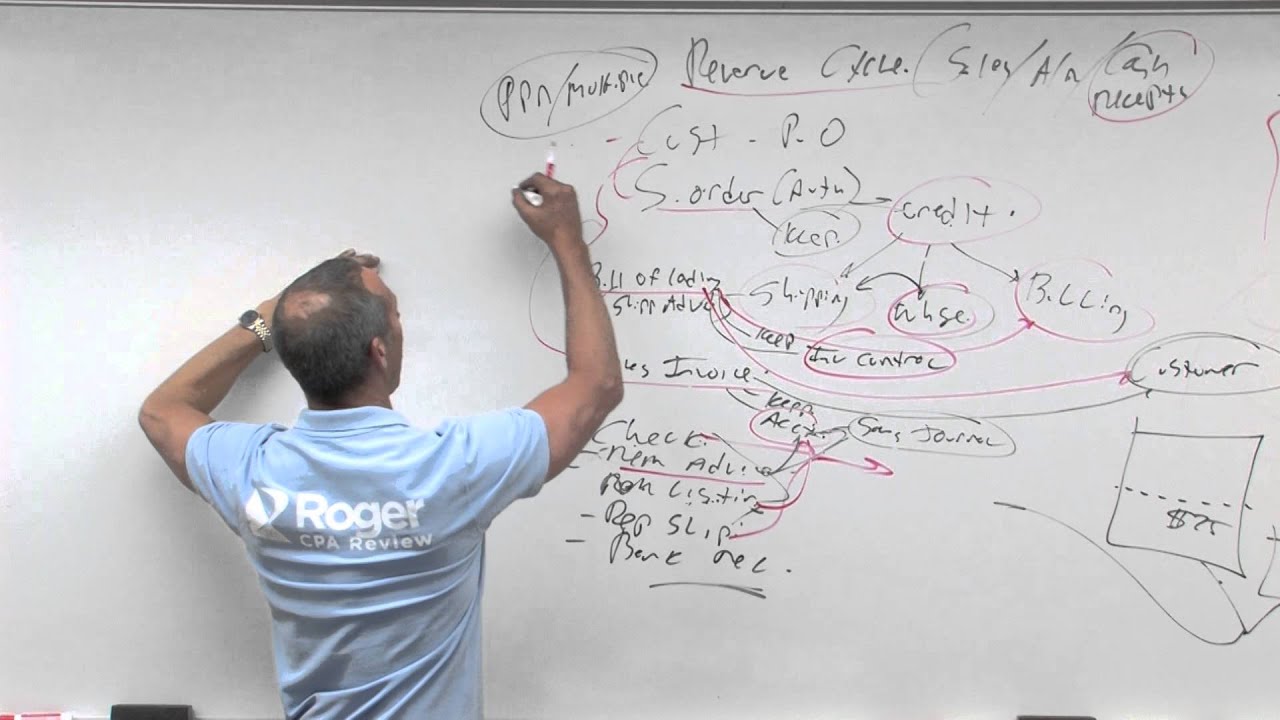

In this video, 3.06 – Internal Control – Revenue Cycle – Lesson 2, Roger Philipp, CPA, CGMA, discusses how controls have a function of either preventing material misstatements in the financial statements before they occur, or detecting and correcting misstatements that have already occurred. Preventive controls are most effective, but are generally more expensive to implement. Controls that detect and correct misstatements are less expensive to implement but may detect material misstatements too late. If an auditor chooses to rely on internal control during an audit, the auditor must conduct tests of controls within each operating cycle, such as the revenue cycle, the personnel and payroll cycle, the spending or disbursement cycle, and the investment and financing cycle. In order to conduct tests of controls, for each operating cycle an auditor should understand the characteristics such as which documents and employees are typically involved, the control strengths and weaknesses found within the cycle, and common control issues that occur in the cycle. Here, Roger provides some context for conducting tests of controls in the revenue cycle. The revenue cycle involves sales, accounts receivable, and cash receipts. Because cash collections are part of the revenue cycle, and cash carries a high degree of inherent risk, there is a high degree of inherent risk in the revenue cycle, which can be managed with key controls. One key control is requiring pre-printed, pre-numbered, numerically sequenced documents, such as checks in a checkbook. The revenue cycle is then triggered when a customer sends a purchase order. Connect with us: Website: https://accounting.uworld.com/cpa-rev... Blog: https://accounting.uworld.com/blog/cp... Twitter: / uworldrogercpa Facebook: / uworldrogercpareview Instagram: / uworldrogercpareview Pinterest: / uworldrogercpareview LinkedIn: / uworld-roger-cpa-review Are you accounting faculty looking for FREE CPA Exam resources in the classroom? Visit our Professor Resource Center: https://accounting.uworld.com/cpa-rev... Video Transcript Sneak Peek: Now in your notes it mentions that controls have a function of either preventing misstatements before they occur, most effective, or detecting and correcting misstatements that have already occurred, which is less expensive to implement, but could be detected too late. If you detect too late, they end up in the financial statements, which could be a problem. That's what we're looking at as far as operating cycles. Now, with the cycles, we're going to look at a couple of different cycles, revenue cycle, expenditure cycle, and so on. Let's start out here with the revenue cycle. The revenue cycle, let's think about ... and for each cycle, what I want you to think about is what cycle are we in, what documents and what employees exist in that cycle, and then, basically, what are the strengths or weaknesses, what could go right, what could go wrong. As we look at this cycle, the first question is what's happening in the revenue cycle? Let's think about it. We have a lot of money, money, money, and cash coming in. Cash is coming in because we're getting revenue because we're making a sale, so sales. And then when you make a sale, you have an account receivable, and then when you collect that account receivable that's cash receipts. Cash, cash, cash, has a lot of what kind of risk? Inherent risk. You need a lot of key controls. So in this cycle, we're going to talk about sales, accounts receivable, cash receipts. Again, cash, cash, cash has a lot of what kind of risk? Inherent risk. Therefore you need a lot of what? A lot of key controls. Okay, now, when we look at this cycle, what I want us to think about are what are the key documents? If you look in your notes, you'll see it starts out it says, here are the specific employees that are doing certain things and we'll talk about the sales clerk, the credit manager, warehouse clerk, shipping clerk, we'll come back to those, but then it talks about some of the documents. Now, with all of these documents, the documents should be PPN, and multiple copies. What does it mean? PPN means preprinted, pre-numbered, and numerically controlled. If you look at your checks, on your check, aren't they preprinted? Mm-hmm. Aren't they pre-numbered? Mm-hmm. Aren't you accounting for them, numerically controlled? So if you're missing check, actually true story. Someone broke into my office, and what they did ... They didn't actually break in, someone left the door open. It was during working hours. So all of a sudden, someone had said, "Hey, there was someone in your office, and I went in and they kind of said, 'Oh, sorry, I was in the wrong place,' "and they left." They looked around, they said, "I didn't see anything missing."

Comments