Moving Average MA Time Series Models скачать в хорошем качестве

Moving Average MA Time Series Models

5 дней назад

Не удается загрузить Youtube-плеер. Проверьте блокировку Youtube в вашей сети.

Повторяем попытку...

Повторяем попытку...

Скачать видео с ютуб по ссылке или смотреть без блокировок на сайте: Moving Average MA Time Series Models в качестве 4k

У нас вы можете посмотреть бесплатно Moving Average MA Time Series Models или скачать в максимальном доступном качестве, видео которое было загружено на ютуб. Для загрузки выберите вариант из формы ниже:

-

Информация по загрузке:

Скачать mp3 с ютуба отдельным файлом. Бесплатный рингтон Moving Average MA Time Series Models в формате MP3:

Если кнопки скачивания не

загрузились

НАЖМИТЕ ЗДЕСЬ или обновите страницу

Если возникают проблемы со скачиванием видео, пожалуйста напишите в поддержку по адресу внизу

страницы.

Спасибо за использование сервиса ClipSaver.ru

Moving Average MA Time Series Models

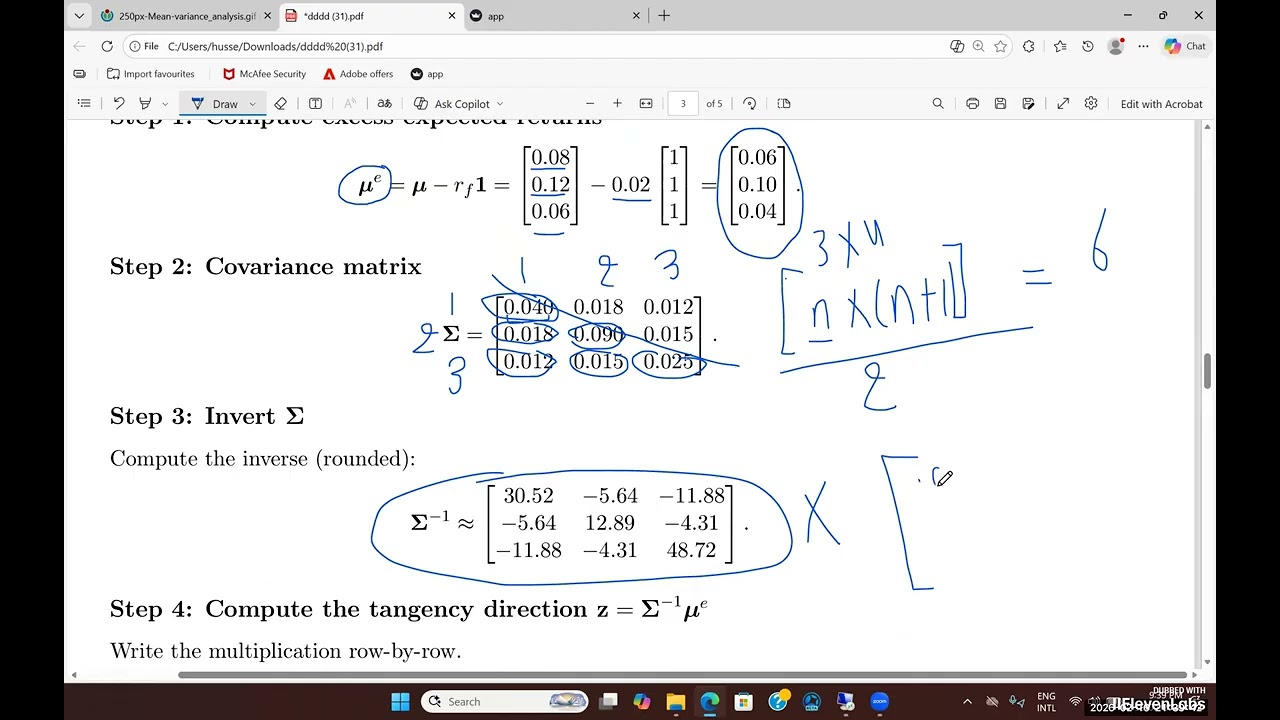

In this lecture, we explain moving average (MA) time-series models from first principles, with a strong focus on intuition, econometric logic, and empirical finance applications. We clarify what MA(q) really means as a moving average of error shocks, not past values, and show how shocks propagate over time and generate short-memory dependence. We apply a moving average (MA) model to month-to-month returns for the overall market using the Finance Research Gate website. The estimated MA(1) coefficient (θ₁) is statistically significant at the 10% level but not at the 5% level. This provides only weak evidence of short-term dependence in market returns. Therefore, while the results do not strongly support violations of market efficiency, they also do not fully rule out mild short-run predictability at the monthly horizon.

Comments

-

Трансляция закончилась 3 дня назад

Трансляция закончилась 3 дня назад

-

1 час назад

1 час назад

-

1 день назад

1 день назад

-

6 дней назад

6 дней назад

-

2 дня назад

2 дня назад

-

3 дня назад

3 дня назад

-

6 часов назад

6 часов назад

-

Трансляция закончилась 47 минут назад

Трансляция закончилась 47 минут назад

-

6 дней назад

6 дней назад

-

1 день назад

1 день назад

-

10 дней назад

10 дней назад

-

4 дня назад

4 дня назад

-

1 час назад

1 час назад

-

12 дней назад

12 дней назад

-

1 день назад

1 день назад

-

3 дня назад

3 дня назад

-

![Trump i Netanjahu uderzają. Rosja i Chiny bezsilne [Analiza]](https://imager.clipsaver.ru/NJ0t3ykIjLU/max.jpg) 4 часа назад

4 часа назад

-

6 часов назад

6 часов назад

-

2 дня назад

2 дня назад

-

5 часов назад

5 часов назад