Finance Theory — 15.4: The Mutual Fund Separation Theorem скачать в хорошем качестве

Finance Theory — 15.4: The Mutual Fund Separation Theorem

1 день назад

Не удается загрузить Youtube-плеер. Проверьте блокировку Youtube в вашей сети.

Повторяем попытку...

Повторяем попытку...

Скачать видео с ютуб по ссылке или смотреть без блокировок на сайте: Finance Theory — 15.4: The Mutual Fund Separation Theorem в качестве 4k

У нас вы можете посмотреть бесплатно Finance Theory — 15.4: The Mutual Fund Separation Theorem или скачать в максимальном доступном качестве, видео которое было загружено на ютуб. Для загрузки выберите вариант из формы ниже:

-

Информация по загрузке:

Скачать mp3 с ютуба отдельным файлом. Бесплатный рингтон Finance Theory — 15.4: The Mutual Fund Separation Theorem в формате MP3:

Если кнопки скачивания не

загрузились

НАЖМИТЕ ЗДЕСЬ или обновите страницу

Если возникают проблемы со скачиванием видео, пожалуйста напишите в поддержку по адресу внизу

страницы.

Спасибо за использование сервиса ClipSaver.ru

Finance Theory — 15.4: The Mutual Fund Separation Theorem

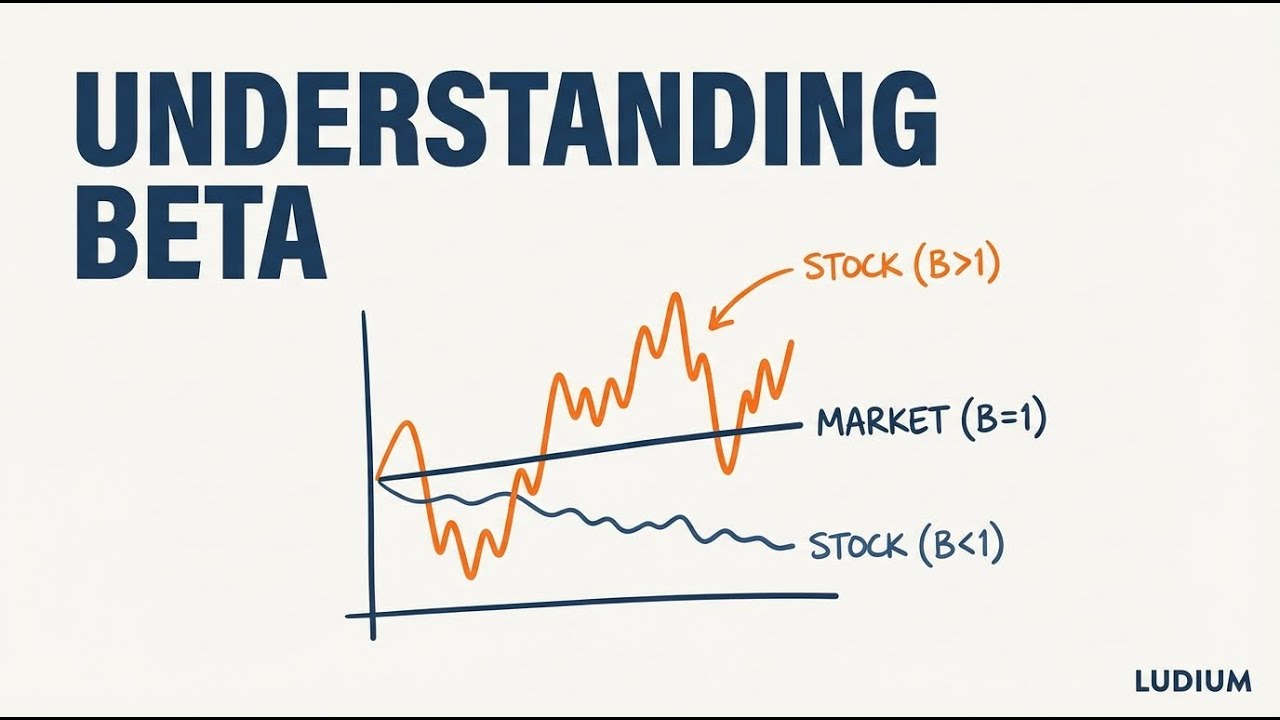

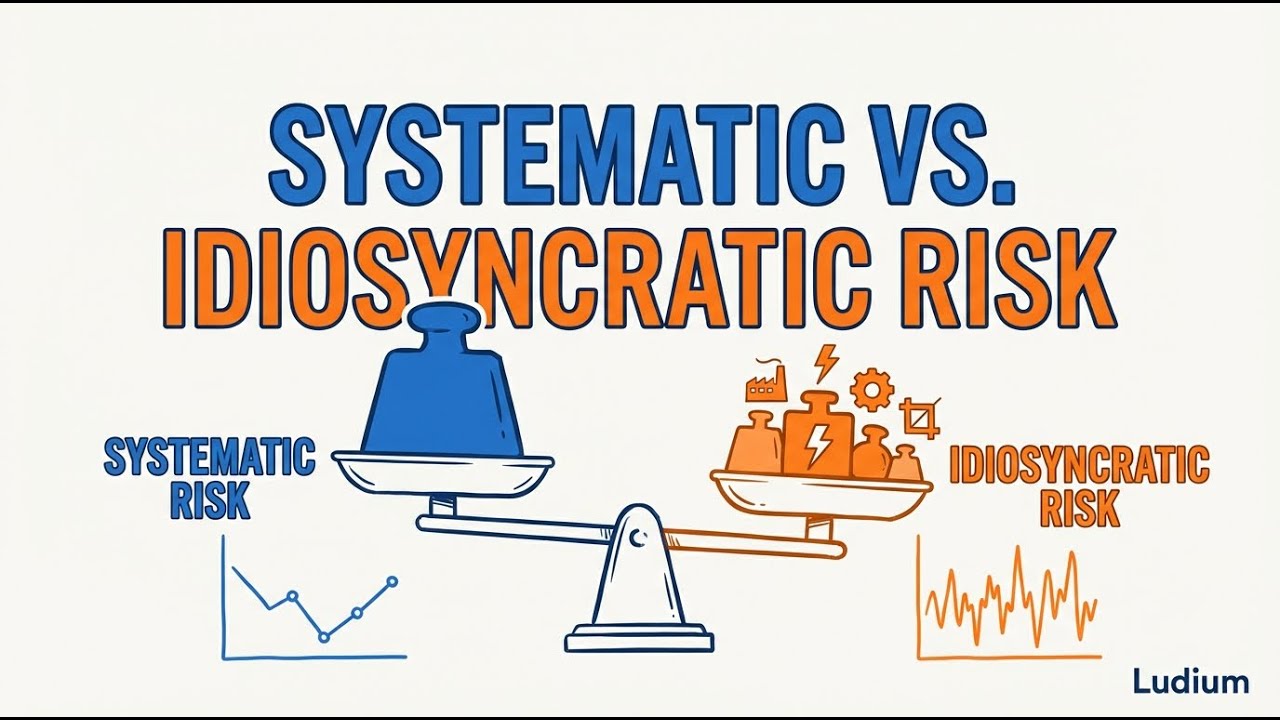

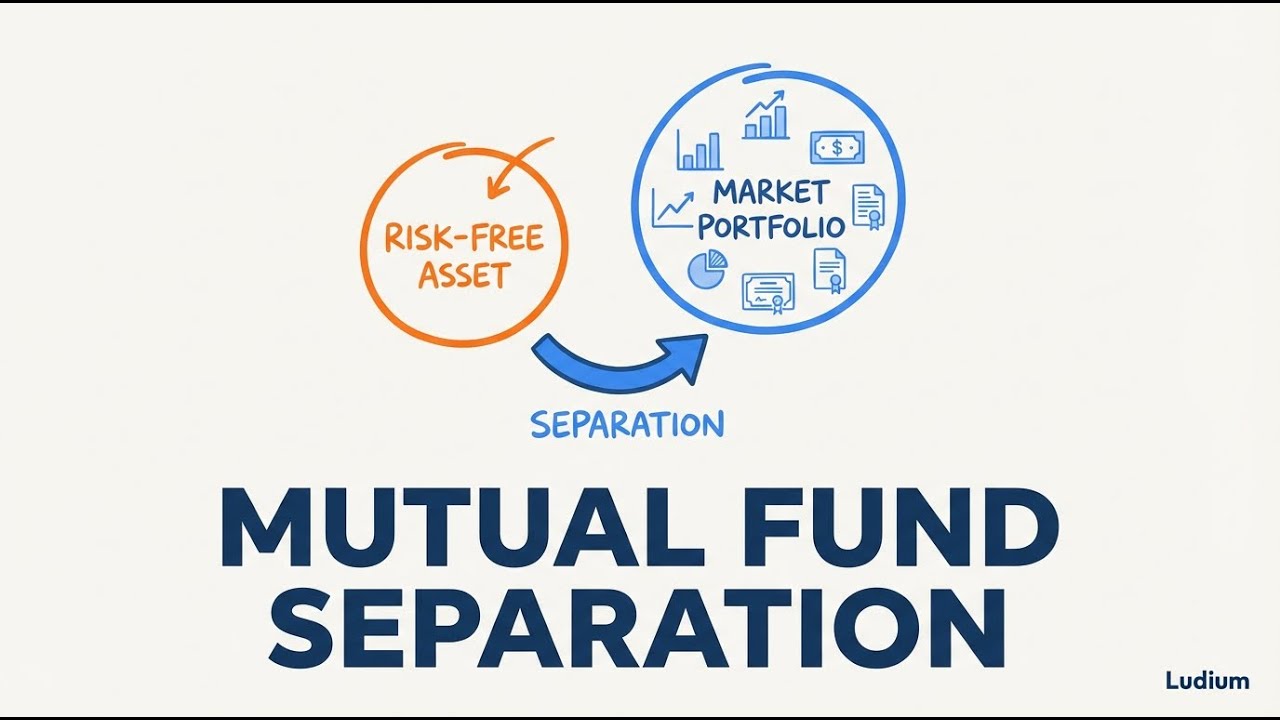

Why can one single mutual fund mathematically serve every investor — from the most conservative to the most aggressive? This video builds from indifference curves through the Capital Allocation Line to the Mutual Fund Separation Theorem, then examines what alpha really means and why most active managers fail to deliver it after fees. Key concepts covered: • Indifference curves in risk-return space: why they slope upward and are convex • Diminishing marginal utility of risk and the ice cream sundae analogy • Risk-averse vs. risk-tolerant investors: steep vs. flat indifference curves • The Capital Allocation Line (CAL) from the risk-free rate through the tangency portfolio M • Mutual Fund Separation Theorem: one fund plus T-Bills serves all mean-variance investors • Alpha as risk-adjusted outperformance above the passive benchmark line • The "2 and 20" fee structure and why managers need roughly 2.5% gross alpha just to break even • Fee drag: how management fees erode or eliminate alpha on the risk-return diagram • Berkshire Hathaway as evidence of genuine sustained alpha (Sharpe ratio above the S&P 500) • Practical takeaway: buy an index fund, adjust your T-Bill allocation, and demand after-fee alpha from any active manager ━━━━━━━━━━━━━━━━━━━━━━━━ SOURCE MATERIALS The source materials for this video are from • Ses 15: Portfolio Theory III & The CAPM an...

Comments