Credit Risk Modelling: Pricing of a Defaultable Bond with Reduced-Form Models Part I скачать в хорошем качестве

Credit Risk Modelling: Pricing of a Defaultable Bond with Reduced-Form Models Part I

1 год назад

Не удается загрузить Youtube-плеер. Проверьте блокировку Youtube в вашей сети.

Повторяем попытку...

Повторяем попытку...

Скачать видео с ютуб по ссылке или смотреть без блокировок на сайте: Credit Risk Modelling: Pricing of a Defaultable Bond with Reduced-Form Models Part I в качестве 4k

У нас вы можете посмотреть бесплатно Credit Risk Modelling: Pricing of a Defaultable Bond with Reduced-Form Models Part I или скачать в максимальном доступном качестве, видео которое было загружено на ютуб. Для загрузки выберите вариант из формы ниже:

-

Информация по загрузке:

Скачать mp3 с ютуба отдельным файлом. Бесплатный рингтон Credit Risk Modelling: Pricing of a Defaultable Bond with Reduced-Form Models Part I в формате MP3:

Если кнопки скачивания не

загрузились

НАЖМИТЕ ЗДЕСЬ или обновите страницу

Если возникают проблемы со скачиванием видео, пожалуйста напишите в поддержку по адресу внизу

страницы.

Спасибо за использование сервиса ClipSaver.ru

Credit Risk Modelling: Pricing of a Defaultable Bond with Reduced-Form Models Part I

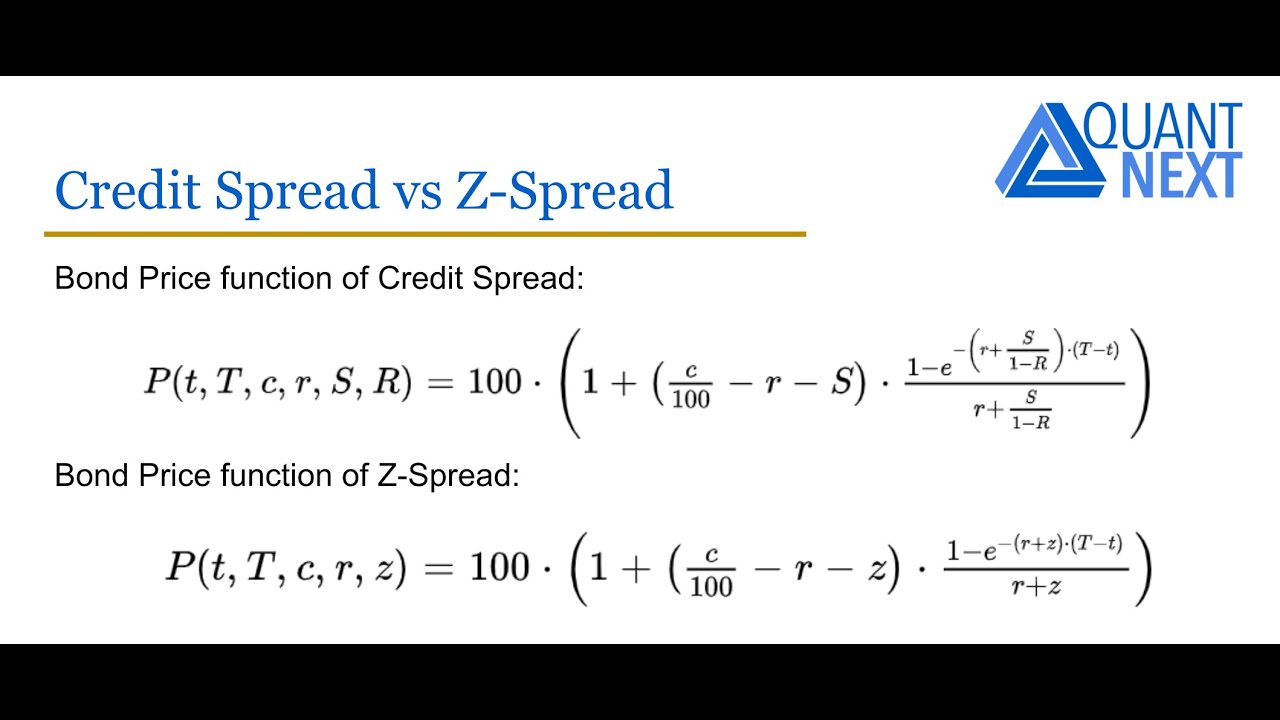

★★ Save 10% on All Quant Next Courses with the Coupon Code: QuantNextYoutube10 ★★ ★★ For students and graduates, we offer a 50% discount on all courses, please contact us if you are interested ★★ ★★ Visit us: https://quant-next.com ★★ ★★ Contact us: contact@quant-next.com ★★ ★★ Follow us: / quant-next ★★ In this video we will see how to price a risky zero coupon bond assuming zero recovery rate with a reduced-form model for credit risk. 0:14 Pricing of a Risk-Free Zero-Coupon Bond 0:53 Pricing of a Risky Zero-Coupon Bond No Recovery Rate 2:51 Estimation of the Survival Probability and the Default Intensity 3:04 Relationship between the Z-Spread and the Default Intensity #creditrisk, #creditriskmodel, #quantitativefinance, #financeeducation, #quant, #quantnext, #defaultprobability, #reducedformmodels, #defaultmodel, #bondpricing

Comments