Finance Theory — 16.1: From the CML to the SML: Why Beta Replaces σ скачать в хорошем качестве

Finance Theory — 16.1: From the CML to the SML: Why Beta Replaces σ

7 часов назад

Не удается загрузить Youtube-плеер. Проверьте блокировку Youtube в вашей сети.

Повторяем попытку...

Повторяем попытку...

Скачать видео с ютуб по ссылке или смотреть без блокировок на сайте: Finance Theory — 16.1: From the CML to the SML: Why Beta Replaces σ в качестве 4k

У нас вы можете посмотреть бесплатно Finance Theory — 16.1: From the CML to the SML: Why Beta Replaces σ или скачать в максимальном доступном качестве, видео которое было загружено на ютуб. Для загрузки выберите вариант из формы ниже:

-

Информация по загрузке:

Скачать mp3 с ютуба отдельным файлом. Бесплатный рингтон Finance Theory — 16.1: From the CML to the SML: Why Beta Replaces σ в формате MP3:

Если кнопки скачивания не

загрузились

НАЖМИТЕ ЗДЕСЬ или обновите страницу

Если возникают проблемы со скачиванием видео, пожалуйста напишите в поддержку по адресу внизу

страницы.

Спасибо за использование сервиса ClipSaver.ru

Finance Theory — 16.1: From the CML to the SML: Why Beta Replaces σ

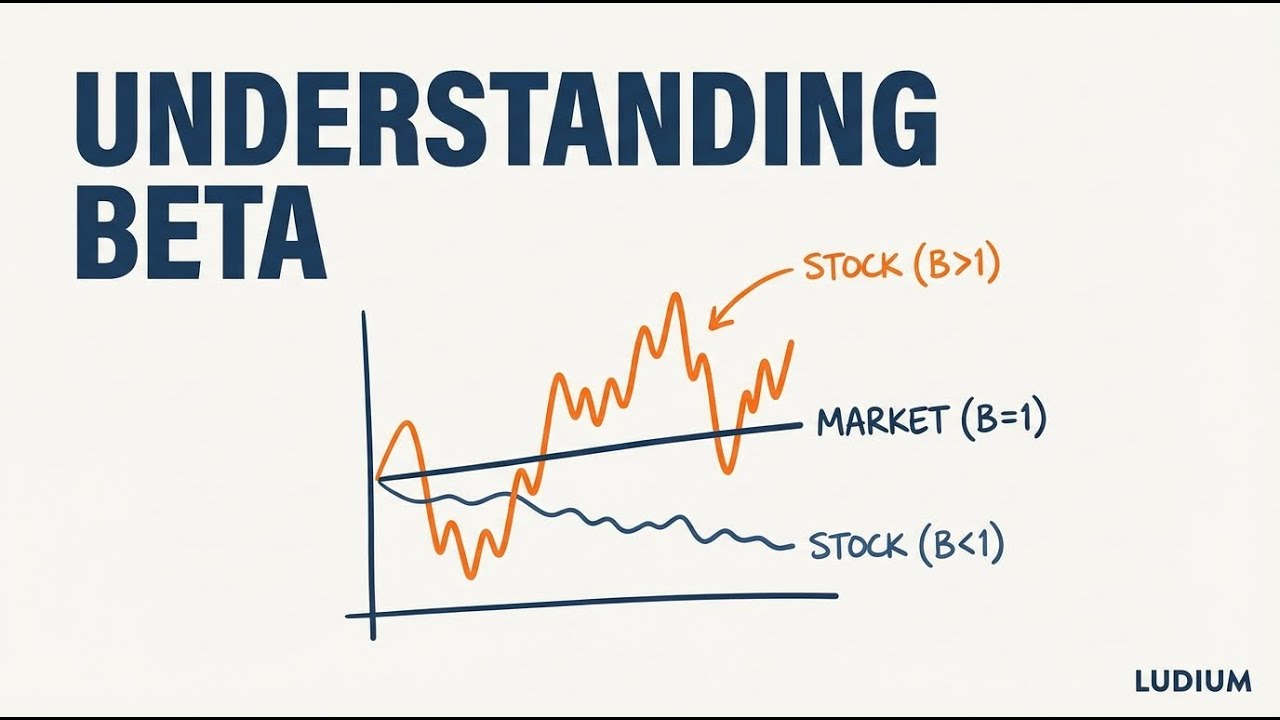

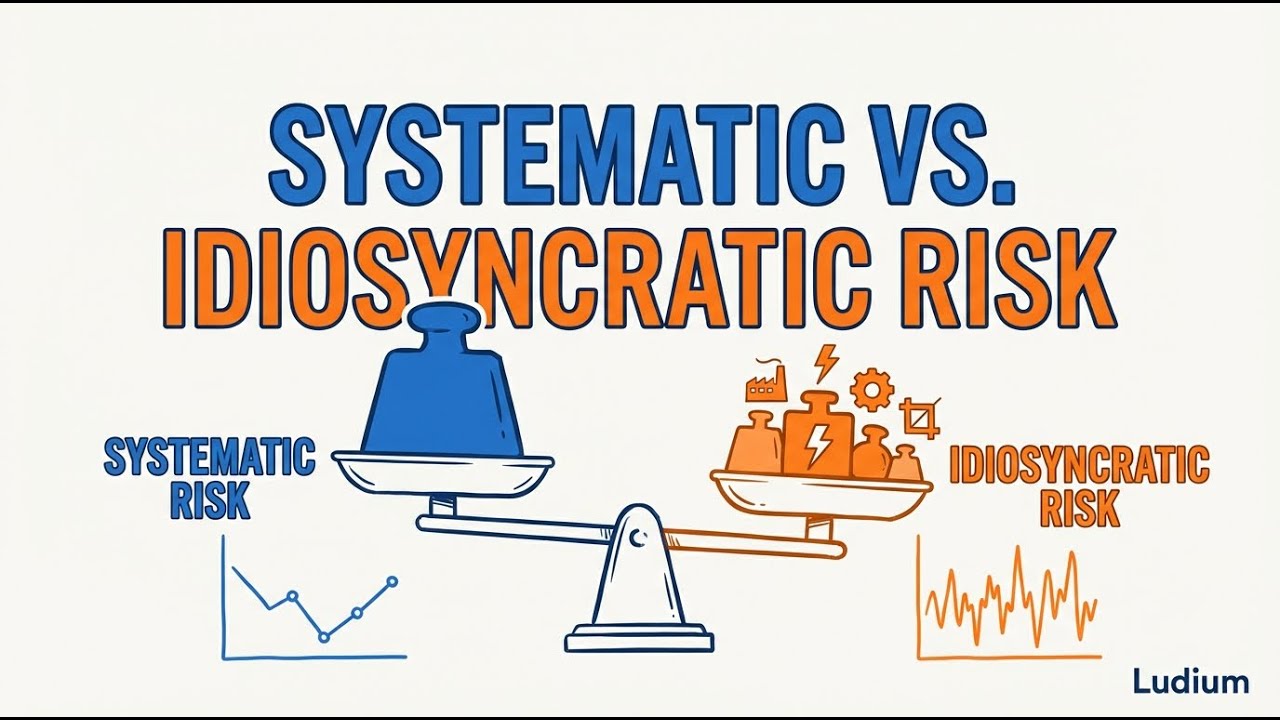

Why can't you use the Capital Market Line to find IBM's discount rate? Because the CML only works for efficient portfolios, and IBM isn't one. This video traces the precise logical step from the CML to the Security Market Line, showing why standard deviation gives way to beta — and why that single substitution produces a pricing equation that works for every asset in the economy. Key concepts covered: • The efficient frontier, the risk-free asset, and the derivation of the Capital Market Line (CML) • Why individual stocks like IBM sit below the CML and cannot be priced using total volatility (σ) • Diversifiable risk vs. systematic risk — and why only systematic risk earns a premium • Beta defined: Cov(Ri, Rm) / Var(Rm) as a measure of market sensitivity • The Security Market Line (SML) equation: E(Ri) = Rf + βi × (E(Rm) − Rf) • How the CML and SML agree on efficient portfolios where βp = σp/σm • Alpha as deviation from the SML — the basis for evaluating active management • Counterexample: a high-σ gold mining stock (β = 0.2) vs. a lower-σ regional bank (β = 1.3) • Step-by-step IBM discount rate calculation using the SML (β = 0.70, result = 8.35%) • The core CAPM insight: the market does not reward diversifiable risk ━━━━━━━━━━━━━━━━━━━━━━━━ SOURCE MATERIALS The source materials for this video are from • Ses 16: The CAPM and APT II

Comments