Applying and Explaining Vector Autoregression VAR Methodology in Time Series Analysis скачать в хорошем качестве

Applying and Explaining Vector Autoregression VAR Methodology in Time Series Analysis

1 день назад

Не удается загрузить Youtube-плеер. Проверьте блокировку Youtube в вашей сети.

Повторяем попытку...

Повторяем попытку...

Скачать видео с ютуб по ссылке или смотреть без блокировок на сайте: Applying and Explaining Vector Autoregression VAR Methodology in Time Series Analysis в качестве 4k

У нас вы можете посмотреть бесплатно Applying and Explaining Vector Autoregression VAR Methodology in Time Series Analysis или скачать в максимальном доступном качестве, видео которое было загружено на ютуб. Для загрузки выберите вариант из формы ниже:

-

Информация по загрузке:

Скачать mp3 с ютуба отдельным файлом. Бесплатный рингтон Applying and Explaining Vector Autoregression VAR Methodology in Time Series Analysis в формате MP3:

Если кнопки скачивания не

загрузились

НАЖМИТЕ ЗДЕСЬ или обновите страницу

Если возникают проблемы со скачиванием видео, пожалуйста напишите в поддержку по адресу внизу

страницы.

Спасибо за использование сервиса ClipSaver.ru

Applying and Explaining Vector Autoregression VAR Methodology in Time Series Analysis

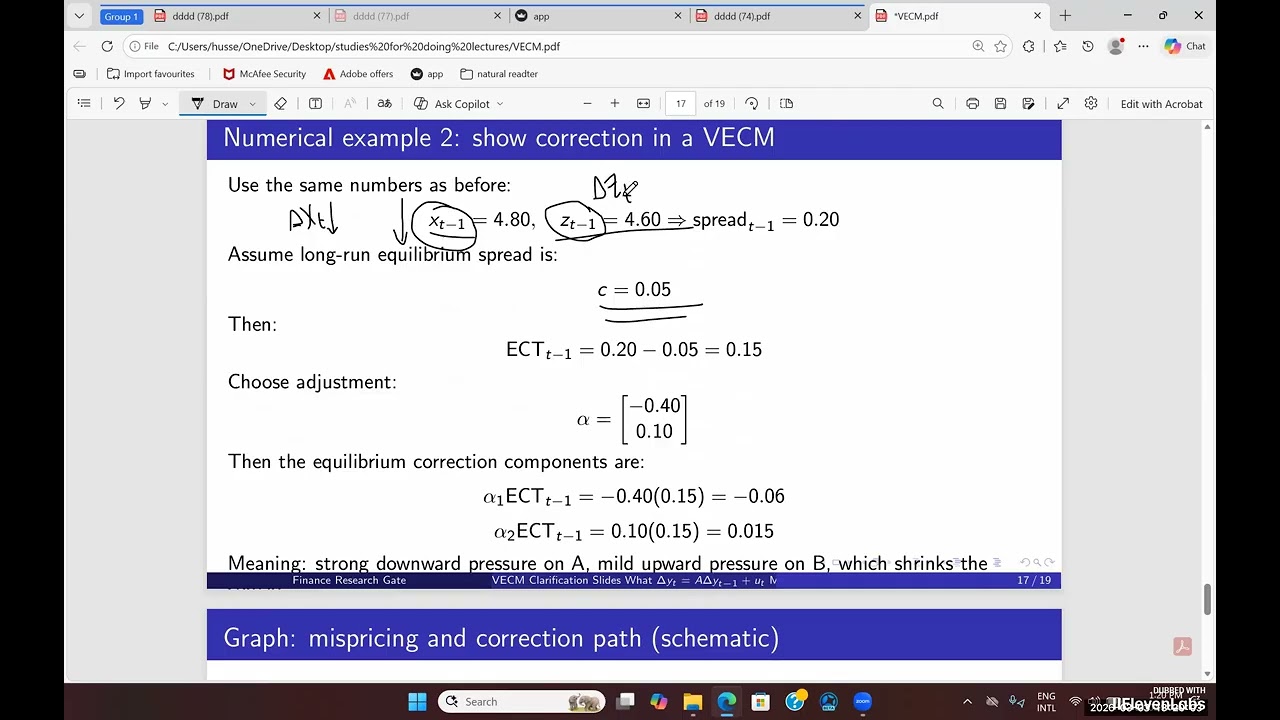

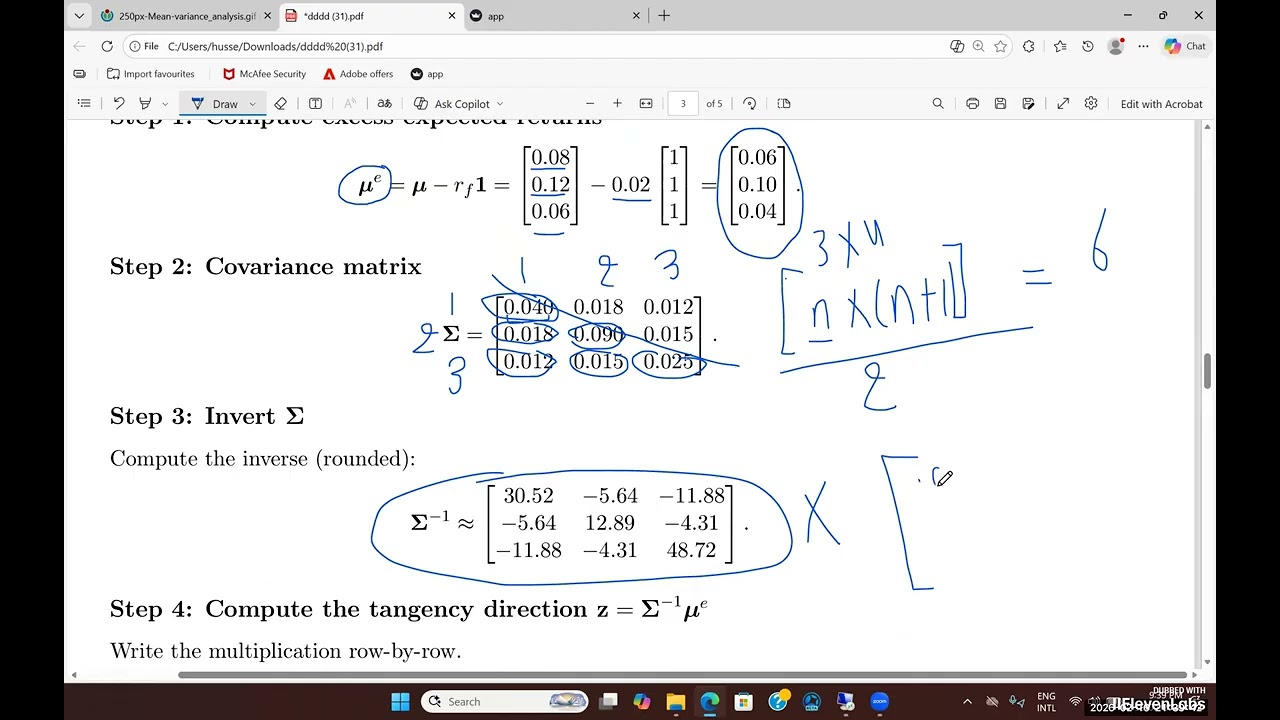

In this video, we apply and explain the Vector Autoregression (VAR) methodology in time series analysis. We walk through how multiple economic variables are modeled jointly, how the transition matrix is estimated, how expected values are formed, and how innovations capture unexpected movements. The focus is on understanding the mechanics of VAR models, interpretation of fitted versus actual values, and how VARs are used to analyze dynamic relationships in time series data. We use the finance research gate website. https://finresgate.com/app/

Comments