Minimum Variance Tracking Error Portfolio скачать в хорошем качестве

Minimum Variance Tracking Error Portfolio

11 дней назад

Не удается загрузить Youtube-плеер. Проверьте блокировку Youtube в вашей сети.

Повторяем попытку...

Повторяем попытку...

Скачать видео с ютуб по ссылке или смотреть без блокировок на сайте: Minimum Variance Tracking Error Portfolio в качестве 4k

У нас вы можете посмотреть бесплатно Minimum Variance Tracking Error Portfolio или скачать в максимальном доступном качестве, видео которое было загружено на ютуб. Для загрузки выберите вариант из формы ниже:

-

Информация по загрузке:

Скачать mp3 с ютуба отдельным файлом. Бесплатный рингтон Minimum Variance Tracking Error Portfolio в формате MP3:

Если кнопки скачивания не

загрузились

НАЖМИТЕ ЗДЕСЬ или обновите страницу

Если возникают проблемы со скачиванием видео, пожалуйста напишите в поддержку по адресу внизу

страницы.

Спасибо за использование сервиса ClipSaver.ru

Minimum Variance Tracking Error Portfolio

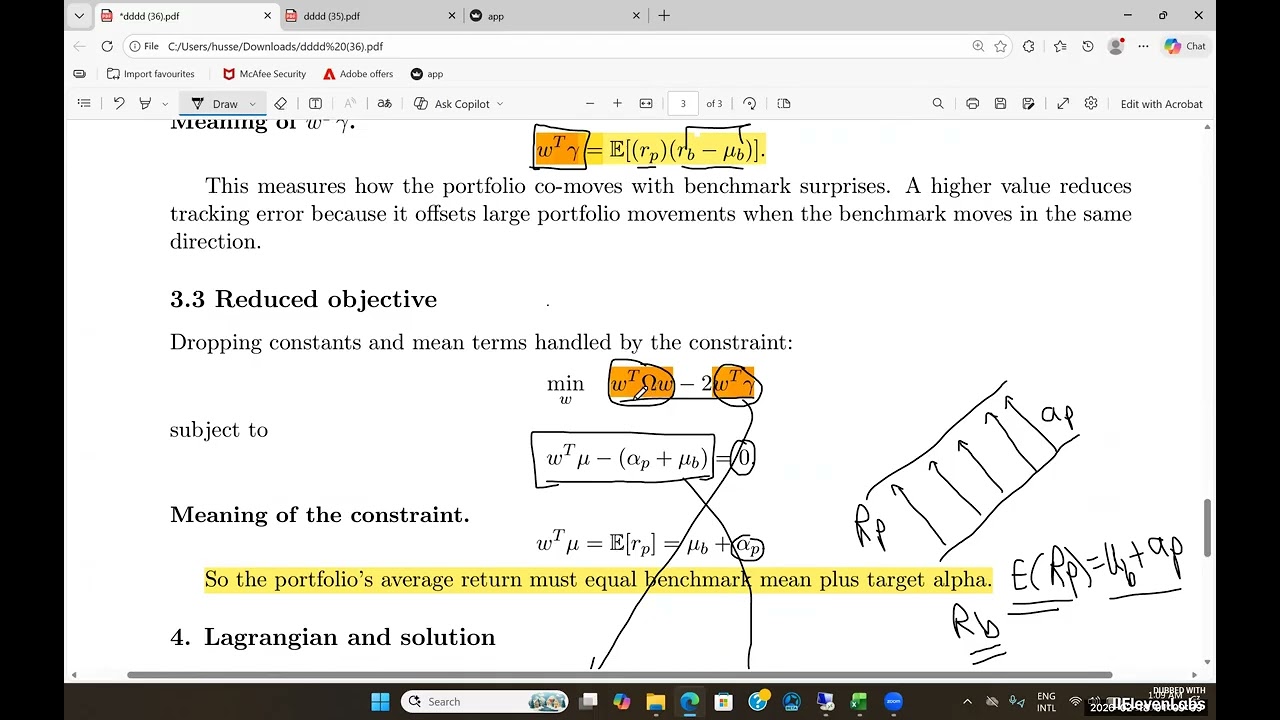

We develop the minimum variance tracking error portfolio in a fully unconditional setting. Starting from the definition of tracking error, we derive the optimization problem step by step and show how minimizing tracking error variance reduces to a quadratic form involving the second moment matrix of asset returns. We explain the economic meaning of each term in the objective, including why portfolio squared returns increase tracking error and how co-movement with benchmark surprises reduces it. The lecture clarifies the difference between second moments and covariances, explains the role of the mean tracking (alpha) constraint, and provides intuition for why the inverse second moment matrix determines optimal portfolio weights. The discussion emphasizes conceptual understanding and practical implementation, with applications illustrated using Finance Research Gate.

Comments