Black–Litterman for Maximum Sharpe Optimization Theory and Numerical Example скачать в хорошем качестве

Black–Litterman for Maximum Sharpe Optimization Theory and Numerical Example

2 недели назад

Не удается загрузить Youtube-плеер. Проверьте блокировку Youtube в вашей сети.

Повторяем попытку...

Повторяем попытку...

Скачать видео с ютуб по ссылке или смотреть без блокировок на сайте: Black–Litterman for Maximum Sharpe Optimization Theory and Numerical Example в качестве 4k

У нас вы можете посмотреть бесплатно Black–Litterman for Maximum Sharpe Optimization Theory and Numerical Example или скачать в максимальном доступном качестве, видео которое было загружено на ютуб. Для загрузки выберите вариант из формы ниже:

-

Информация по загрузке:

Скачать mp3 с ютуба отдельным файлом. Бесплатный рингтон Black–Litterman for Maximum Sharpe Optimization Theory and Numerical Example в формате MP3:

Если кнопки скачивания не

загрузились

НАЖМИТЕ ЗДЕСЬ или обновите страницу

Если возникают проблемы со скачиванием видео, пожалуйста напишите в поддержку по адресу внизу

страницы.

Спасибо за использование сервиса ClipSaver.ru

Black–Litterman for Maximum Sharpe Optimization Theory and Numerical Example

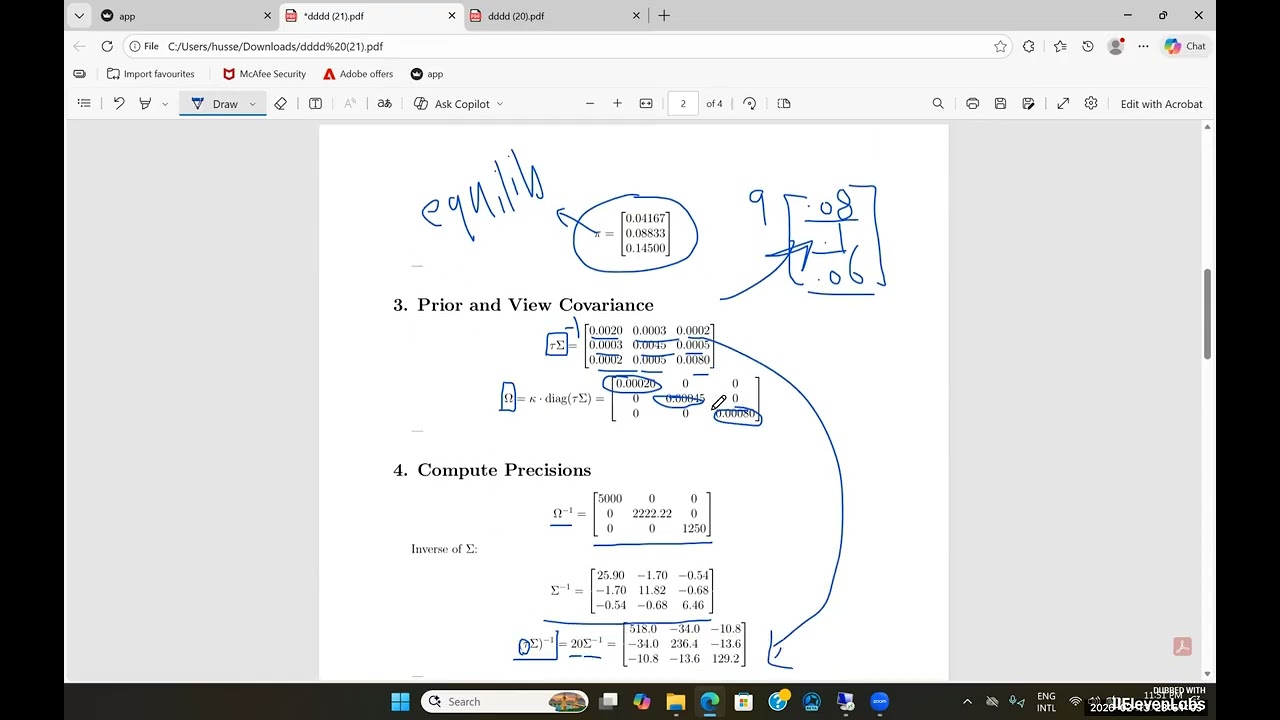

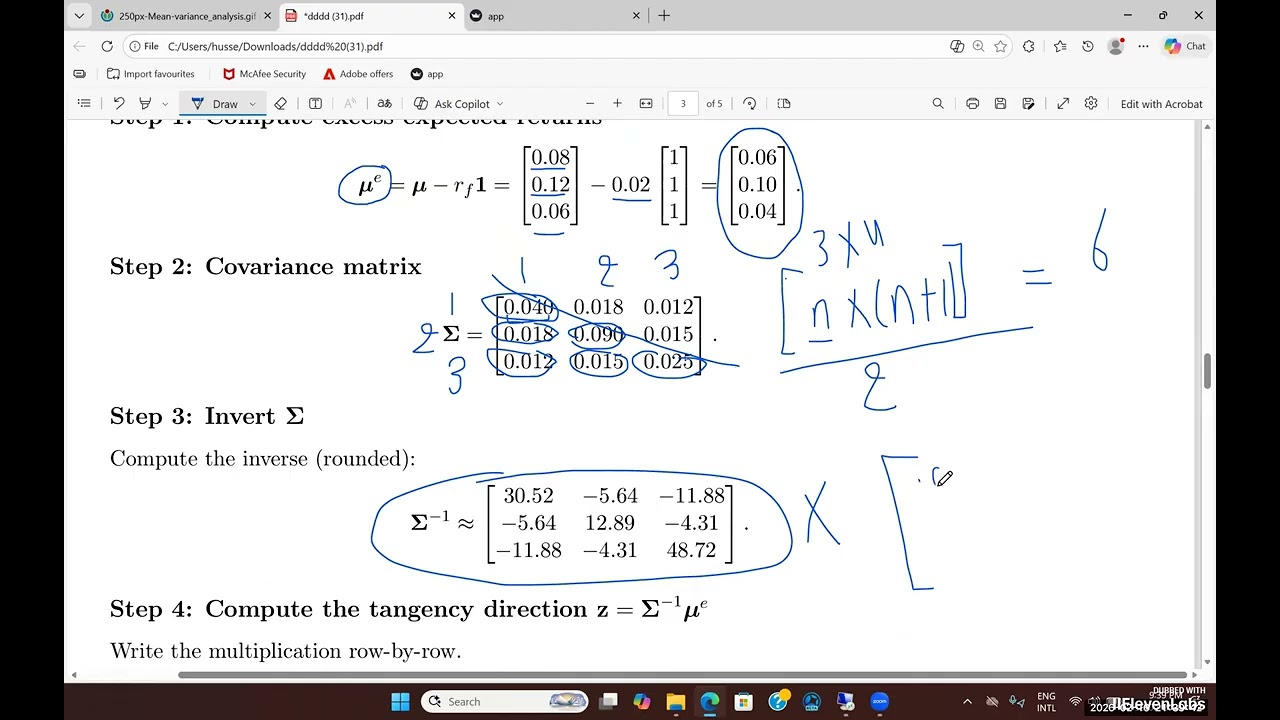

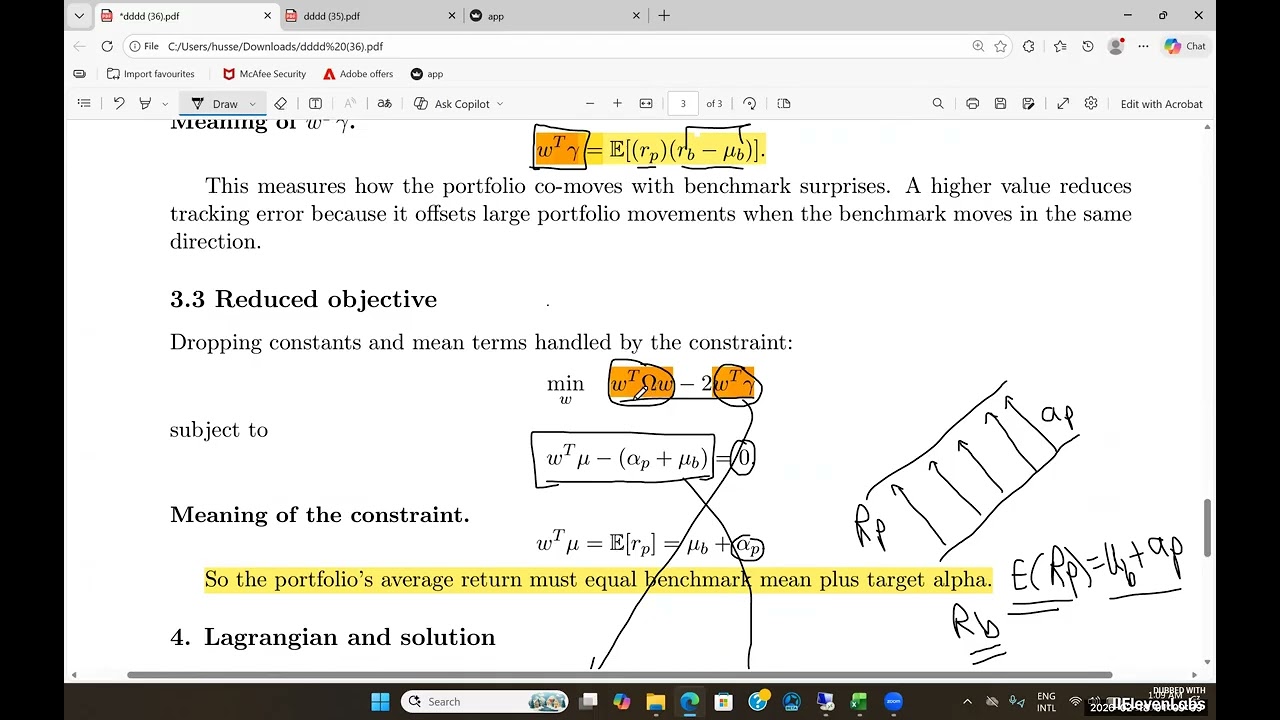

We explain the Black–Litterman model for portfolio optimization and show how it can be used to construct a maximum Sharpe ratio portfolio. We start from the mean–variance framework and introduce the Black–Litterman prior, investor views, and the role of the picking matrix and view uncertainty. Using a clear numerical example, we demonstrate how expected returns are updated and how the resulting posterior returns are used in portfolio optimization. The lecture connects theory, matrix algebra, and practical implementation, with applications illustrated using Finance Research Gate.

Comments

-

2 года назад

2 года назад

-

5 дней назад

5 дней назад

-

6 месяцев назад

6 месяцев назад

-

Трансляция закончилась 1 час назад

Трансляция закончилась 1 час назад

-

2 недели назад

2 недели назад

-

2 часа назад

2 часа назад

-

11 месяцев назад

11 месяцев назад

-

23 часа назад

23 часа назад

-

2 недели назад

2 недели назад

-

13 дней назад

13 дней назад

-

1 день назад

1 день назад

-

6 дней назад

6 дней назад

-

19 часов назад

19 часов назад

-

12 дней назад

12 дней назад

-

3 недели назад

3 недели назад

-

4 дня назад

4 дня назад

-

9 часов назад

9 часов назад

-

8 месяцев назад

8 месяцев назад

-

Трансляция закончилась 1 день назад

Трансляция закончилась 1 день назад

-

2 дня назад

2 дня назад